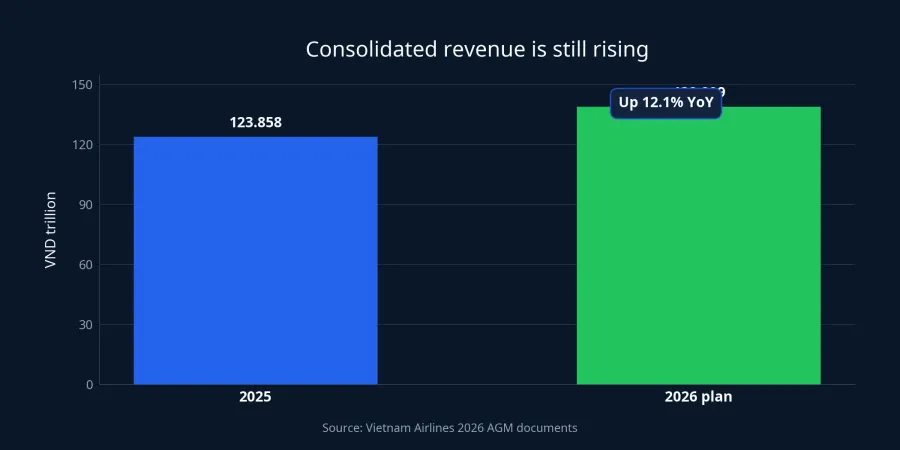

Vietnam Airlines is heading into 2026 with a contradiction that can easily mislead newer investors. At the top line, the carrier is targeting VND 138,899 billion in consolidated revenue, up 12.1% from 2025. At the bottom line, consolidated net profit is planned at just VND 22 billion.Vietnam Airlines

That is not a minor accounting detail. It says scale has come back, but earnings quality is still fragile. For an airline, a large revenue base matters less than how much survives after fuel, aircraft leases, maintenance, and FX costs run through the model.

Traffic is back, and the operating base is larger again

The easiest part of the recovery to see is volume. Vietnam Airlines expects to carry 27.73 million passengers in 2026, up 8.1% from 2025. International passengers are projected at 9.8 million, up 13.4%, while domestic traffic is expected at 17.93 million, up 5.5%.Vietnam Airlines

The base year was not weak. In 2025, the airline carried 25.65 million passengers, up 11.7% from 2024 and 1% above plan. Consolidated revenue reached VND 123,858 billion, beating the initial target by 6.1%.Vietnam Airlines

That matters because it confirms part of the recovery story is real rather than narrative-driven. International routes are broadening again, cross-border travel demand is still improving, and management is planning additional services to Copenhagen, Amsterdam, and selected destinations in Southeast Asia and South Asia.Vietnam Airlines

But airline stocks do not move on passenger growth alone. A carrier can fly more seats and sell more tickets while still producing weaker earnings if input costs rise faster than revenue. That is why investors need to separate two questions: how far operations have recovered, and how durable the profit stream has become.

The real bottleneck is cost pressure, not demand

Vietnam Airlines' AGM materials make the biggest variable clear: fuel. In 2025, average Jet A1 prices came in at USD 86.75 per barrel, USD 2.14 above plan, adding roughly VND 660 billion to fuel costs from pricing alone. Fuel currently accounts for about 30% of total operating costs.Vietnam Airlines

The 2026 planning assumption is much heavier. The airline built its budget around an average jet fuel price of USD 128.54 per barrel, up USD 41.79 from the 2025 realized level, or roughly 48%. On fuel prices alone, excluding traffic and FX effects, incremental costs could reach VND 11.9 trillion versus the prior year.Vietnam Airlines

That said, fuel is not the only driver, and it would be too neat to frame the entire margin story around oil. The same documents also cite pressure from aircraft lease rates, spare parts, repair and maintenance costs, supply-chain disruptions, and engine recalls. Fuel is the largest variable, but not the only one shaping the earnings outcome.Vietnam Airlines

