In a VN30 rebalance story, the easiest mistake for a new investor is often not misreading which stock may be added or removed. The bigger mistake is misreading the timeline: the data is already locked by late June, while most mechanical ETF flows usually show up more clearly around the announcement date and the effective date. If you watch the tape without watching the calendar, it becomes easy to buy into emotion after the market has already priced in part of the story.TBTCVN

For the third-quarter 2026 review, BSC expects HoSE to add MCH and TCX to the VN30 basket while removing TPB and PLX. The schedule currently discussed points to a July 15 announcement and an August 3 effective date.TBTCVN So this is not really a simple “index inclusion means upside” story. It is a test of whether investors understand the mechanism before reacting to price.

The three dates matter more than the stock names

If you remember only one point from this piece, remember the three dates. Late June is when the inputs for the review are effectively locked. July 15, if the schedule holds, is when the market gets the official list. August 3 is when the new basket starts to take effect for index-tracking funds.TBTCVN

Those dates lead to three different questions. Before the announcement, the market is mainly trading probabilities and brokerage forecasts. After the announcement, the focus shifts to the scale of trading passive funds may have to execute. Near the effective date, the real question becomes whether actual liquidity is deep enough to absorb those mechanical orders.

That is why a stock can rise before its inclusion is officially confirmed, then stall once the formal announcement arrives. When everyone is looking at the same schedule, the edge no longer comes from simply “knowing the news.” It comes from understanding how much of that news is already in the price.

Why MCH and TCX are being flagged

VN30 is not a popularity list. The basket is screened based on market capitalization, free-float ratios, and liquidity. A company can be large and still fall short if its tradable float or trading depth does not fit the index framework.

MCH clearly has the strongest scale advantage in this review. On June 29, the stock closed at VND 131,000 per share, implying a market capitalization of roughly VND 169,600 billion. TCX closed at VND 44,400, with a market capitalization of around VND 102,600 billion. On the other side, TPB ended at VND 16,350 with a market capitalization of about VND 45,400 billion, while PLX closed at VND 37,250 with a market capitalization of roughly VND 47,300 billion. At a basic level, those figures explain why the market is paying more attention to MCH and TCX in this review cycle.

But market value is only the first layer. For a stock like TCX, the free-float ratio is the variable worth tracking because it directly affects the capitalization used in the index review. If that ratio comes in below expectations, the stock’s fit for VN30 can look different from what the headline market cap suggests.

On the other side, if TPB or PLX is projected to leave the basket, that does not mean the business suddenly deteriorated overnight. What it signals first is a weaker relative position under this period’s scoring framework. A stock can lose ground in index ranking without its core business story turning materially worse.

