Fast-growing export revenue is one of the easiest stories for investors to buy into. A company ships more, foreign demand holds up, the currency does not get in the way, and the order book looks healthy for the next few quarters. On the surface, that sounds like a clean growth case. But for exporters, revenue only captures the visible layer. The deeper question is whether the company can withstand a trade defense investigation once its products become large enough to draw scrutiny in overseas markets.

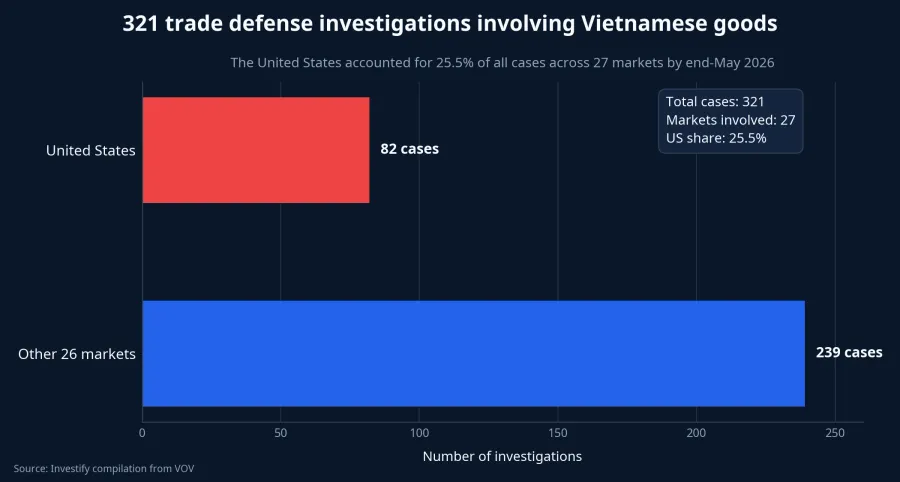

VOV, citing Vietnam's Trade Remedies Authority, reported that by the end of May 2026 Vietnamese goods had faced 321 trade defense investigations across 27 markets, with the United States alone accounting for 82 cases.VOV For retail investors, that changes how export stocks should be read. Revenue growth is no longer a straightforward positive. It is also a sign that a company has become more visible to regulators, trade lobbies and domestic producers in the importing country.

Why strong sales do not automatically mean safety

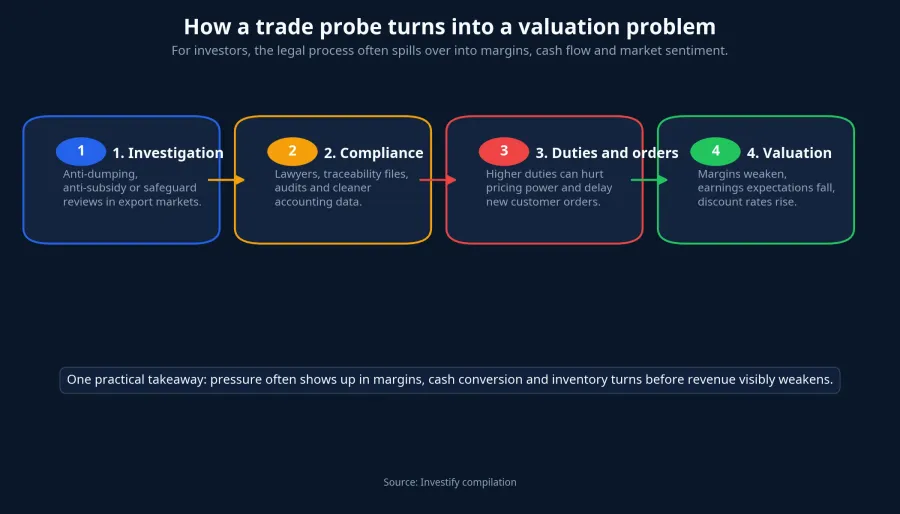

The simple version is this: export revenue tells you a company is selling, but it says almost nothing about how durable that market access really is when legal pressure rises. Anti-dumping, anti-subsidy and safeguard investigations do not move on the same schedule as quarterly earnings. They often surface precisely when a company is performing well, because rapid market penetration is what brings attention in the first place.

VOV noted that many investigations last 12 to 18 months, and some extend beyond three years.VOV During that time, the risk is not limited to the final tariff outcome. Exporters may have to pay for lawyers and consultants, clean up accounting records, prove origin, rework traceability files and live with customers delaying new orders until the process becomes clearer. In practice, pressure can hit margins well before revenue reflects the damage.

