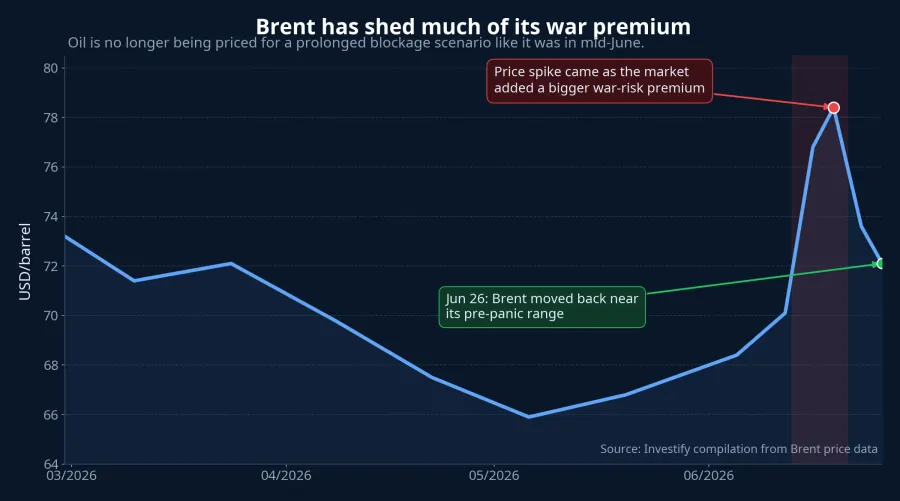

Brent has moved back near its late-February range. For newer investors, that made June 26 one of the more confusing sessions of the week: why did oil cool off while military headlines around Iran and the Strait of Hormuz were still coming in? August Brent settled at USD 71.99 a barrel, while WTI closed at USD 69.23.MarketWatch

The bigger picture is that oil does not trade on noise alone. It trades on the probability that physical barrels can still leave the Gulf and reach refiners on time. When the market believed a prolonged blockage was plausible, Brent had to carry a much larger war-risk premium. Once fresh evidence suggested flows were recovering, a large part of that premium came back out of the price very quickly.

Brent is not falling because the war story is over

The easiest mistake is to draw a straight line from conflict intensity to oil prices. The more important layer is whether tankers can still pass critical chokepoints, whether crude can still reach refineries on schedule, and whether buyers have to pay up for insurance or rerouting.

Internal price data show Brent near USD 70.84 a barrel on February 26. It then climbed to USD 112.57 on March 27 and touched USD 114.44 on May 4. That move reflected a market pricing the possibility that supply disruption could last long enough to materially reshape the balance in physical oil.

So Brent returning toward USD 72 a barrel on June 26 does not mean geopolitical risk has disappeared. It means traders are less convinced by the worst-case scenario: tension remains, but the system has not broken.

Hormuz is a flow story, not just a headline story

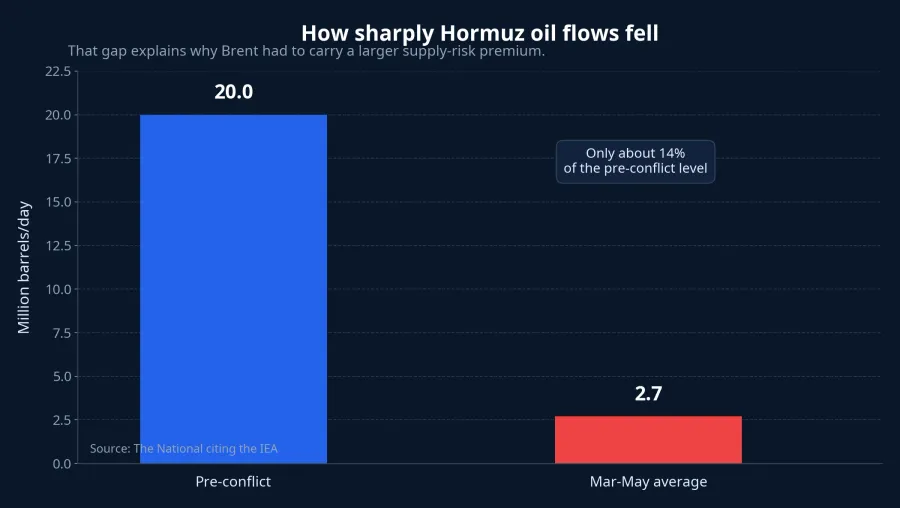

The Strait of Hormuz matters because it is the narrowest choke point for Middle Eastern oil. Before the conflict, the strait handled roughly 125 to 140 ship movements a day and carried about 20 million barrels of oil and refined products daily.Euronews At that scale, even a partial slowdown forces the market to add a transport-risk premium.

