Vietnam has just widened its fiscal room, but that alone does not turn every infrastructure-linked stock into the same opportunity. What matters next is not the headline about a looser budget stance. What matters is how quickly public money moves from planning documents to construction sites, and from construction sites to revenue, margin, and cash flow.

The new framework matters because it signals a stronger policy commitment to growth through capital spending in 2026-2030. That is meaningful for listed companies tied to highways, materials, logistics, and industrial infrastructure. But in the stock market, policy is only the opening move. Investors still need proof that money is actually flowing through the system.Bao Chinh Phu

What the new fiscal framework really changes

Decision 1119/QD-TTg, issued on June 23, 2026, revises parts of Decision 368/QD-TTg. Under the updated framework, state budget mobilization for 2026-2030 rises to 18% of GDP, the domestic revenue share moves to 87-88%, and development investment spending is targeted at roughly 40% of total state budget expenditure.Van ban CP In practical terms, that creates more room for public investment to play a larger role in the growth mix.

The headline figure is the budget deficit target, which has been lifted from around 3% of GDP to around 5% of GDP by 2030. The national ceiling for external debt also moves up from 45% to 50% of GDP, expanding the fiscal buffer relative to the previous framework.Bao Chinh Phu For investors, the message is not that every public-investment theme becomes bullish overnight. The message is that the state now has more room to sustain capital spending over a multi-year horizon.

That is still only the policy layer. Between a fiscal target and a company's earnings report sit several filters: budget allocation, capital assignment, actual disbursement, project execution, accepted work volume, and working-capital pressure. New investors often skip these middle layers and buy the big story too early. That is usually where disappointment starts.

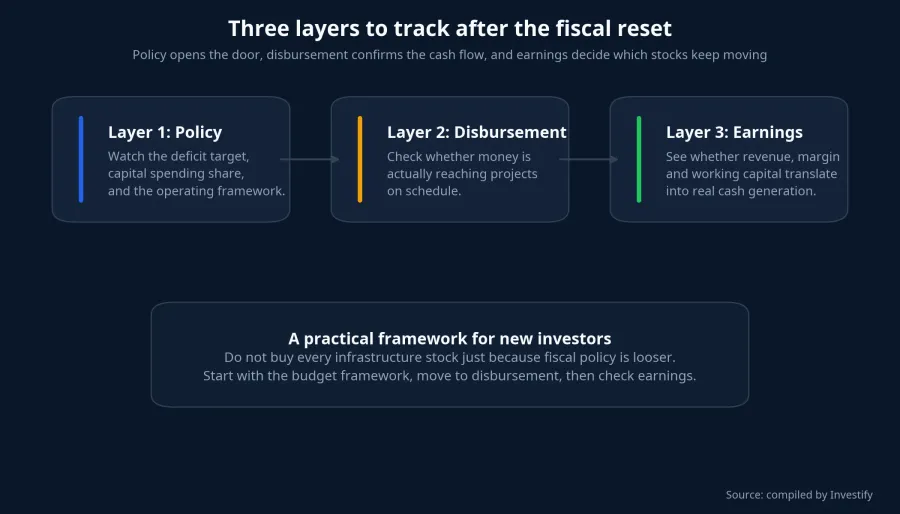

A three-layer framework for reading the story

The cleaner way to read this theme is to split it into three layers: policy, disbursement, and corporate earnings. Each layer tells a different part of the story, and each one arrives on a different timeline.

The first layer is policy. This is where the market reacts to the state's willingness to dedicate a larger share of the budget to development spending. It is the earliest source of optimism, and it is why construction contractors, quarry operators, cement names, steel suppliers, logistics players, and industrial park developers quickly enter investor conversations. But policy is also the layer most vulnerable to over-excitement, because prices can move well before cash does.

The second layer is disbursement. This is where the story begins to earn credibility. Once funds leave the planning stage and hit actual projects, the market can start judging whether the headline has operational substance. Until then, the theme remains more narrative than evidence.

The third layer is earnings. A company can win more contracts and still fail to create shareholder value if input costs rise, working-capital needs stretch, or margins stay thin. In the end, the market rewards businesses that can turn execution speed into real profit, not just bigger top-line numbers.

The trading screen is already telling a selective story

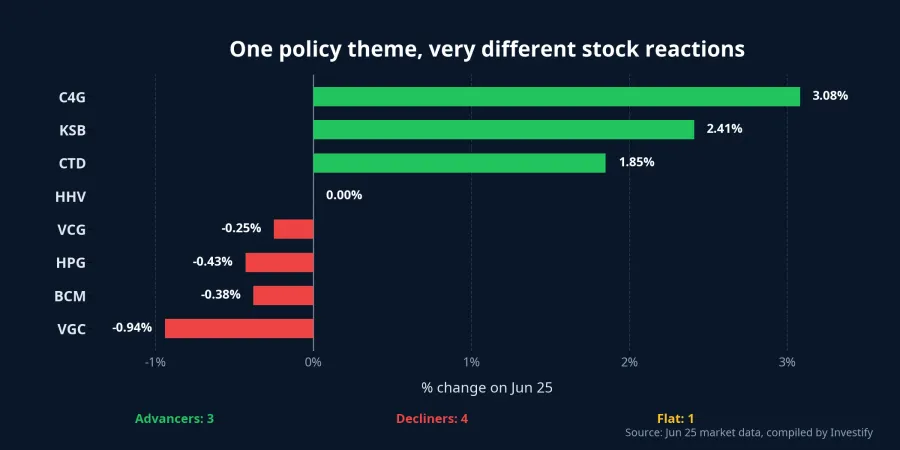

If the new fiscal framework were enough to lift the entire public-investment complex at once, the market would already be showing it. Instead, the June 25 session pointed in the opposite direction. The VN-Index closed at 1,863.07, down 14.95 points, or 0.80%, while stocks associated with public investment moved in sharply different directions.