It would also be too simplistic to assign the entire wave of investigations to one single cause. There are at least three plausible drivers moving together: Vietnam's exports have expanded across more sectors, protectionist pressure in global trade remains elevated, and the range of products under review is widening beyond traditional industrial categories.VOV For investors, the key point is not which factor explains the biggest share. The key point is that the risk baseline for exporters has shifted.

The risk no longer stops with steel or chemicals

For years, many investors treated trade defense as mainly a steel, aluminum or chemical issue. That lens is getting outdated. VOV reported that the list of targeted products has expanded to agriculture, seafood, processed food, wood products, fruits, vegetables and plant-based goods.VOV That matters because sectors once seen as less exposed to legal friction than heavy industry can no longer assume they sit outside the danger zone.

For agricultural and seafood exporters, trade defense readiness is not just a legal department issue. It starts with the raw-material base, production logs, origin records, traceability systems and the ability to pull data from farmers and packaging partners quickly. If sourcing runs through too many middle layers and documentation only gets assembled after questions arrive, the cost of handling an investigation rises sharply.

VOV's reporting from Can Tho offers a useful real-world example. The city has issued 657 planting-area codes covering more than 11,000 hectares, along with 45 packing-facility codes for 17 companies.VOV That is more than an agricultural management detail. For investors, it shows how sustainable exporting is moving away from simply “selling more” and toward proving exactly where a product came from, how it was made and whether the paperwork can stand up to scrutiny.

The transmission mechanism runs straight into margins

One common mistake is to wait for revenue weakness before reassessing the stock. In reality, the first hit often shows up in cost structure and cash conversion. A company can still report healthy top-line growth while legal fees, documentation work, audit requirements and longer customer negotiations start to build beneath the surface.

If an investigation ends badly, exporters usually face three unattractive choices. They can cut prices to keep customers. They can pass part of the cost on and risk losing volume. Or they can scale back in that market to defend profitability. Different paths, same destination: earnings expectations come down, and the valuation multiple investors are willing to pay usually compresses with them.

This is especially sensitive for companies with thin gross margins. When there is little room to absorb extra duties, legal expenses or traceability costs, even a modest deterioration can force a repricing of the growth story. Two companies can both post strong export growth, yet carry very different risk quality if one has cleaner data and a thicker margin cushion while the other depends on short-term pricing.

What to watch beyond export revenue

The first signal is market concentration. If a large share of sales depends on one importing country that is stepping up investigations, revenue growth needs to be read alongside concentration risk. A company with more diversified export markets may grow less dramatically, but it is often better positioned to absorb a legal shock in one jurisdiction.

The second signal is gross margin. The thinner the margin, the less room the company has to carry extra duties, consulting bills or origin-compliance costs. In steel, Investify's internal data shows HRC at USD 1,195.10 per ton on June 26, up about 35.0% from USD 885 per ton on the same date a year earlier. When input prices move that sharply, questions around pricing, subsidies and injury to domestic producers in the importing market tend to become more sensitive.

The third signal is the combination of receivables, inventory and operating cash flow. Revenue is what gets booked; cash collection tells you whether customers remain confident enough to keep the relationship moving. If sales rise while receivables swell, inventory turns slow and operating cash flow weakens, that is usually the moment to dig deeper instead of celebrating growth at face value.

The fourth signal is disclosure quality. Companies that speak loudly about export expansion but say little about traceability systems, sourcing transparency, legal risk or early-warning capability deserve more caution. By contrast, a slower-growing exporter that is clear about customers, inputs and contingency planning may justify a lower risk discount.

A more useful framework for reading export stocks

For newer investors, the lesson is not to avoid the export sector altogether. Exports remain a major growth engine for many Vietnamese businesses, and there is no evidence that every company will face the same outcome. But the new warning does require a different reading frame. The question is no longer only whether orders are growing. It is whether the company can preserve the quality of that growth when scrutiny intensifies.

A practical framework is to separate exporters into two broad groups. The first group grows revenue quickly but relies heavily on a small set of markets, operates with thin margins, has weaker traceability and tends to discuss risk in generic language. The second group may look less flashy on sales growth, but it has more diversified end markets, cleaner raw-material systems, stronger data infrastructure and better margin resilience. In the current environment, that second group is more likely to earn a sturdier valuation.

The core thesis is straightforward: for export stocks, revenue growth is necessary but no longer sufficient. The more important valuation layer now sits in trade defense readiness, margin durability and the quality of data a company can produce when challenged. The indicators worth tracking over the next few quarters are export-market concentration, receivable trends, risk disclosure quality and real investment in traceability. If those variables do not improve, revenue growth on its own will become a much weaker argument for the stock.