A VND 20 trillion bond plan naturally triggers an easy headline reaction: the bank is borrowing more money, so funding pressure must be rising. That reading is too shallow. In its June 26 disclosure, Sacombank did not simply say it would issue private bonds. It stated that the issuance was aimed at increasing Tier 2 capital.Sacombank

That distinction matters because banks do not operate like industrial companies. A manufacturer issuing bonds is usually judged by the project pipeline, cash generation and debt repayment profile. A bank issuing qualifying bonds also has to be read through a different lens: whether the proceeds strengthen regulatory capital, preserve capital ratios and create more room for risk-weighted assets, which in practice means more room for lending.

What Sacombank actually approved

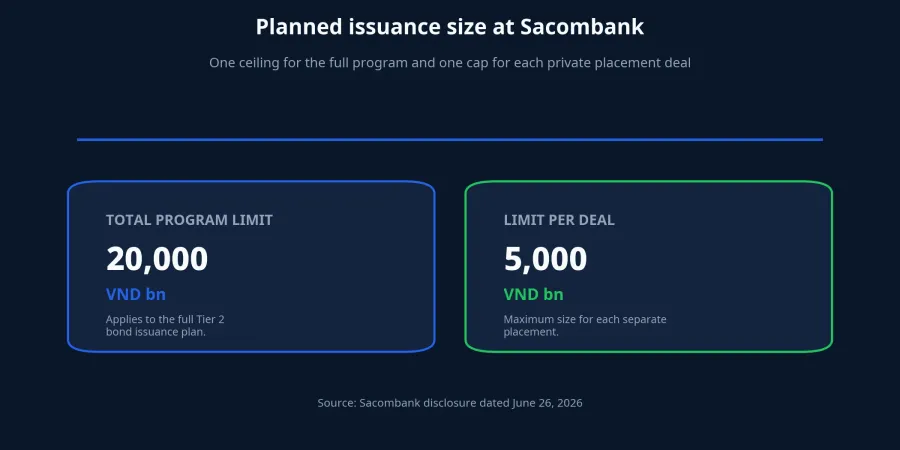

According to the June 26 disclosure, Sacombank approved a plan to issue private-placement bonds eligible for Tier 2 capital in 2026, with a maximum total value of VND 20 trillion and a cap of VND 5 trillion for each individual issuance transaction.Sacombank Those are the only fresh transaction figures that really matter in this story, and both come directly from a current official filing.

VietnamPlus reported that the bonds are expected to be privately placed with institutional professional securities investors, not offered as a mass-market product to ordinary depositors.VietnamPlus For retail readers, that is a useful first filter. A bank bond is not a savings account with a more attractive label.

The deeper point is not that Sacombank “needs money” in a generic sense. The deeper point is that it is trying to build an additional layer of capital that can count toward regulatory capital. Once you view the deal through that framework, the headline changes from “more borrowing” to “more balance-sheet capacity.”

Why Tier 2 capital matters

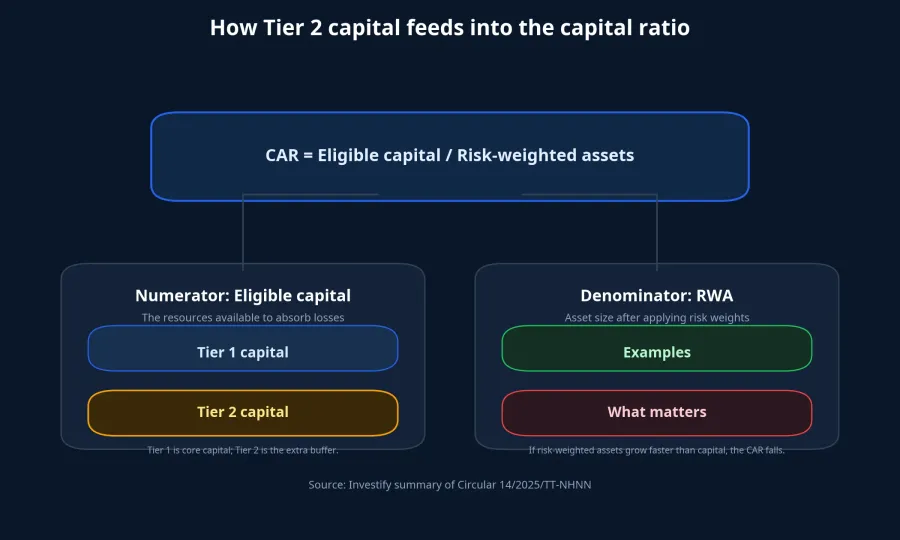

Under Circular 14/2025/TT-NHNN, commercial banks must maintain a minimum core Tier 1 ratio of 4.5%, a minimum Tier 1 ratio of 6%, and a minimum capital adequacy ratio of 8%.LuatVietnam These thresholds may sound technical, but they shape how much lending headroom a bank can preserve without stretching its risk buffer.

Put simply, the capital adequacy ratio compares eligible capital with risk-weighted assets. If the numerator grows, the bank has more shock absorption. If the denominator grows faster, usually because lending expands, the ratio comes under pressure. That is why deposit growth alone does not solve the capital question. A bank can be liquid enough in the short run and still need more Tier 2 capital if it wants to expand safely.

