SASCO has just put three market-moving signals on the table at once: first-half 2026 revenue is estimated at more than VND 1,500 billion, pretax profit at more than VND 400 billion, and the company is preparing to move SAS from UPCoM to HOSE.Fili A new investor could easily flatten that into one neat story about passenger traffic recovering. That would miss the real point. The market is not only watching how many travelers pass through the airport. It is watching whether SASCO can hold on to the most profitable parts of the non-aviation value chain.

That distinction matters because profit is growing faster than revenue in a business many people still treat as a pure traffic proxy. Once that happens, the right question is no longer whether more passengers are flying. The better question is what services the company is selling, which travelers it is monetizing best, and how much profit it keeps from each revenue line.

The numbers already say this is more than a traffic story

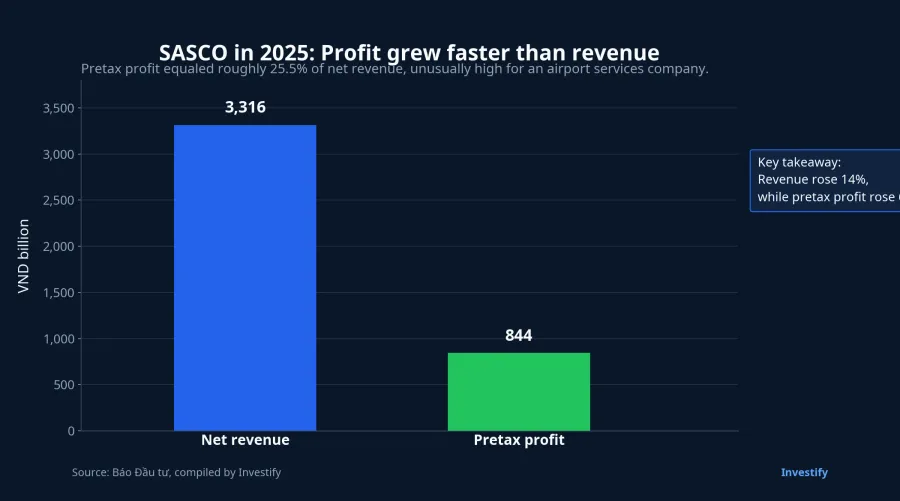

In 2025, SASCO posted total revenue of VND 3,535 billion, net operating revenue of VND 3,316 billion and pretax profit of VND 844 billion. Pretax profit rose 67%, far faster than the 15% increase in total revenue.Báo Đầu tư That gap alone tells investors something important: revenue growth and profit growth are not interchangeable. When profit outruns revenue by that margin, the company is usually either leaning harder into higher-margin segments or running the cost base better, often both.

That pattern did not disappear in the opening quarter of 2026. Dân trí reported that SASCO generated VND 779 billion in net revenue and VND 155 billion in net profit, while passenger traffic through Tan Son Nhat rose by about 9%.Dân trí A 9% traffic increase is solid, but it is not explosive. The fact that profit still held up well suggests SAS should not be read as a simple mechanical bet on airport volumes.

That is especially true in airport services, where mix matters almost as much as footfall. An international traveler, a premium passenger, and a shopper willing to spend in duty free are not economically equivalent to a domestic traveler who simply passes through the terminal. The same traffic rebound can produce very different profit outcomes depending on which services a company controls and how much pricing power it has inside the airport ecosystem.

Earnings quality matters more than a strong headline

The interesting part of SASCO's story is that the profit base does not look like a one-off seasonal spike. According to Báo Đầu tư, the company expanded its presence at Tan Son Nhat's T3 terminal, opened the Lotus lounge early in the rollout phase and kept building a more integrated non-aviation services ecosystem.Báo Đầu tư For investors, this matters because durable earnings usually come from strong commercial positioning and high-margin services, not just from riding a favorable industry cycle.

Still, not every dong of profit carries the same quality. On first mention, CEO and Board Member Nguyễn Văn Hùng Cường of Công ty Cổ phần Dịch vụ Hàng không Sân bay Tân Sơn Nhất (SASCO, SAS) said the 2026 plan was built conservatively. He also said that if investors strip out the roughly VND 40 billion provision write-back tied to the wage fund in the previous year, core profit would still be up by about 3% this year. Part of the positive first-half result also came from dividends paid earlier by affiliated companies.Fili

That distinction is valuable, especially for less experienced investors. A strong reported quarter does not automatically mean every component of profit is equally repeatable. Profit generated by lounges, airport retail and duty free is the kind the market can value over a longer horizon. Profit boosted by affiliate dividends, write-backs or timing effects is supportive, but it should not be mistaken for the core engine.

