Vietnam's domestic carbon exchange is scheduled to begin operating on June 29. For retail investors, this is not really about opening another account and trying to trade carbon credits from day one. The more important shift is that a cost once buried in sustainability reports and environmental disclosures is now moving into a market structure with clearer registration, custody, trading, and settlement rules.TBTCVN

Put simply, emissions are moving closer to a price board. Once that cost starts to generate observable reference prices, high-emitting companies will have less room to talk about environmental exposure in vague language. Investors, in turn, get another layer of information for re-reading margins, clean-technology capex, and valuation discounts across energy-intensive listed companies.

This Is More Than Green Messaging

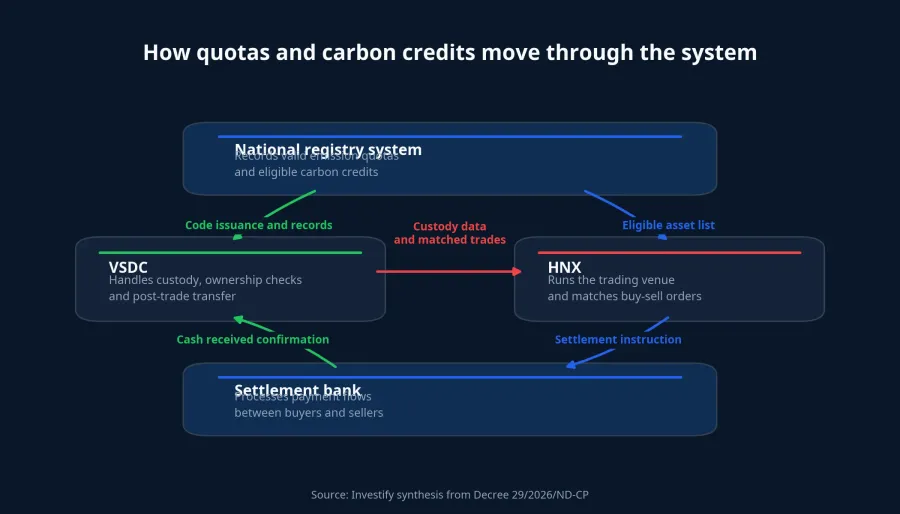

The legal framework is no longer at the proposal stage. Decree 29/2026/ND-CP took effect on January 19, 2026, setting out rules for domestic registration, coding, ownership transfer, custody, trading, and settlement for greenhouse-gas emission quotas and eligible carbon credits.Báo Chính phủ

For retail investors, the important point is that the infrastructure sits inside familiar financial-market plumbing. HNX runs the trading venue, while VSDC handles custody and settlement; on June 22, the relevant parties signed cooperation agreements covering data exchange, disclosures, supervision, and incident handling ahead of launch.VietnamPlus

The decree also makes clear that this is not a promise-based market. Participants may use only one securities trading account with a carbon trading member; they must have sufficient cash before placing a buy order, and enough quotas or carbon credits before placing a sell order.Báo Chính phủ That sounds technical, but the investment takeaway is straightforward: emissions costs are being pulled out of the gray zone and into a system backed by actual assets and actual cash movements.

Which Groups Come Under Scrutiny First

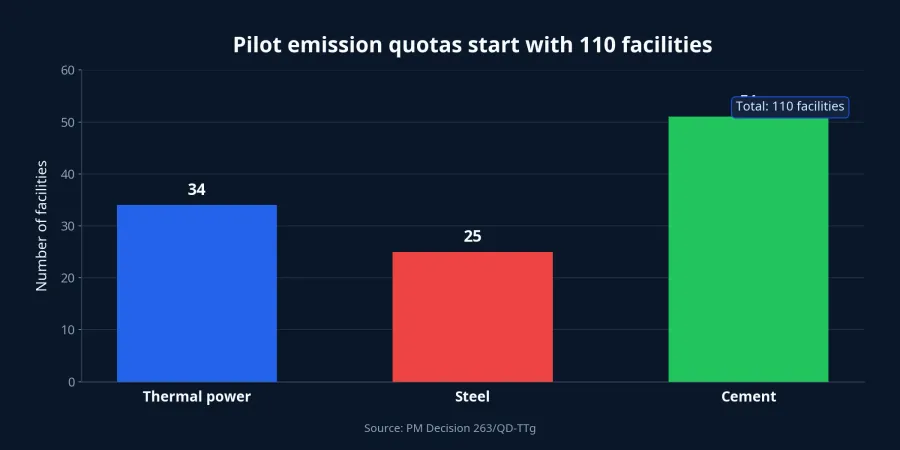

Not every listed company will feel the impact in the same way during the opening weeks. The Ministry of Agriculture and Environment has already made pilot quota allocations to 110 facilities ahead of the exchange launch, and another report says those 110 largest facilities account for about 40% of the country's direct emissions.TBTCVNBáo Đầu tư

The practical way to frame this is to start with sectors that are both emissions-heavy and already inside the pilot phase. Prime Ministerial Decision 263/QD-TTg allocates quotas for 34 thermal-power plants, 25 steel production facilities, and 51 cement plants in the 2025-2026 pilot period.Báo Chính phủ In stock-market terms, those are the same clusters investors already watch through output, pricing power, coal, electricity, and public-investment demand.

