At first glance, the latest news on State Treasury deposits looks like a straightforward positive for Vietnamese bank stocks. That reading is tempting, but it moves too fast. What the market has actually received is not a monetary easing decision. It is a policy instruction to study whether Treasury deposits can be used more flexibly to support short-term banking-system liquidity.Tuổi Trẻ

That distinction matters. There is a wide gap between “could provide support” and “has already injected liquidity.” The core thesis here is narrower: Treasury deposits may create extra technical headroom for some banks, but only if the proposal becomes an operational rule, and even then the effect remains constrained by exchange-rate pressure.

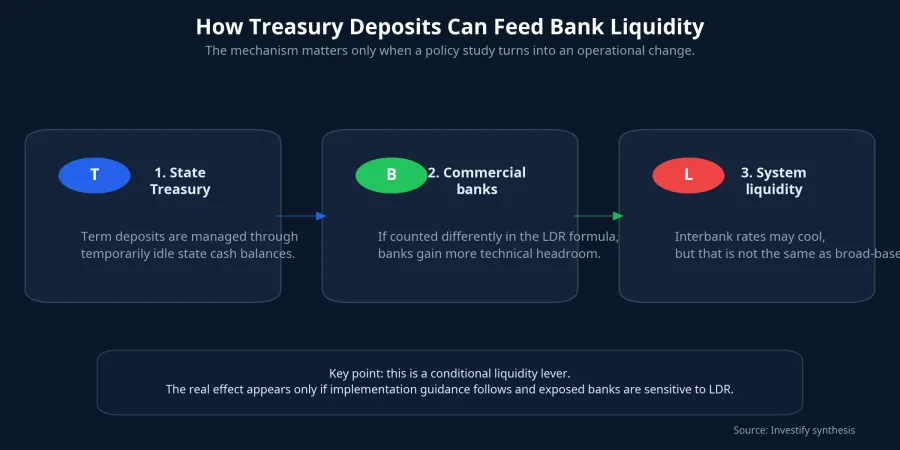

What Resolution 168 actually says

The key passage in Resolution 168/NQ-CP dated June 27 asks the State Bank of Vietnam to continue studying whether a higher share of term deposits from the State Treasury held at commercial banks can be counted in mobilized funding. The resolution also tells the Ministry of Finance and the SBV to coordinate Treasury deposits at commercial banks to support short-term funding for the economy.Tuổi Trẻ

The operative phrase is “continue studying.” That means policymakers have opened a path, not issued an immediately effective formula. The same resolution also allows the Ministry of Finance to decide deposit-allocation limits, including cases above 50% of temporarily idle state cash balances, in order to deepen coordination between fiscal and monetary policy.Tuổi Trẻ For newer investors, the cleanest way to frame this is as a more flexible short-term allocation mechanism, not a promise that funding will suddenly become cheaper across the board.

Why the mechanism runs through LDR

To understand the equity angle, investors need to return to the loan-to-deposit ratio, or LDR. When a bank’s lending grows too close to the amount of deposits counted as eligible funding, the bank loses room to expand credit unless it raises deposits, changes its funding mix, or benefits from a technical adjustment in the formula. In other words, the same amount of real money in the economy can produce different lending headroom depending on how the denominator is defined.

The current framework already contains that technical foundation. Under Circular 08/2026/TT-NHNN, effective from May 15, 2026, demand deposits from the State Treasury are still excluded from total deposits for LDR purposes, while 80% of term deposits from the Treasury are also excluded. Put differently, banks can currently count 20% of Treasury term deposits in the LDR denominator.

That is precisely why Resolution 168 is worth watching. If the ratio is adjusted further, some banks could gain extra technical breathing room without waiting for a rise in household or corporate deposits. This is better understood as a change in liquidity management math than as a magic source of new money.