Put differently, the market pays up for repeatable earnings. Investors who fail to separate operating strength from accounting support risk misreading both the health of the business and the durability of the stock narrative.

The HOSE move is about standards, not just liquidity

On first mention, Chairman Johnathan Hạnh Nguyễn of Công ty Cổ phần Dịch vụ Hàng không Sân bay Tân Sơn Nhất (SASCO, SAS) said major shareholders had agreed to pursue a transfer of SAS to HOSE in order to improve governance standards, transparency and trading liquidity.Fili If investors only hear the word liquidity, the move can sound technical. In reality, a board change like this matters only if it forces the company to live under a higher baseline of disclosure, market scrutiny and governance expectations.

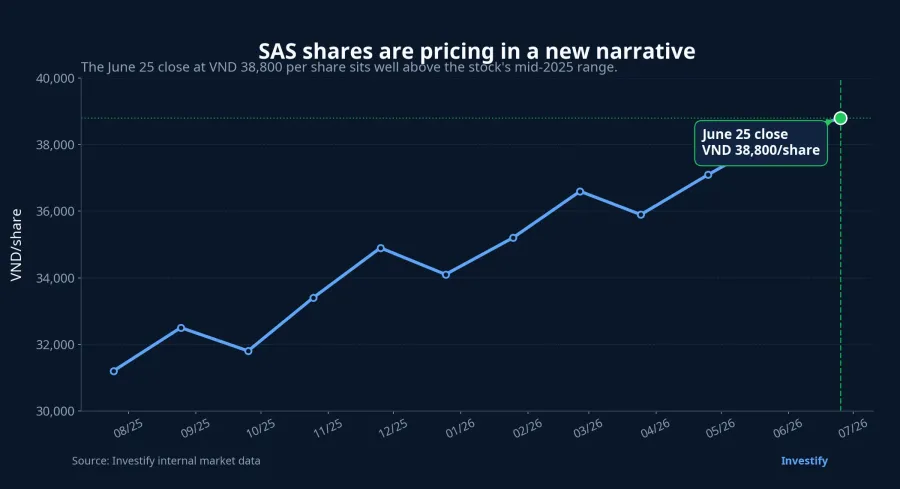

According to Investify's internal market data, SAS closed on June 25 at VND 38,800 per share, up 2.65% from the previous session, on matched volume of 39,100 shares and an implied market capitalization of about VND 5,200 billion. A company generating hundreds of billions of dong in profit but trading with a thin free float is often difficult for both institutions and retail investors to engage with meaningfully. If a move to HOSE comes with better visibility and, eventually, better float, the market's valuation framework for SASCO could shift.

There is also a broader regulatory backdrop. VnEconomy reported that Circular 139/2025/TT-BTC requires HOSE to complete the transfer of listed shares from HNX by December 31, 2026.VnEconomy SASCO is currently on UPCoM, not HNX, so investors should not overstate the direct effect of that policy on this stock. But the larger message is still useful: the market structure is moving toward clearer specialization and higher listing discipline. A company that wants to be treated as a higher-quality public-market story will eventually have to fit that direction.

This is also where investors need to avoid an easy causal leap. A move to HOSE does not automatically send the share price higher. The real effect depends on what happens after the move: better disclosure, broader investor attention, and whether liquidity actually improves in substance rather than in narrative. HOSE is a gateway to a different valuation conversation, not a guaranteed reward.

Long Thanh is an option on future growth, not booked profit

The third layer of the story is Long Thanh. Fili and Dân trí both reported that SASCO is preparing operating models, staffing, physical space and financial resources so it can join tenders when opportunities open up at Long Thanh International Airport.FiliDân trí That is worth watching because it fits the company's capabilities and could open a new non-aviation profit pool.

But it needs to be framed honestly. Long Thanh is still an option on future growth, not a profit stream investors can already count on. The outcome depends on project timing, tender terms, location allocation, duty-free partners and, ultimately, real passenger throughput once the airport is operating. If the market starts pricing Long Thanh as though the earnings are already secured, investors will be front-loading hope into valuation.

The cleaner way to read SASCO is to separate it into three layers. The first is the current core business: lounges, airport retail, service operations and the ability to protect margins. The second is the capital-markets layer: a potential transfer to HOSE and a higher listing standard. The third is Long Thanh, where the company has a credible right to compete, but not a guaranteed stream of cash flow.

The core thesis is straightforward. SASCO is being re-rated primarily because of earnings quality and the prospect of moving into a stricter listing framework, not simply because more passengers are flying again. Long Thanh can extend the story later, but the evidence is not strong enough yet to treat it as a live earnings driver. Over the next few quarters, the key signals to watch are whether core margins hold, whether the HOSE plan advances, and whether SASCO secures any concrete commercial position at Long Thanh.