One number from last week was almost designed to make retail investors feel better: foreign investors were net sellers by only about VND 213.2 billion across the market in the Jun 22-26 week, down more than 92.5% from the previous week.ĐTCK On the surface, that looks like a clean signal that a major source of pressure is fading.

But a lighter seller is not the same thing as a committed buyer. In equity markets, the headline flow number only tells part of the story. The more important question is where the money is going and whether it is spreading across the market. When an index rises mostly because a handful of very large stocks are doing the heavy lifting, the tape can look healthy while many portfolios still feel stuck.

That is the core thesis for the new week: easing foreign selling is constructive, but the rebound is still too narrow to call broadly healthy. For that judgment to change, investors need to see participation widen beyond a small cluster of heavyweight names.

Less foreign selling helps, but it does not settle the case

According to Đầu tư Chứng khoán, foreign investors were net sellers of about VND 213.2 billion in the Jun 22-26 week, versus roughly VND 2,860.2 billion in the prior week.ĐTCK In raw terms, that is a meaningful improvement. For first-time investors, it matters because it suggests at least one major headwind has become less intense.

Still, the number only tells us that selling pressure has eased. It does not prove that foreign risk appetite has returned to the entire market. If an investor has been unloading aggressively and then slows down, that is better than before, but it is very different from saying that investor has started buying broadly and consistently again.

On the final session of the week, foreign investors also returned to net buying on HOSE by more than VND 332 billion.VietnamPlus That matters for sentiment after a period when many local traders had grown used to seeing foreign money as a steady source of selling. But for sentiment to become evidence, the buying needs to persist and it needs to broaden.

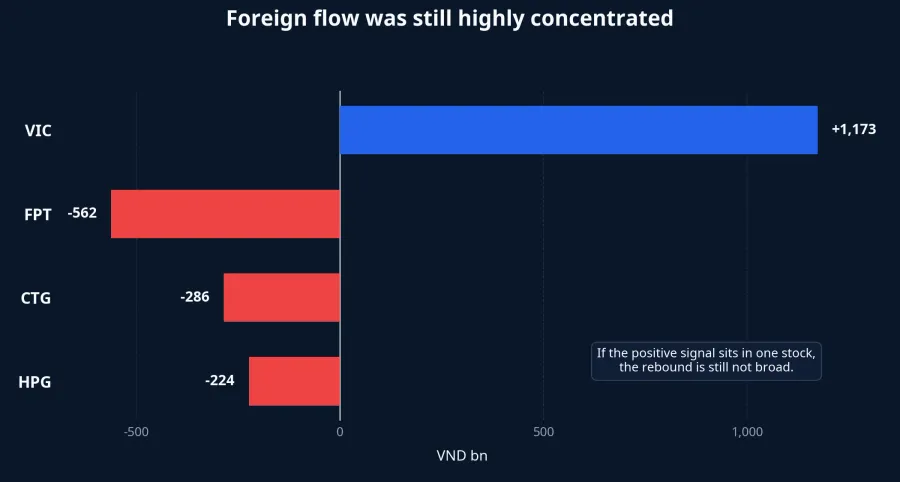

Where the money went matters more than the total

The most revealing part of last week was the internal structure of those flows. VIC was the biggest net-buy stock at about VND 1,173 billion. On the other side, FPT saw net selling of roughly VND 562 billion, CTG about VND 286 billion, and HPG about VND 224 billion.ĐTCK

In plain terms, foreign money did not disappear, but it did not spread evenly either. A large share of the constructive signal sat in one very specific place: VIC. Several other familiar large-cap names were still seeing capital leave. For newer investors, that distinction is critical. A market being re-accumulated broadly is very different from a market being propped up by one or two standout names.

That is also why this should not be read as a single-stock story about VIC or VHM. The real issue is not that one stock attracted strong buying. The issue is what happens to the rest of the market when the positive signal is concentrated that tightly. The broader list still has to prove it can follow.