Why this is not the same as a rate cut

Many retail investors instinctively group any liquidity-support story under the same easy-money label. That shortcut usually leads to poor conclusions. A policy-rate cut affects funding costs and valuation frameworks much more broadly, while a change in how Treasury deposits are counted in LDR would move through a much narrower channel.

The first channel is the interbank market. The second is credit capacity, but that only becomes meaningful for banks that are both sensitive to LDR and large enough holders of Treasury deposits for the recalculation to matter. The third is stock-market sentiment, where investors often react to the story first and ask later where the measurable benefit actually sits.

Three scenarios for the coming week

The first scenario is that the proposal remains under study. If the resolution is not followed by a draft amendment, new guidance, or a more specific operating signal, the immediate effect is likely to be psychological. The second scenario is that implementation signals start to appear, from a draft formula change to clearer detail on Treasury deposit limits. If that happens, the more direct winners would probably be banks whose LDR constraints are tighter and whose Treasury-related deposits are large enough to matter.

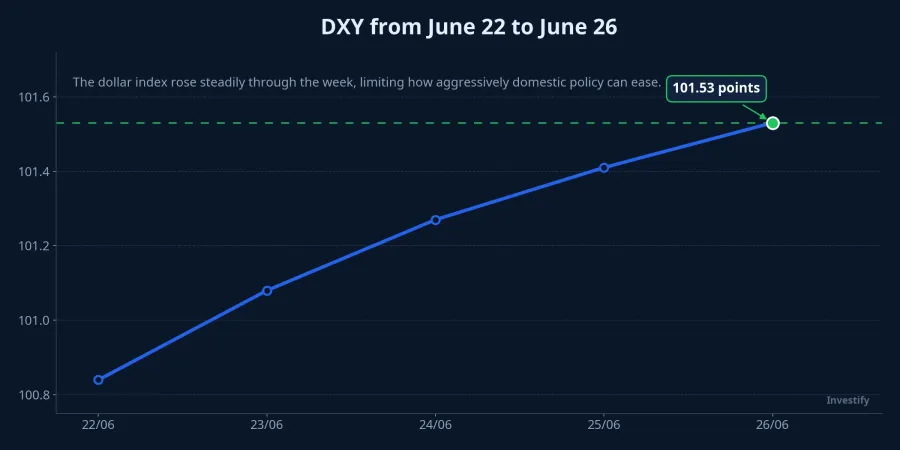

The third scenario is that policy support emerges while exchange-rate pressure continues to act as a brake. DXY closed at 101.53 on June 26, up from 100.84 on June 22. On the same day, USD/VND stood at VND 26,316 per dollar. As long as the US dollar remains firm, the SBV’s room to signal aggressive easing is still constrained.