That also explains why oil can react far more aggressively than many first-time investors expect. In crude, the same headline can immediately raise questions about delivery schedules, freight costs, insurance, and alternative routes. Brent did not rise simply because the conflict looked uglier. It rose because the market feared barrels might not get where they needed to go.

What made the risk premium start to unwind

The key change this week was that the market saw evidence that oil was still finding a way out. The National, citing the IEA, reported that hydrocarbon flows through Hormuz fell from about 20 million barrels a day before the conflict to an average of 2.7 million barrels a day across March, April, and May.The National That collapse explains why Brent had carried such a large supply-risk premium in the first place.

The more important update was that UAE oil exports had recovered to nearly 85% of their pre-war level by early June, or roughly 4.3 million barrels a day, up from 1.9 million barrels a day in March.The National For commodity markets, that matters far more than one additional military headline.

Put more simply, the market is moving from asking, “Can oil get out at all?” to asking, “How slow is the exit route?” Once the odds of a full physical lock-up fall, the risk premium has to shrink, even if the region remains tense.

Euronews also said returning tanker traffic through Hormuz and progress in US-Iran talks helped steady market confidence. On June 24, Brent briefly fell below USD 74 a barrel for the first time since the Iran war began in late February.Euronews The market is not saying risk is zero. It is saying risk is no longer large enough to justify the same elevated price floor.

Why fresh military news has not fully reversed the move

MarketWatch reported that oil rose in after-hours trading after the US confirmed a retaliatory strike on Iran following an attack on a merchant vessel passing Hormuz. Even so, crude still finished lower during the main June 26 session and posted its third straight weekly decline.MarketWatch That is a sign the market no longer responds to every military development with the same intensity seen earlier in the crisis.

For newer investors, this is where short-term price action can be misleading. Oil can still jump for a few hours after an attack, especially if the headline lands late in the session. But for Brent to resume a durable uptrend, new information has to change assumptions about transport or output. If it does not stop ships, cut exports, or accelerate inventory drawdowns, the move can fade quickly.

That is why the central thesis here is straightforward: Brent is still priced for risk, but no longer for a prolonged blockage scenario. Unless the market sees fresh evidence that physical flows are turning down again, the war-driven upside is unlikely to fully rebuild.

The spillover into Vietnam comes with a lag

In Vietnam, retail fuel prices do not move tick for tick with Brent. After the June 25 price adjustment, E5 RON 92 in Zone 1 stood at VND 19,350 per liter, down VND 770 from the previous period, while 0.001S-V diesel stood at VND 23,960 per liter, down VND 1,470.Lao Động Those numbers already reflect Vietnam’s pricing mechanism, taxes, import lags, and domestic adjustment schedule.

What matters more for investors is that when Brent sheds part of its risk premium, imported inflation pressure also starts to cool over time. Expectations around transport costs, input inflation, and pressure on consumer-facing sectors become less intense. For first-time investors, that is a much more useful framework than trying to infer tomorrow’s pump price from one session in Brent.

Oil stocks will keep moving on different drivers

Another common mistake is to assume lower oil automatically means the entire Vietnamese oil and gas sector weakens for the same reason. Internal market data show that from June 22 to June 26, PVS fell from VND 39,600 a share to VND 37,500, BSR dropped from VND 26,400 to VND 24,250, and PLX slipped from VND 38,650 to VND 36,800. Sentiment clearly softened as Brent cooled, but the earnings transmission mechanism is not the same across the group.

For oilfield service names, investors tend to focus on upstream project timing and oil-price expectations. For refiners, the discussion also runs through crack spreads and inventory values. For fuel retailers, the story is more about end demand and the domestic pricing cycle. They may sit in one sector on the board, but they are not priced off the same profit story.

What to watch over the next two weeks

The most important signal remains physical flow. If tanker traffic through Hormuz keeps improving, Gulf exports hold their recovery, and freight costs do not spike again, Brent has room to stay near a range where much of the war premium has already been removed. For Vietnam, that would mainly feed through as softer inflation expectations and less overheated sentiment toward oil-related stocks.

The opposite scenario is still worth monitoring. If a new incident pushes tankers away from Hormuz again, drives freight costs sharply higher, or blocks more Gulf exports, the latest decline may prove to be only a technical pullback. Current evidence does not support that as the base case, but it remains the key risk because Brent reacts very quickly when physical evidence turns.

The conclusion is fairly simple. In the week of June 26, the market was not declaring the conflict over. It was only saying traders were less willing to pay for a prolonged blockage scenario. For newer investors, that is the distinction that matters most if they want to read oil correctly, understand how the story reaches Vietnam, and avoid chasing fear after much of that fear has already been priced out.