Tier 1 is the core layer, typically made up of charter capital and retained earnings. Tier 2 is a supplementary layer. Qualifying bonds can be included there, which is why they matter differently from plain deposits when investors look at a bank through the lens of capital adequacy.LuatVietnam

This is where newer investors often get tripped up. Deposits give a bank operating funding. They do not automatically improve regulatory capital. A Tier 2 bond issue can therefore make sense even when a bank does not appear short of cash at all. The issue is not immediate liquidity. The issue is balance-sheet resilience and capacity.

Why not issue shares instead

If the only goal were capital quality, new equity would usually look cleaner because it strengthens Tier 1 capital. But equity issuance comes with dilution. More shares mean the benefit per share can fall if profits do not rise quickly enough. Tier 2 bonds avoid immediate dilution, can be executed faster and are often easier to structure, but they create coupon obligations and eventual principal repayment.

That is why it would be wrong to frame Sacombank's plan as an unambiguously positive or negative event. For shareholders, it can be read as a sign that the bank is preparing capital capacity for the next growth phase. It is not, by itself, proof that profits will jump in the near term. The funding cost still has to flow through the income statement, and if returns on new assets do not exceed that cost by enough, shareholders gain a thicker buffer but not necessarily better economics.

VietnamPlus used the phrase “preparing for a growth phase.”VietnamPlus The sensible way to read that is as preparation for more balance-sheet capacity, not as automatic evidence of stronger shareholder returns. Moving from “more capital buffer” to “more shareholder value” still requires the bank to prove asset quality, margin discipline and effective capital deployment.

Bond buyers see the same news from another angle. They are not looking for earnings upside or valuation rerating. They are assessing repayment capacity and bond terms. Tenor, coupon, call features, payment seniority and exit liquidity all matter more than the comforting instinct that a large bank must therefore be a low-risk bond issuer.

Three products, three different risk ladders

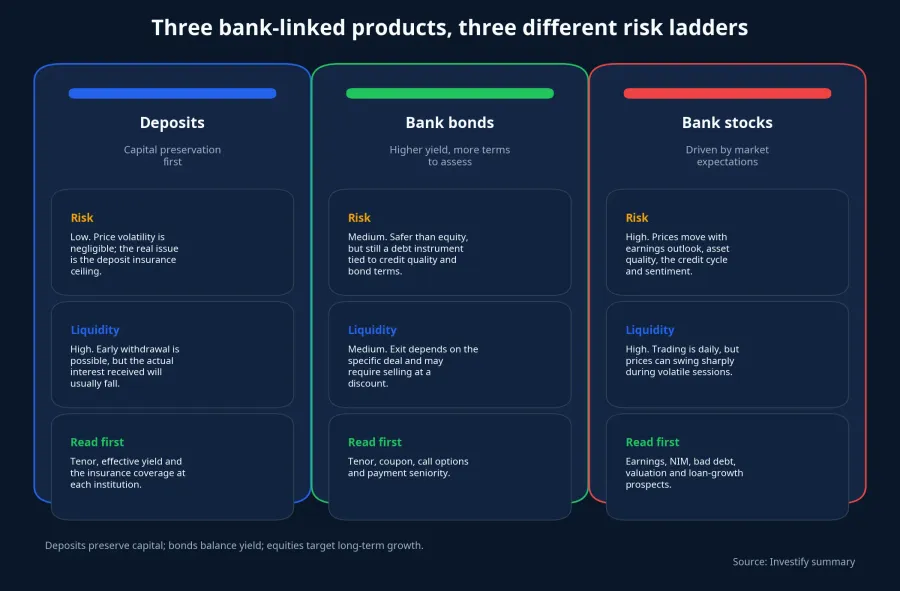

This is where the story becomes practical for retail readers. Deposits, bank bonds and bank stocks are not versions of the same product. They sit on different places in the risk stack, and confusing them usually leads to bad decisions about expected return and downside tolerance.

Under Decision 32/2021/QD-TTg, the maximum insured amount for all insured deposits held by one person at one participating institution is VND 125,000,000, including principal and interest.PBGDPL Deposits therefore come with a specific protection mechanism. Bank bonds do not rely on that mechanism. Bank stocks sit lower still in the stack because they represent ownership capital rather than debt claims.

Decree 200/2026/ND-CP also reiterates that a bond issuer borrows on its own account, repays on its own account and bears full responsibility for the effectiveness of capital use.Báo Chính phủ For investors, that should be interpreted very plainly: a bond is a contractual debt instrument, not a blanket promise of safety simply because the issuer is a recognizable financial institution.

Once you separate those three buckets, Sacombank's announcement becomes much easier to read. If you own STB shares, this is mainly a statement about capital structure, risk absorption and future lending capacity. If you are evaluating bank bonds, the real question is whether the bond terms compensate you for the credit and liquidity risks. If you are simply a depositor, this issuance does not transform your deposit into a bond and should not blur the distinction between the two.

The main takeaway for newer investors

The big picture is that Sacombank is using bonds as a capital tool, not merely as a funding tool. That is the central thesis that holds the entire story together. A planned issuance of up to VND 20 trillion says more about the bank's effort to reinforce its balance-sheet buffer before pushing further into growth than it does about any immediate earnings catalyst.Sacombank

For a newer investor, the disciplined way to read this news is to ask three follow-up questions. Which part of the balance sheet is being reinforced? How could the added funding cost affect future profitability? And where do you sit in the capital structure: depositor, bondholder or shareholder? Once those questions are clear, bank news becomes less intimidating and much more useful.