CII has sold out 25 million CII425002 bonds, raising VND 2,500 billion from 652 investors.CafeF On its own, the phrase “sold out” can sound like a market seal of approval. In corporate bonds, and especially in convertibles, that is only the first layer of what investors should read.

Put simply, the market is not buying a generic bond label. It is paying for a specific bundle of rights, and accepting a very specific bundle of risks in return. Miss that trade-off and a new investor can easily mistake distribution success for a safety guarantee.

The clearest thesis here is straightforward: the deal sold out because it offers three layers of appeal at once, but all three matter only if CII can preserve cash flow, keep access to funding, and maintain enough equity value over a very long horizon. In other words, selling out does not mean the credit risk has disappeared.

What a sold-out deal actually tells you

CII425002 is not a plain-vanilla bond. Based on the issuance details reported by CafeF, it is a convertible bond into common shares, with no warrants, no collateral, a 15-year tenor, and a face value of VND 100,000 per bond.CafeF After costs, CII said it would retain just over VND 2,498.5 billion in net proceeds to invest in its projects and business programs.CafeF

That matters because buyers are clearly not treating the issue like short-term parking cash. They are willing to lock money up for a long period in exchange for two possibilities: earning interest during the holding period and preserving a path into the stock if conversion terms become attractive. That is very different from the logic of a deposit, where capital preservation and predictable cash flow come first.

Still, moving from a successful placement to the conclusion that the deal is “safe” is too large a leap. A sold-out transaction proves only that the risk-reward trade-off was attractive enough for a set of buyers on the issuance date. It does not prove that credit risk is gone, and it certainly does not prove that the issuer will deliver the exact scenario bondholders are hoping for.

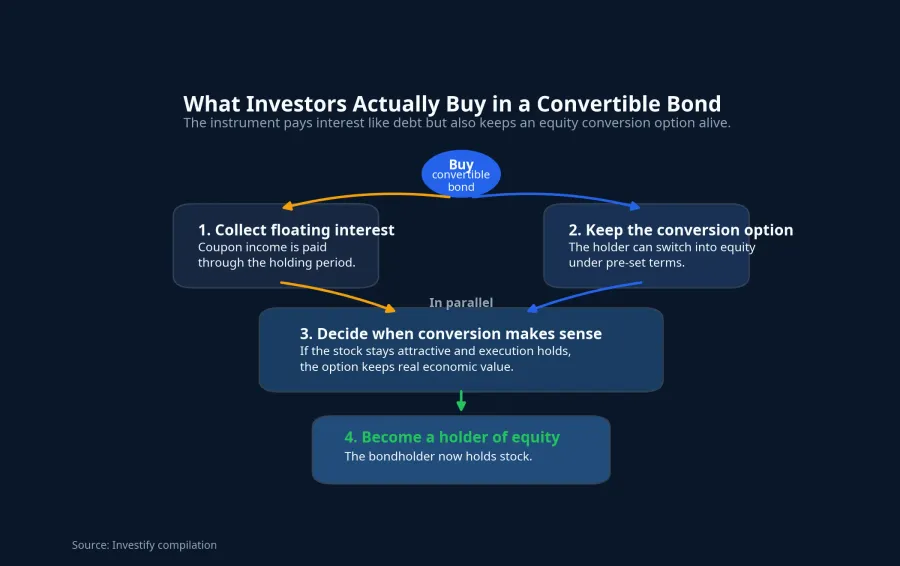

Investors are buying a hybrid contract

The first layer of appeal is the coupon. CII’s issuance result stated that the bond carries a floating rate equal to a reference rate plus a 3.5% annual spread.Vietstock That means investors are not just extending long-term credit. They are also collecting compensation for the issuer’s credit risk and for tying up capital in a long-duration infrastructure story.

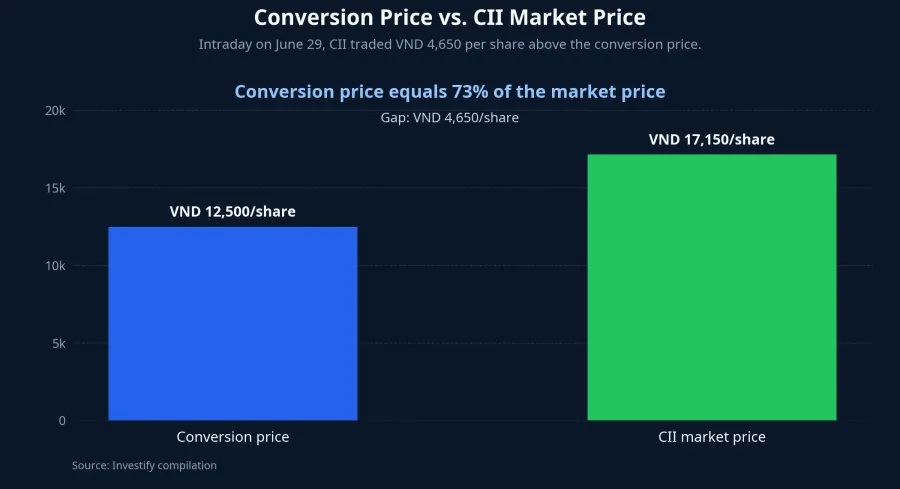

The second layer is the conversion option. The issuance plan sets a 1:8 conversion ratio, meaning one bond can turn into eight common shares at a conversion price of VND 12,500 per share.CafeF Intraday on June 29, CII stock was trading around VND 17,150 per share, above that conversion level. That gap alone is enough to keep the bond from being read as debt only.