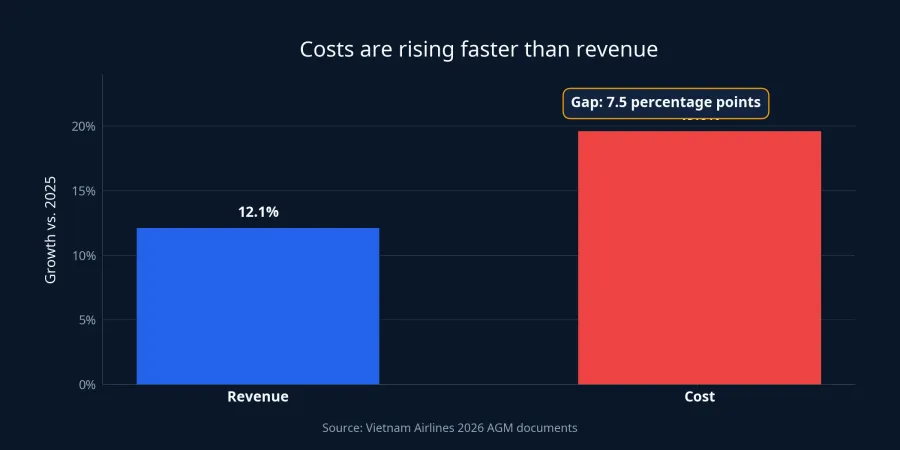

Put the two layers of data side by side and the mismatch becomes obvious. Consolidated revenue is planned at VND 138,899 billion in 2026, up 12.1%. Consolidated costs, however, are expected to reach VND 138,389 billion, up 19.6% from 2025.Vietnam Airlines

That is the part many first-time investors miss when they see a large revenue headline. If costs rise faster than revenue, most of the improvement at the top line gets absorbed before it ever reaches profit. An airline can look busy operationally and still leave shareholders with a very thin earnings year.

The profit plan is so thin that the safety cushion is close to zero

Vietnam Airlines is targeting VND 510 billion in consolidated pre-tax profit for 2026, but only VND 22 billion in consolidated net profit. That is a sharp contraction from 2025, when the group posted VND 8,168 billion in consolidated pre-tax profit and VND 7,607 billion in consolidated net profit.Vietnam Airlines

VND 22 billion is effectively breakeven at group scale. That does not mean the business is falling back into the crisis conditions of the past few years. A better reading is that the recovery still lacks enough earnings thickness to absorb a meaningful cost shock. Even a modest move in fuel, FX, or lease costs could materially change the year-end result.

In that sense, HVN still looks more like an ongoing restructuring story than a stabilized earnings growth story. With companies in that phase, investors cannot treat a single annual plan as proof that the hard part is over. What matters is whether profit stays positive after the peak season, when the full burden of variable costs becomes clearer.

Restructuring has reduced pressure, but it is not finished

The balance-sheet section of the documents is more constructive. Vietnam Airlines said it completed the first phase of its equity raising by the end of September 2025, adding VND 8,971 billion to charter capital and cash resources. In 2025, it also disbursed VND 1,522 billion from that capital increase.Vietnam Airlines

Another notable point is that, by the end of 2025, the airline said it no longer had short-term commercial borrowings and had largely repaid overdue supplier balances under the agreed schedule. For an airline, that matters more than the optics of revenue growth, because weak liquidity can derail operations even when demand is recovering.Vietnam Airlines

Still, calling the restructuring complete would be premature. Vietnam Airlines has set 2026 development investment spending at VND 5,228.7 billion, including VND 2,709.8 billion for aircraft investment alone. The airline is also continuing documentation for a 20-30 wide-body aircraft program for 2031-2035 and a plan to lease 12 wide-body aircraft for 2028-2030.Vietnam Airlines

That is why two ideas need to coexist. Liquidity is clearly healthier than it was at the worst point of the downturn. But capital needs for fleet renewal, together with a still-heavy operating cost structure, are large enough to keep profit vulnerable if the input environment turns less favorable.

What investors should watch in HVN

HVN closed at VND 23,000 per share on June 26, implying a market capitalization of about VND 71.6 trillion. That suggests the market is not valuing the company on VND 22 billion of planned 2026 profit alone. Investors are also paying for its flag-carrier position, network scale, and a longer recovery runway tied to international travel. These market figures were cross-checked from Investify's internal database.

The more useful way to read the stock is through three layers. First comes traffic: international passengers, load factor, ticket revenue, and route expansion. Second comes margin: fuel, FX, lease costs, and aircraft maintenance. Third comes the balance sheet: cash flow, fleet investment pressure, and whether the company can maintain its no-short-term-commercial-debt position.

The clearest takeaway from the 2026 plan is that Vietnam Airlines has regained scale, but not the same degree of earnings resilience. This is not a weak-revenue story. It is a story of profits that remain highly sensitive to input costs. The signals worth tracking over the next few quarters are whether consolidated costs stay near the VND 138,389 billion plan, whether jet fuel cools versus management assumptions, and whether profit remains positive after the peak season. Those variables, more than passenger growth alone, will show whether HVN's recovery is turning into a more durable earnings profile.