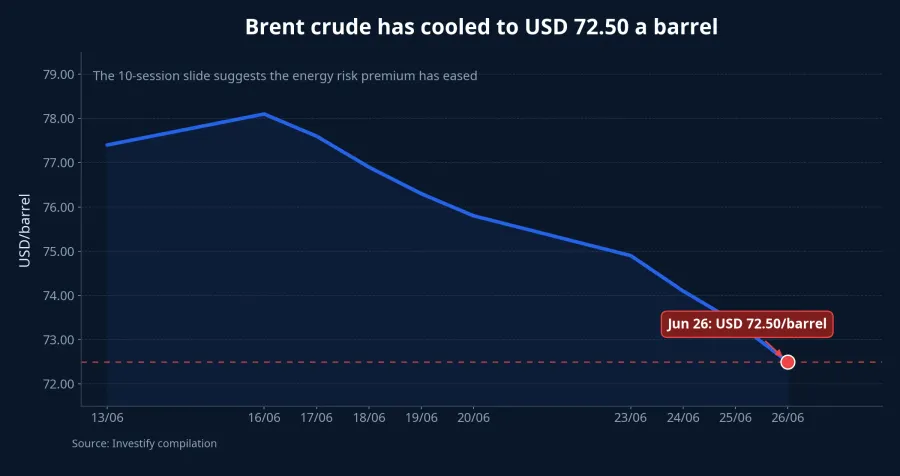

Oil is usually the first thing markets can see. When Brent dropped from USD 80.59 a barrel on June 19 to USD 72.50 on June 26, the sense of relief was understandable. Cooler energy prices usually mean less near-term inflation pressure, softer transport costs, and a smaller geopolitical risk premium.

But the bigger picture outlined by the BIS does not stop with oil. In the statement accompanying its annual economic report on June 28, the institution highlighted four pressure points: inflation, expectations around artificial intelligence, financial vulnerabilities, and public debt close to record levels.BIS In other words, markets may have become less afraid of one shock, without necessarily becoming stronger ahead of the next one.

That is the part many newer investors miss. A falling oil chart does not make sovereign balance sheets lighter, does not prove that AI investment will convert into durable profits, and does not improve bond-market shock absorption on its own.

Lower oil prices remove only one layer of fear

The numbers do matter. Brent fell roughly 10.0% in a single week. That is enough to change near-term sentiment because oil feeds directly into macro expectations.

But the BIS is not saying the most dangerous part of the story sits in oil itself. Its point is that every visible shock can expose deeper weaknesses underneath. When debt is already high, asset prices are already stretched, and liquidity in core markets is thinner than it looks, a new negative trigger can create a much larger chain reaction than investors expect.BIS

High debt leaves policymakers with less room

The first BIS warning is that public debt is sitting near record highs while global interest rates remain much higher than in the old cheap-money era.BIS The market implication is concrete: the more governments have already borrowed, the less freedom they have to deploy large-scale support in the next downturn without facing higher funding costs or bond-market resistance.

This is not just a budget story. Government bonds are the reference asset behind a wide range of valuations, from corporate borrowing costs to derivatives. When sovereign yields jump, they flow through to equity valuations, exchange rates, and the cost of capital across the system.

The BIS also notes that the growing role of non-bank financial institutions, including hedge funds, can make stress in bond markets spread faster during volatile periods.BIS The key takeaway is that the transmission channel can become shorter. Once liquidity weakens, the time markets have to rebalance themselves tends to shrink.

For Vietnamese investors, the first checkpoint in that story remains the US dollar. DXY rose from 100.86 on June 19 to 101.53 on June 26, an increase of roughly 0.7%. At the same time, USD/VND stood at 26,316 on June 26. One stronger week is not an exchange-rate shock, but it is enough to remind investors that when the world turns risk-averse, the dollar is usually the earliest place where the stress shows up.

Artificial intelligence is still a major expectation, not a risk-free zone

The second warning from the BIS is that the investment wave around artificial intelligence may be moving faster than the ability to verify it through real profits. The report acknowledges that AI can lift productivity, but it also says the sustainability of this cycle may come under pressure if supply bottlenecks constrain output or if the race for leadership leads to overinvestment.BIS

That matters because markets often confuse a valid long-term trend with a valuation that must always be valid. A technology can genuinely reshape the economy while the stocks linked to it still become too expensive in the short run, simply because capital is paying for expectations faster than profits can be delivered.

For Vietnam, the effect does not need to run through domestic companies immediately. It runs through global risk appetite. If large-cap US technology names come under pressure because investors start auditing capex bills or reassessing valuation multiples, international money usually becomes less enthusiastic about higher-risk assets in smaller markets.

Bond-market liquidity is the hardest part to see

If there is one part of this BIS warning that is both less visible and more unsettling, it is bond-market liquidity. For newer investors, the simplest definition is the ability to buy or sell without causing outsized price moves. When liquidity is thin, the same news can send prices lower much faster because there are not enough buyers standing in the middle.

