On June 22, LMH opened its first annual general meeting attempt with a result that reads almost unreal: not a single shareholder showed up. The company still had 1,847 shareholders on the May 25 record date, representing more than 25.6 million voting shares, yet attendance at the credential check stood at 0%.Vietstock

That is not just a strange anecdote from Vietnam's small-cap market. It is a clean lesson in what many new investors still overlook. A stock is not only a code flashing on a trading screen. It is a slice of ownership, and that ownership becomes passive very quickly if the person holding it never reads meeting materials, never shows up, never authorizes a proxy and never asks what management is actually proposing.

An empty room is a governance signal

The most useful way to read LMH is not as a curiosity, but as a pattern. Vietstock also reported that in both 2024 and 2025, the company had to call its AGM a third time before it could be held.Vietstock That matters more than the headline-grabbing 0% attendance on the first attempt this year, because it suggests the problem is not one bad morning. It points to a longer-running gap between the company and the people who legally own it.

For newer investors, this is where the signal needs to be read carefully. A failed first AGM does not automatically mean the company is uninvestable, and it does not create a buy or sell call on its own. What it does show is that the natural pressure mechanism inside a public company is getting thinner. When shareholders do not show up, management faces less direct scrutiny, and one layer of market discipline simply goes missing.

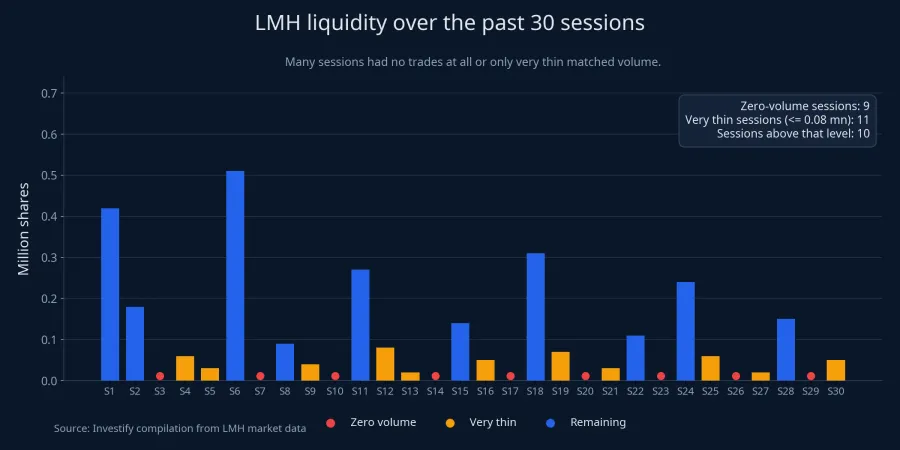

LMH's trading profile helps explain how that can happen. The stock is trading around VND 1,300 per share, and recent sessions have often shown almost no liquidity. When a name is both cheap and thinly traded, many holders stop treating it as active ownership. It starts to feel more like a forgotten position than a company they still need to monitor.

Why the first AGM can fail

Under Vietnam's 2020 Law on Enterprises, a first AGM can proceed only when attending shareholders represent more than 50% of total voting rights. If that threshold is not met, the company can call a second meeting, which requires at least 33% of voting rights unless the charter sets a higher bar. If that still fails, a third meeting may proceed regardless of the attendance ratio, unless the charter states otherwise.Chính phủ

This is why a failed first AGM does not mean the company is paralyzed for the year. The legal framework already anticipates weak attendance. But investors should not stop at the legal mechanism. The more important question is why the first round, where scrutiny is strongest and symbolism matters most, could not draw shareholders into the room.

Several explanations can coexist. Some investors may own too few shares to think the trip is worth their time. Some may have bought the stock long ago and no longer follow it. Others may not understand how proxy authorization works, so absence turns into total silence. None of those explanations proves misconduct on its own, but together they still produce the same outcome for minority investors: their oversight rights go unused.

That is the key point. The company may eventually move forward through later meeting rounds, yet small shareholders have already missed their clearest chance to hear management answer questions under direct pressure.

Small rights are still real rights

In plain terms, a common share usually comes with one vote. Common shareholders have the right to attend the AGM, speak, vote directly or through a proxy, receive dividends and review certain company materials under the law.Chính phủ A holder with a tiny stake cannot personally swing every resolution, but that is not the point. These rights still help investors understand how the business they own is being run.

This is often where first-time investors leave value on the table. They watch price moves, social-media narratives and next-quarter earnings expectations, while AGM materials feel dry and distant. In reality, AGMs are where many wallet-level decisions are laid out in plain sight: dividend plans, capital raises, ESOP issuance, related-party transactions, governance changes and business plans for the next year.

An additional share issuance can dilute ownership. A dividend plan reveals whether the company prefers to return cash or hold it back. A major investment proposal with weak justification tells its own story. None of this requires investors to be lawyers or accountants. The simple discipline of downloading the AGM documents and reading the key resolutions can offer a better risk filter than staring only at price candles.

AGM season is a practical governance test

The cleanest lesson from LMH is not "sell whenever an AGM room looks empty." It is also not "relax if the company eventually gets the meeting done." A better framework is to treat AGM season as a governance stress test. Did the company release materials early enough. Were those materials easy to find and detailed enough to be useful. Did the proposals explain the use of capital, profit assumptions and shareholder trade-offs clearly. Did management answer difficult questions directly, or hide behind generic language.

That test matters even more in illiquid names. When a stock barely trades, investors cannot assume they will exit smoothly at the price they want. When analysts, funds and mainstream media are not covering the company closely, retail investors cannot outsource the monitoring job to someone else. In that setting, an empty meeting room is not just about apathy. It also suggests that important corporate decisions may be passing with very little outside challenge.

The recent liquidity pattern at LMH underlines that risk. Many sessions posted zero matched volume or only very thin turnover. In a stock like this, the idea that you can "just sell if something goes wrong" is much weaker than it sounds. When you finally want to react, the bid side may not be there in enough size or fast enough to make that decision easy.

What first-time investors should do differently

The money implication is straightforward: the more you ignore shareholder rights, the more your investment process depends on other people doing the monitoring for you. Once you buy a stock, you are no longer just watching from the outside. You have become an owner, even if the stake is small. Owners should know what the company is asking for, what it is promising and how it responds when shareholders push back.

The first step does not need to be complicated. Check the AGM schedule of the companies you own. Download the meeting documents. Read the sections on business targets, dividends, capital raising and large transactions. If you cannot attend, check whether the proxy process is clearly explained. If a company makes it hard for shareholders to access materials, hard to participate or chronically unable to secure first-round attendance, that deserves a place on your governance watchlist.

The core thesis here is simple: AGM season is not a side ritual. It is one of the most practical screening tools retail investors have. LMH just makes that truth unusually visible. The lasting takeaway is not only the figure of 1,847 shareholders or the 0% attendance rate. It is the gap between being listed as an owner and behaving like one. For new investors who want to rely less on the randomness of price action, that is the gap worth closing first.