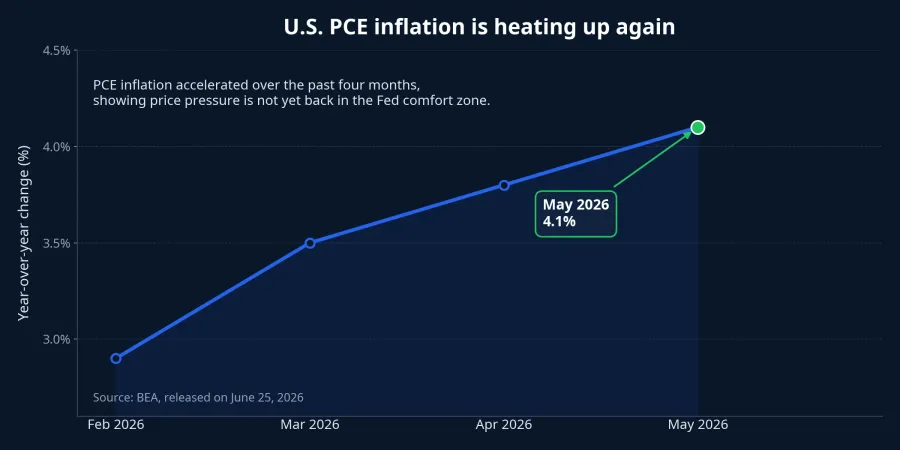

U.S. PCE inflation rose 4.1% year over year in May, the highest reading in the past four months and the first return to that zone in years.BEA For new investors in Vietnam, this is not the kind of headline that should lead straight to “stocks must fall,” “gold must rise,” or “the exchange rate is about to break.” The real message sits elsewhere: this print changes how markets price the near-term path of U.S. rates, which in turn changes how investors should read the dollar, gold, and risk assets.

The first important point is that the U.S. market did not react in a one-way fashion. The 4.1% annual reading matched Wall Street expectations, while the 0.4% monthly increase came in below the 0.5% forecast. In the same session, the Dow and the S&P 500 each rose 0.8%, while the Nasdaq gained 0.9%, helped in part by Micron’s earnings and guidance lifting semiconductor names.MarketWatchBarron's In plain terms, the same inflation release can coexist with higher stock prices if investors decide the surprise is not large enough to overturn the earnings story.

What 4.1% actually tells investors

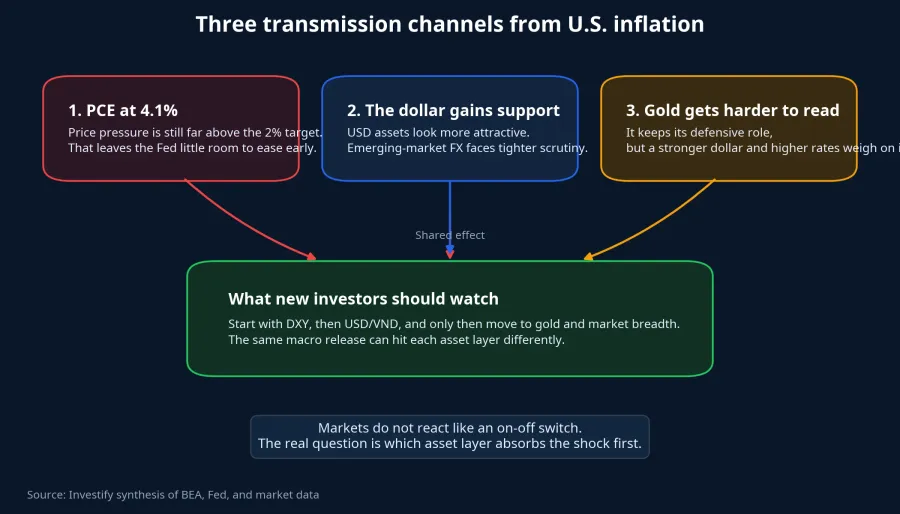

For a retail reader, 4.1% does not mean “the Fed will hike at the next meeting.” The better interpretation is simpler: if inflation is still far from the 2% target, the Fed has less reason to ease policy early. Once that expectation takes hold, the U.S. dollar is usually the first layer of the market to react, while gold and equities respond in different rhythms depending on the surrounding context.

Over the past four months, price pressure has been moving up rather than down. Core PCE, which strips out food and energy, also rose 3.4% in May. That matters more than a dramatic headline because it suggests inflation pressure is not only about short-term commodity swings, but also about the underlying trend.BEA

That is why one of the most common mistakes among new investors is turning a macro release into an absolute conclusion. Higher inflation does not automatically mean an immediate risk-off move across every asset. What it does mean is that the expected rate path becomes harder to bring down, and the cost of capital has to be repriced accordingly.

The Fed still has little reason to ease early

At its June 17, 2026 meeting, the Fed kept the policy rate in a 3.5% to 3.75% range and said inflation remained elevated relative to its 2% goal. That was an issued policy decision, not just a directional remark.Fed Set next to the fresh PCE release, it gives markets another reason to keep the “higher for longer” narrative on the table.

That does not mean the Fed will necessarily raise rates again. The more relevant issue is that the current rate range may stay in place longer than investors had hoped. For newer readers, the difference matters. One approach is guessing the next policy move. The other is understanding how global capital reprices when the easing timeline gets pushed back.

Mechanically, the transmission path is fairly clear. Hotter PCE pushes back easing expectations. That makes dollar-denominated assets more attractive. From there, gold enters a new tug-of-war, while risk assets have to live with tighter discounting. One macro shock, but not one identical market response.