C4G rose 3.08%, KSB gained 2.41%, and CTD added 1.85%. On the other side, VCG slipped 0.25%, HPG fell 0.43%, BCM lost 0.38%, VGC dropped 0.94%, and HHV was flat. The same macro narrative produced very different stock outcomes. For new investors, that is the key lesson: the market is selecting specific links in the chain, not buying the entire "public investment" label.

That selectivity is rational. A contractor may benefit early if its backlog is large and revenue recognition lines up with project progress. A materials company can look better if its quarry sits close to the project, keeping transport costs low. By contrast, steel names, port operators, or industrial park developers may need more evidence before the market treats the story as an earnings upgrade.Bao Chinh Phu

Disbursement is improving, but it is not the final confirmation yet

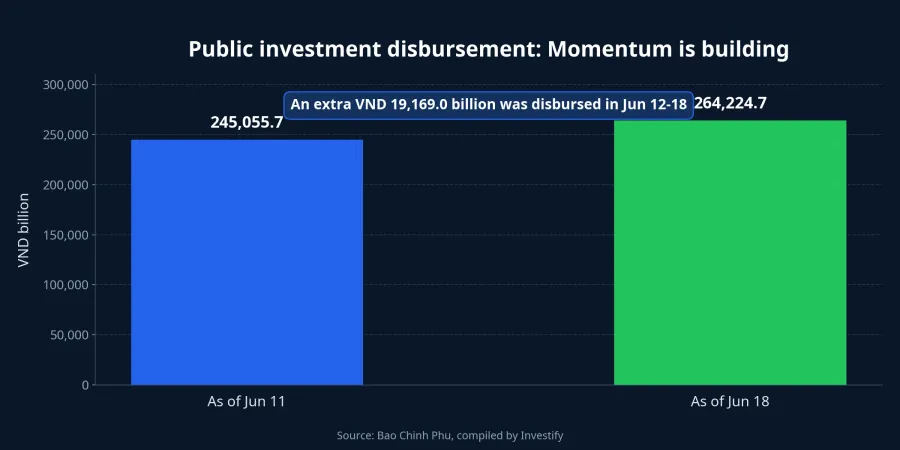

The latest government data show that as of June 18, 2026, public investment disbursement had reached VND 264,224.7 billion, equal to 25.7% of the plan assigned by the Prime Minister. The 2026 public investment plan funded by the state budget totals VND 1,026,662.1 billion, while the cumulative assigned plan at the reporting date, including additions from local governments, stands at VND 1,040,261.7 billion.Bao Chinh Phu

During June 12-18 alone, newly disbursed capital reached VND 19,169.1 billion, 1.1 times the previous week.Bao Chinh Phu That is a constructive sign because it shows momentum. It is still not enough, however, to conclude that every linked company has entered a fresh earnings cycle.

The reason is straightforward: faster disbursement does not flow evenly into every listed name. One project may move quickly, but the company involved could be a subcontractor with thin margins. Another company may win larger work volume, yet need to commit more working capital before seeing the benefit in cash flow. That is the difference between having a story and having results.

Who gets watched first, and who still needs proof

Historically, the first names to be re-rated are usually infrastructure contractors and materials businesses located close to active projects. Those are the areas where disbursed capital is most likely to convert quickly into measurable work volume. If project execution stays on track, backlog and revenue recognition in these groups become the market's first verification points.

Steel, asphalt, logistics, and infrastructure operators can benefit as well, but their timing is often less direct. The same public-investment theme does not reach every industry at the same speed. Industrial parks, for example, may gain later because the effect still depends on transport connectivity, land legality, rental pricing, and handover progress.

What policy alone cannot answer is which companies can defend their margin. That is the real long-term question. A public-investment cycle only creates durable stock winners when companies avoid margin erosion from input costs, wage pressure, and capital intensity. The framework creates opportunity for many businesses, but it does not promise the same return profile for all of them.

What investors should monitor next

One detail deserves more attention than it has received so far. Decision 1129/QD-TTg, issued on June 24, 2026, approves a scoring framework for ministries, central agencies, and local governments based on how they execute public investment disbursement plans. Monthly and quarterly scoring will be used to commend, push, remind, or warn units depending on execution quality.Bao Chinh Phu

That matters because the government is moving from messaging to measurement. Once disbursement progress is tracked regularly, investors gain a cleaner way to separate stories backed by real money from stories backed only by expectation. For new investors, that is a much safer framework than buying an entire sector basket on a single policy headline.

The thesis, then, is fairly direct: Decision 1119 expands Vietnam's fiscal room for 2026-2030, but the real stock winners will only emerge if disbursement keeps accelerating and corporate earnings confirm the flow-through. The main signals to watch over the next two weeks are updated disbursement data, liquidity accompanying price action in construction and materials stocks, and second-quarter earnings reports. If those three indicators improve together, the public-investment story becomes more durable. If disbursement slows or profit fails to track revenue, the market is likely to reprice expectations quickly.