A green index is not the same as a green market

The Jun 26 session was a clean example of the trap in reading the market through the index alone. VN-Index closed at 1,871.91, up 8.84 points or 0.47%. VietnamPlus noted that VIC and VHM were the biggest contributors, adding nearly 10 points to the benchmark on their own.VietnamPlus

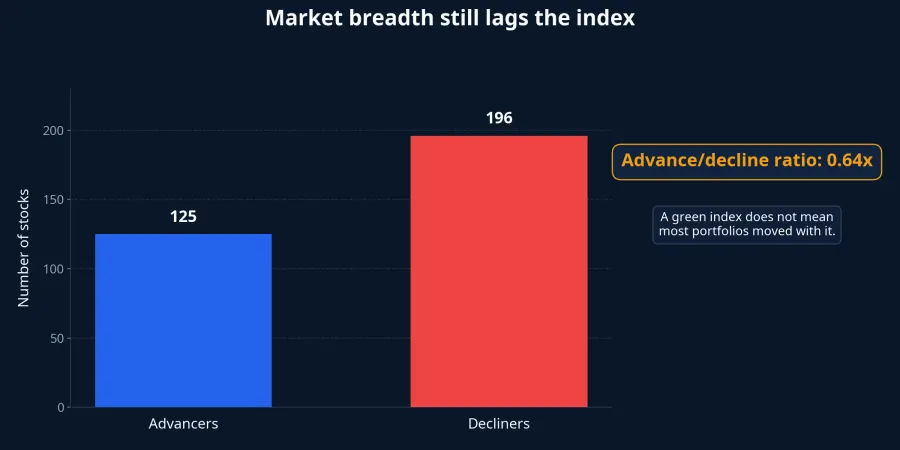

If all you see is the line that says “VN-Index rose,” it is easy to assume the market is improving in a fairly even way. Breadth says otherwise. Investify’s internal data showed 125 advancers versus 196 decliners in the Jun 26 session. VietnamPlus, using a broader market count, also reported that decliners still outnumbered advancers, at 412 versus 325.VietnamPlus

The scopes are different, but the message is the same: the index’s green finish did not represent most stocks. That is why many first-time investors often feel confused in the early stage of a rebound. The news says the market went up, but their account is flat or still red. There is no contradiction. A market-cap-weighted index is built to reflect the pull of the biggest companies, so when the leaders rise faster than the rest, the benchmark will recover before the average portfolio does.

The new week should be judged by breadth, not just by points

In a rebound that is still narrow, investors do not need to guess with emotion. There are three practical signals to watch right on the screen. First, do advancers start outnumbering decliners for several sessions in a row? One green session powered by a few leaders is not enough. What the market needs is repeated participation across more groups.

Second, does the list of point contributors expand beyond the ultra-large caps? If banks, brokers, steel, retail, or technology names start taking turns supporting the index, the rebound will have a broader base. If the benchmark still depends on a very small leadership cluster, the market will remain vulnerable whenever that cluster cools off.

Third, how do foreign investors trade in the first few sessions of the new week? Continued net buying would be more convincing if it stops being concentrated in a single stock. Markets that are genuinely getting healthier tend to show fresh money appearing in several places at once, even if not at dramatic levels. If the positive signal remains isolated, the more disciplined conclusion is that selling pressure is easing, not that broad participation has arrived.

Conclusion: Better tone, but not broad health yet

Easing foreign selling is real progress and it deserves to be acknowledged as such. But the data still does not support an overly enthusiastic read. Foreign flows remained heavily concentrated, and market breadth still lagged behind the benchmark’s green finish.

The most coherent conclusion, then, is that this rebound is still in a proving phase. It can widen if money rotates into more sectors and if advancers begin to take the lead more consistently. If that does not happen, a green VN-Index will remain mostly a large-cap signal rather than proof that the broader market has regained strength.

The watch list for the opening sessions of the new week is therefore straightforward: breadth, leadership rotation, and whether foreign buying becomes less concentrated. If those three pieces improve together, “lighter foreign selling” can start to look like the foundation of a broader rebound instead of just a temporary relief signal.