ETFs are what give this story real weight

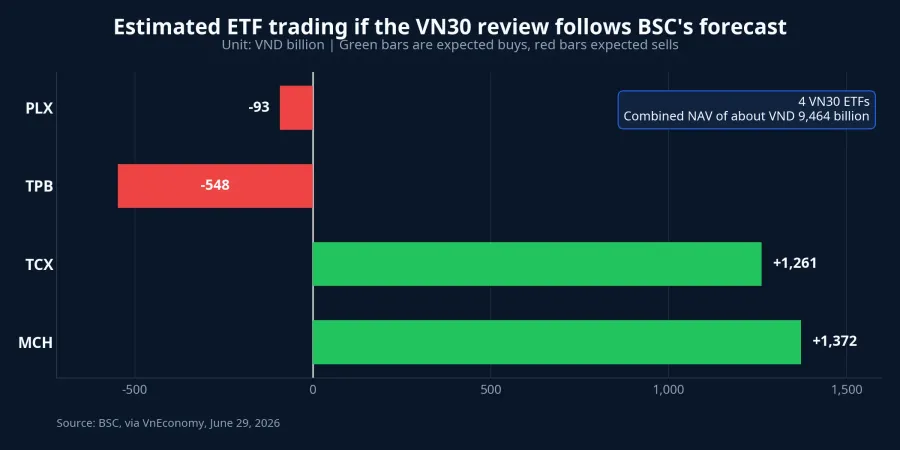

The reason VN30 reviews always attract speculative attention is the ETF layer. According to VnEconomy, four funds tracking VN30, DCVFMVN30, KIM Growth VN30, MAFM VN30, and SSIAM VN30, currently have combined NAV of around VND 9,464 billion.VnEconomy When the index changes its basket, those funds do not have much room to trade on discretion. They have to align portfolios with the benchmark.

The same source says BSC estimates that MCH could see around VND 1,372 billion in ETF buying and TCX around VND 1,261 billion if both are added. On the sell side, TPB could face around VND 548 billion of selling pressure and PLX around VND 93 billion if they are removed.VnEconomy Those figures are large enough to explain why the market often moves ahead of a rebalance.

Still, these are forecast-based estimates, not confirmed trading instructions. If the final basket differs from expectations, if fund size changes before the effective date, or if final weights are calculated differently, the actual trading amounts will also change. The numbers help investors understand the mechanism. They do not promise a fixed price path.

That is also why investors should avoid assigning every move to one cause. If MCH or TCX rises before the announcement, part of that may reflect VN30 inclusion expectations. But it may also reflect front-running, broader appetite for large-cap names, and liquidity concentrating in a small set of stocks. The more disciplined reading is that price action is moving alongside rebalance expectations, not that the rebalance alone explains everything.

Inclusion does not mean a straight line higher

The mechanism is simple. If the market knows a group of ETFs may have to buy a stock soon, some active investors will try to buy first. Once that happens, the easiest part of the trade may already be in the price before the funds execute. When the mechanical buying finally arrives, the stock can still climb, but it can also run into profit-taking because earlier buyers start to exit.

The reverse can happen with stocks expected to leave the index. Selling pressure may show up early because the market knows passive funds may need to cut weight. But once that mechanical selling is out of the way, the stock can stabilize if the business story does not deteriorate further. That is why “removed from VN30” is not a final verdict, just as “added to VN30” is not a guarantee of a sustained rally.

After the funds finish rebalancing, the market returns to its usual questions. Is the valuation still reasonable. How much profit-taking supply is waiting. And does the business have enough earnings, cash flow, and forward visibility to defend the new price range. Index news can create very real short-term moves, but business quality still acts as the final filter.

What new investors should watch from now to the effective date

The first step is to separate forecasts from confirmation. Before July 15, every scenario is still a probability, no matter how often MCH and TCX are mentioned. Buying simply because “they are almost certainly getting in” is still a bet on the forecast holding up. For a new investor, understanding the bet matters more than the stock symbol itself.

The second step is to look at baseline liquidity, not just the estimated order value. A VND 1,372 billion buy order in MCH sounds huge, but the price impact still depends on how much stock is available for sale and what normal trading volume looks like. In the same way, VND 93 billion of selling in PLX should not be read the same way as VND 93 billion of selling in a much less liquid stock.

The third step is to remember that VN30 is an index basket, not a recommendation list. A stock enters because it fits the benchmark rules at a given point in time. That may attract additional passive money, but it does not replace earnings, operating cash flow, valuation, or sector risk. For investors holding index ETFs or fund certificates, the lesson is even clearer: passive investing always comes with a hidden cost, because funds must trade on schedule rather than only at the most attractive price.

The most practical conclusion is this: in this VN30 review, the more reliable thesis is not “the winning names are the stocks entering the basket.” The stronger thesis is that the market will keep reacting to the calendar and to the mechanical rebalancing needs of ETFs. The three signals worth tracking from now until the effective date are the official list on July 15, the revised trading estimates once that list is locked, and actual liquidity around August 3. If those three signals do not line up, price action can look very different from the crowd’s first instinct.