But that is where discipline matters. A stock price above the conversion level only tells you the option has value at the time you observe it. It does not guarantee that the advantage will survive over a 15-year tenor. If the stock price drops sharply or project execution loses momentum, the most attractive feature of the convertible can weaken very quickly.

The third layer is confidence in CII’s ability to keep rolling capital through its infrastructure pipeline. That is probably the hardest part to measure. There is no precise way to break investor demand into coupon appetite, equity optionality, and trust in the company’s long-cycle funding model. Even so, the structure suggests buyers are willing to give CII more time to turn borrowed capital today into operating cash flow and equity value later.

Where the real risk sits

The first issue to read carefully is “no collateral.” That does not mean the company has no assets. It means this bond does not come with a ring-fenced asset that bondholders can look to first if the downside case materializes. For a new investor, that distinction matters: the size of a company’s asset base and the recovery position of a specific unsecured bond are not the same thing.

The second risk is that the conversion option only works if the stock remains attractive. Today, the gap between VND 12,500 and VND 17,150 makes the story look favorable. But bondholders are not buying a snapshot of one trading session. They are buying into a multi-year path in which the stock can move through several valuation cycles while the issuer still has to keep meeting interest obligations.

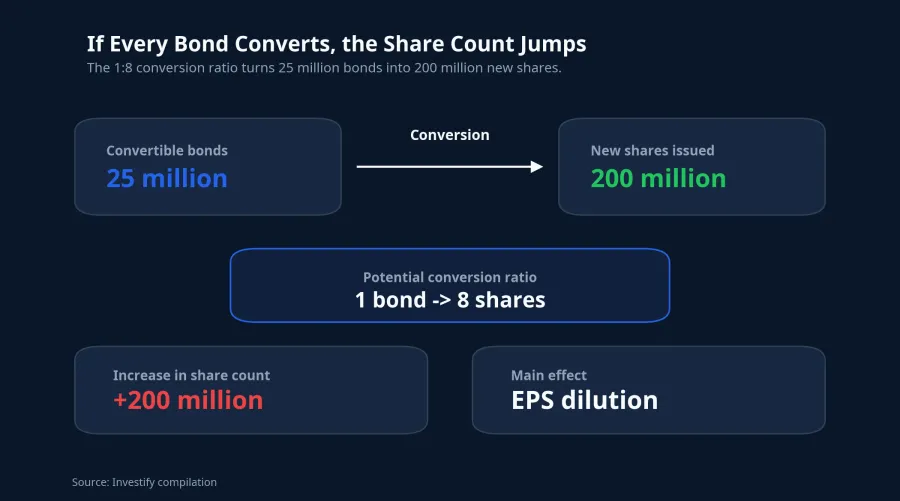

The third risk is dilution. If all 25 million bonds convert at the 1:8 ratio, the company could end up issuing as many as 200 million new shares.CafeF For existing shareholders, that directly affects how future earnings are spread across the capital base. For bondholders, dilution is not automatically negative, but it is a reminder that the interests of today’s creditors and today’s shareholders do not always move in lockstep.

What new investors should read after the headline

Another detail worth noting is that conversion is not scheduled as a one-off event. The issuance plan says it is expected to happen across 13 conversion rounds.CafeF That reduces single-day event risk, but it also stretches the investment story across many years. New investors should not read this as a simple “higher-yield-than-deposit” product and stop there.

A better way to read the transaction is in layers. Layer one is the placement result: CII sold everything. Layer two is the benefit structure: floating interest, a conversion option, and a path toward becoming a shareholder. Layer three is the part that determines real investment quality: how the company will generate cash flow from projects, whether the stock can stay comfortably above the VND 12,500 conversion price, and how meaningful dilution becomes if conversions are triggered at scale.

That is why the most defensible conclusion is not “the market has validated CII as safe,” but “the market has accepted a hybrid contract whose trade-off looked attractive at issuance.” That reading stays consistent with the evidence. What makes the bond worth studying is its structure, not the idea that a sold-out headline can answer the harder question of where cash flow will come from over the next 15 years.

The next signals to monitor are also clear. First, the execution pace of the projects CII is using the proceeds to fund. Second, the company’s ability to keep servicing interest as the rate backdrop changes. Third, the distance between CII’s stock price and the VND 12,500 conversion level over time. If those three signals hold up, the conversion option keeps its value. If they do not, the attractive issuance-day headline will give way to the oldest debt question of all: who pays, and with what cash flow.