What investors should avoid is jumping too quickly from “high-emission sector” to “bad stock.” The evidence so far supports a narrower conclusion: companies in these groups will face stronger pressure to disclose compliance costs more clearly. The actual profit impact will vary by company, depending on whether emissions sit below quota or above it, whether the firm has excess allowances to sell or deficits to buy, and how far it has already invested in cleaner technology.

That means the impact is more likely to be stratified than uniform. Two cement names can sit in the same industry while facing very different carbon-cost pressure if one runs a newer, more efficient line and the other still relies on older processes. Once the market has a visible mechanism for carbon costs, the valuation gap between those firms can widen even if both still report acceptable current earnings.

How Carbon Costs Reach the Income Statement

For newer investors, the practical reading is not to guess the day-one carbon price. New markets usually need time to develop enough liquidity, enough counterparties, and enough transaction history to produce a reliable reference price. In the early phase, the more useful question is whether companies begin disclosing quotas, compliance costs, and decarbonization capex in a more concrete way.

The first transmission channel is cost of goods sold. If a steel, cement, or thermal-power company has to buy additional quotas because its emissions exceed its allocation, that expense will eventually pressure margins. The only real buffer is pricing power or a faster emissions-reduction path than peers.

The second channel is capital spending. Once carbon costs become tradable, management teams face a familiar corporate-finance trade-off: spend upfront on cleaner technology, or accept a higher compliance bill later. For long-term investors, that makes capex plans, equipment upgrades, fuel switching, and energy-efficiency programs more informative than broad sustainability slogans in annual reports.

The third channel is valuation. Two companies may post the same current earnings, but the one with lower emissions intensity could deserve a better valuation multiple once the market starts treating carbon as a real input cost. By contrast, a company with strong headline profits but heavy dependence on emissions-intensive technology may deserve a deeper discount because investors worry those earnings do not yet fully reflect the environmental bill of future years.

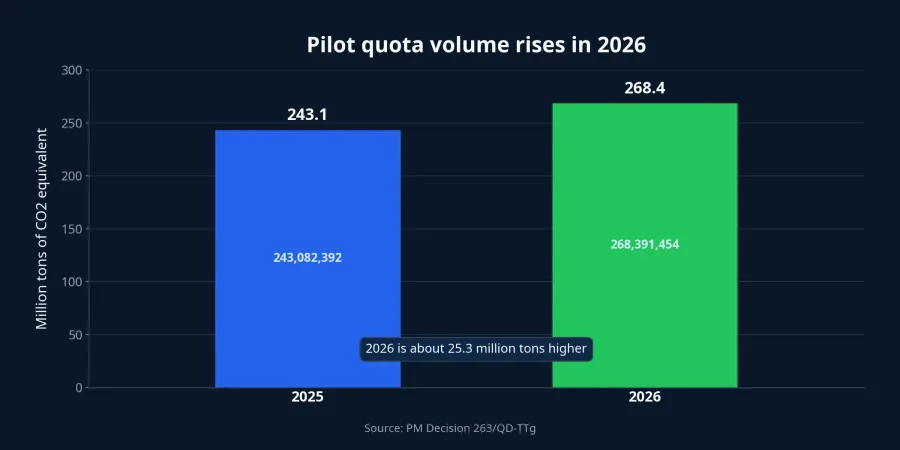

The pilot allocation is also large enough that this should not be dismissed as a communications exercise. Total pilot greenhouse-gas quotas stood at about 243.1 million tons of CO2 equivalent in 2025 and rise to about 268.4 million tons in 2026.Báo Chính phủ Once a market of that size begins to generate reasonably usable price signals, the way investors read profits in emissions-heavy sectors is likely to change.

What Retail Investors Should Watch After Launch

The first signal is actual trading data, not launch-day noise. If the market quickly discloses what instruments traded, how many orders were placed, who sat on each side of the market, and where reference prices formed, the story moves from infrastructure to real cost transmission. If the initial phase is mostly ceremonial, investors should treat it as a market that has completed only its first step.

The second signal is disclosure quality at the company level. Past policy cycles in Vietnam have shown that firms willing to publish details early often help the market price risk more calmly. In interim reports and management commentary from emissions-heavy issuers, retail investors should look for very specific answers: how much quota was allocated, how much has already been used, how any shortfall will be handled, and what investments are meant to reduce emissions intensity per unit of output.

The third signal is that the monitoring universe is already wider than many investors assume. Bao Dau tu reports that 2,166 facilities are currently required to report greenhouse-gas emissions, not just the 110 largest facilities that received pilot allocations in the first phase.Báo Đầu tư That means the emissions story will almost certainly extend beyond the first three pilot sector groups over time.

The core thesis here is straightforward: from June 29 onward, retail investors do not need to treat the carbon exchange as a new speculative product, but they should treat it as a new data layer for reading emissions-heavy stocks. The bigger risk is not missing an early trade. It is continuing to value companies as if emissions costs were still just a vague footnote at the back of a report. Over the next few weeks, the most useful signals will be the market's first reference prices and the transparency level of large emitters.