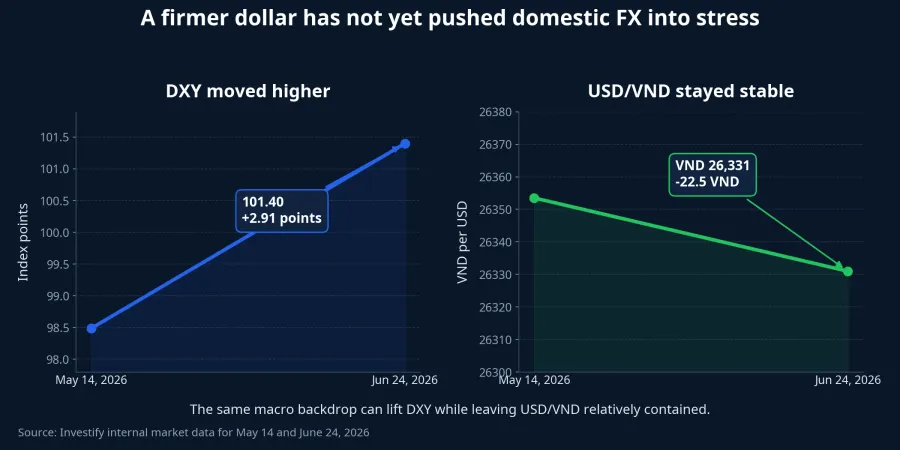

The dollar usually reacts first, but Vietnam’s FX has not flashed stress

DXY stood at 101.40 on June 24, 2026, up from 98.49 on May 14, 2026. That suggests the dollar has gained a firmer base as markets reassessed the U.S. rate outlook. For a beginner, this is the first layer worth checking after an inflation print because it captures macro expectations much faster than waiting for an equity screen to turn green or red.

But a firmer dollar does not automatically mean USD/VND has to jump into stress at once. Investify’s latest internal data shows USD/VND at VND 26,331 per dollar on June 24, 2026, not far from VND 26,353.5 on May 14, 2026. In other words, external pressure has appeared, but the domestic system is still absorbing it.

This is where new investors often overreact. They see the international dollar move higher and immediately assume domestic FX is about to enter a fresh stress phase. In reality, the two layers are linked but they do not always move at the same speed. When DXY rises while USD/VND stays contained, the right takeaway is not “there is no risk.” It is that the risk has not yet spilled into a clearly stressful domestic condition.

Gold is no longer a one-direction trade

International gold stood at USD 4,025.78 an ounce on June 25, 2026, well below USD 4,547.89 on May 15, 2026. That is a meaningful decline in magnitude, but not enough by itself to call a disorderly collapse because the move has not shown blanket panic. The more important point is the mechanism behind it: gold is being pulled by two opposing forces at the same time.

On one side, higher inflation helps gold preserve its defensive appeal for some investors. On the other, the same inflation pressure makes an early Fed rate cut less likely, which supports the dollar and real yields. When both forces are in play, buying gold simply because “U.S. inflation is above 4%” means missing half the story. Gold has not lost its role, but it has become harder to interpret cleanly.

This is also a useful example of causal discipline. If gold falls while inflation stays high, that is not enough to say “the market no longer believes in gold.” Part of the pressure may come from a stronger dollar. Another part may come from position trimming after an earlier run-up. The evidence in this article supports a two-way tug-of-war, not a single all-explaining cause.

Vietnam’s equities need to be read through breadth

The VN-Index closed at 1,863.07 on June 25, 2026, down 0.80%, with 115 gainers and 176 decliners. That matters because it reinforces a basic point: the headline index does not tell the whole story of money flow. A session with only a modest index decline can still be a session in which risk appetite is narrowing across smaller pockets of the market.

With U.S. inflation still outside a comfortable zone, Vietnam’s market may have to absorb another layer of external noise. But this layer does not work like an on-off switch. If domestic liquidity stays healthy and leadership groups keep their own earnings or industry narratives, the U.S. data may only show up as sharper market differentiation. If the dollar keeps its support while breadth deteriorates, the pressure will become more visible in assets that depend on long-duration capital and on risk appetite.

That is also why it is dangerous to copy Wall Street’s reaction directly onto Vietnam’s tape. Nasdaq’s gain on June 25 was helped by Micron, which means a company-specific catalyst was mixed into the macro story.Barron's The same principle applies to the VN-Index: the same global macro pressure can lead to very different outcomes depending on sector-specific stories and the quality of domestic liquidity.

Conclusion: The market reading map has changed

The main thesis here is straightforward: a 4.1% PCE print is not enough to call for a prolonged selloff across every asset, but it is enough to keep a floor under the dollar and make gold and rate-sensitive equities harder to read in the short run. Put simply, this inflation release does not hand investors a buy or sell order. It forces them to read the market in a better sequence.

The three signals worth watching over the next few sessions are:

- Whether DXY can hold its new range or fades as a short-lived post-data reaction.

- Whether USD/VND stays stable or begins to show clearer signs of strain.

- How the VN-Index moves relative to market breadth, especially in sessions where the headline index barely changes.

If all three deteriorate together, the market would be moving into a more clearly defensive state. If DXY cools off or USD/VND continues to absorb the pressure, the U.S. inflation data will likely matter more as a filter on capital allocation than as a broad risk-off trigger. That is the real value of the 4.1% print: it does not tell investors what to buy or sell, but it does tell them which layer of data to read first before jumping to conclusions.