That is why lower oil prices cannot be treated as a safety certificate for the rest of the market. If core bond markets are still fragile, a new shock from somewhere else can still send yields sharply higher, compress equity valuations, and strengthen the dollar as money rotates back toward defensive assets.

Gold tells a similar story. Spot gold stood at USD 4,052.38 an ounce on June 26, down roughly 2.4% from June 19. But on any timeframe broader than one week, gold is still sitting at an elevated level. That suggests the war premium may be fading while the demand for protection against broader uncertainty remains intact.

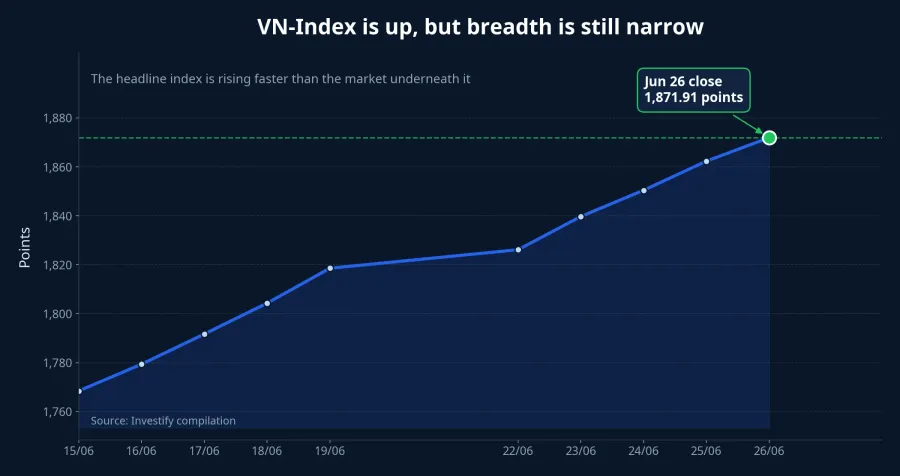

Vietnam is rising, but the breadth is not fully healthy

VN-Index closed at 1,871.91 on June 26, up about 2.6% from June 19. That is a meaningful advance and a reminder that the domestic market still has its own drivers.

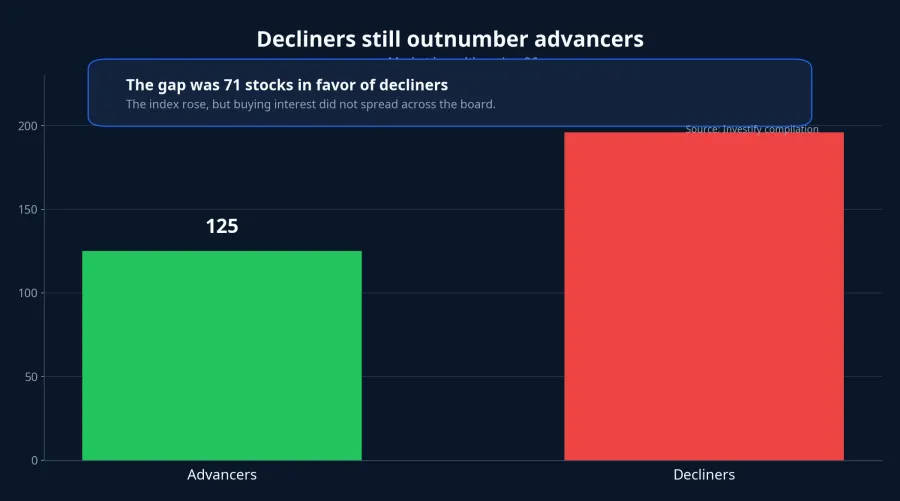

But one detail deserves closer attention: on June 26, decliners totaled 196, above the 125 advancers. The index moved higher, yet the support underneath it was not broad-based.

That does not mean the Vietnamese market is about to reverse immediately. It only means the durability of the current rally still depends on whether money starts to spread across a wider set of stocks.

What to watch next week

The central lesson from the BIS warning is that investors should not let one visible variable stand in for the whole risk picture. Lower oil only tells us that one source of pressure has eased. It says nothing definitive about sovereign debt, the durability of the AI investment cycle, or the shock-absorption capacity of bond markets.

That leaves a clear thesis: the world has removed part of its energy fear, but it has not yet moved past a broader test of financial-system resilience. For Vietnamese investors, the three signals worth watching over the next one to two weeks are whether DXY keeps climbing, whether gold stays elevated even as oil cools, and whether market breadth in Vietnam improves enough to validate the rise in VN-Index.

If all three ease together, the market will have a much firmer basis for relief. If oil keeps falling while the dollar stays firm, gold stays high, and breadth remains narrow, then markets have only let go of one fear rather than returning to a genuinely easier state.