Not every bank stock benefits equally

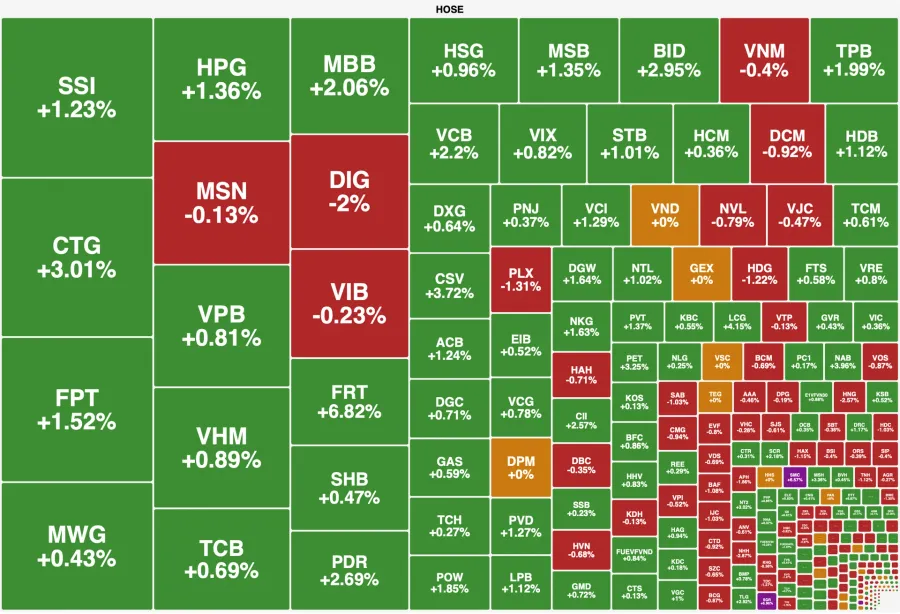

This is the point newer investors miss most often. A liquidity-support headline does not mean the entire banking sector should trade higher together. Market flows rarely distribute themselves so evenly. The transmission mechanism is layered, and the effect depends on funding structure, LDR sensitivity, and each bank’s ability to turn technical headroom into real credit growth.

State-owned commercial banks are the most obvious names in this conversation because of their systemic role and their potential exposure to Treasury deposits. But the real question is not simply which bank gets more money. It is which bank actually needs more room, because if LDR is not the binding constraint, the technical adjustment may matter far less than the market hopes.

If bank shares rally next week, it would still be premature to say the move came entirely from the Treasury-deposit story. Money flows could also be responding to second-half credit expectations, to upcoming second-quarter earnings, or simply to a rotation into large caps that can support the index.

A green index does not guarantee a green portfolio

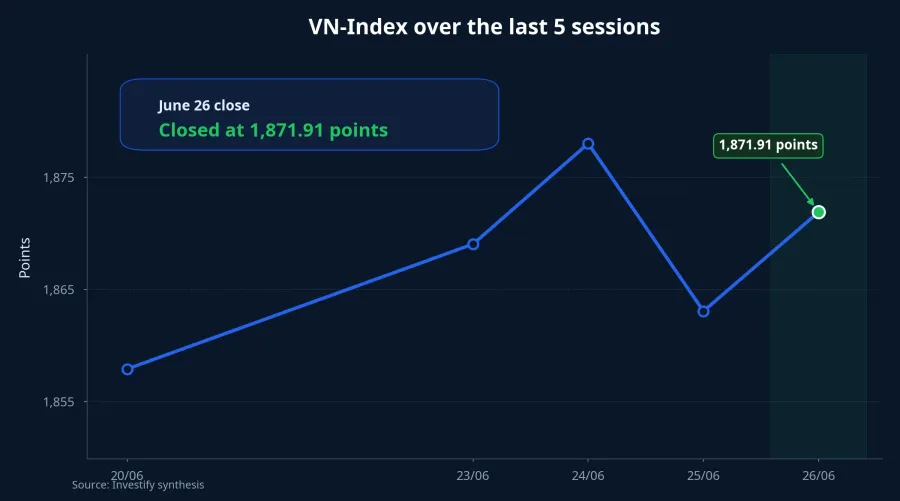

VN-Index closed at 1,871.91 on June 26, up 0.47% in the final session of the week. That does not automatically mean market breadth improved evenly. If money flows concentrate in a few large bank names, the index can still look healthy while much of the board remains mixed.

The screen itself tells the same story: plenty of green may be visible, but it is not evenly spread across sectors or individual stocks. System liquidity support does not mean every listed bank or every stock on the board receives the same valuation reward.

The most disciplined way to read this

From a policy perspective, Resolution 168 shows that the government wants tighter coordination between state cash management and the banking system through the rest of 2026. From a market perspective, this is a conditional support factor for liquidity, not a confirmation that a broad cheap-money cycle has returned.

The most coherent conclusion, then, is a narrow commitment: Treasury deposits could open more technical room for some banks, but that is still not enough to treat the move as a system-wide monetary pivot. The watch list for the next two weeks is fairly clear: does new guidance appear, does the market identify which banks are actually affected, and do DXY and USD/VND cool enough for this support to have a stronger effect.