Decree 200 does not make every private placement safer overnight. What it actually does is tighten issuance discipline, force issuers to be more explicit about why they are borrowing, how proceeds will be used, and what happens if they want to amend bond terms later. For first-time investors, that is real progress. But it mainly fixes the rulebook, not the market's ability to price risk.

That distinction matters because Vietnam's bond market has already taught investors a painful lesson. In the earlier phase, many buyers relied on a short checklist: the coupon was higher than a bank deposit, the bond had collateral, and the product was marketed as something meant for professional investors. After the trust shock of 2022-2023, the right question changed. The issue is no longer just how high the coupon is. The issue is where repayment cash will come from when the bond matures, and whether the investor can tell a strong issuer from a weak one.ĐTCK

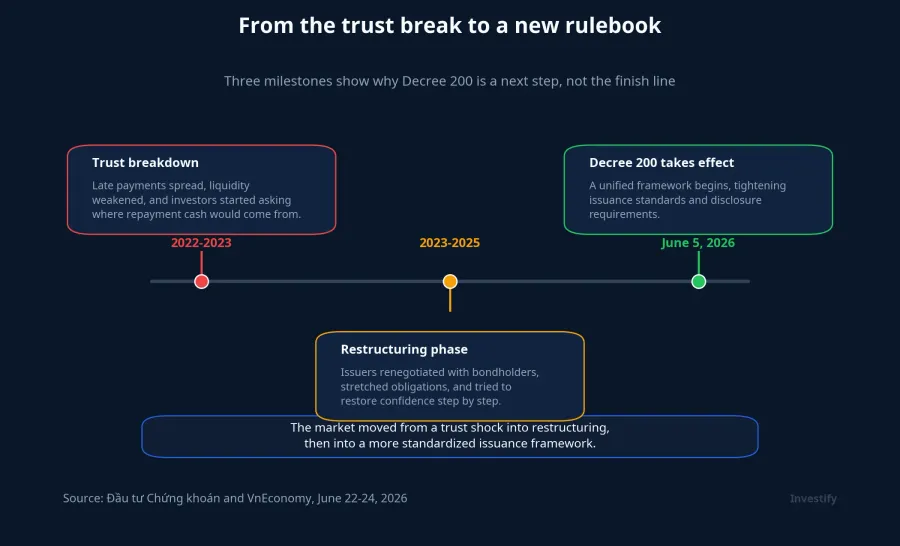

From a trust shock to a new rulebook

Decree 200/2026/NĐ-CP took effect on June 5, 2026 and replaced three earlier frameworks at once: Decree 153/2020, Decree 65/2022, and Decree 08/2023.VnEconomy That matters because the market is no longer moving through a series of temporary patches. It is shifting toward a more unified operating framework. After the dislocation of 2022-2023, investors needed more than another incremental rule. They needed a clearer map of where rights and obligations sit.

Viewed as a timeline, Decree 200 looks like the next step in a rebuilding process rather than the finish line. The first phase was crisis management, when delayed payments and collapsing liquidity changed how investors thought about bonds. The second phase was restructuring, with issuers negotiating with bondholders. Decree 200 sits in a third phase: standardizing the market for what comes next.ĐTCK

The point is not that regulators are trying to shut the market down. The point is that they are trying to keep private placements alive inside a narrower and more disciplined framework. For new investors, that means a high coupon can no longer stand on its own as the main selling point.

What has been repaired is issuance discipline

The clearest change in Decree 200 is the tightening of issuance discipline and proceeds management. Funds raised from bonds must be tracked separately and used for the purpose disclosed to investors. If the proceeds are not yet disbursed, the money can sit in bank deposits or certificates of deposit, but it still has to remain ring-fenced within the logic of the original issuance plan.VnEconomy In practical terms, bond proceeds are less likely to disappear into a company's general cash pool.

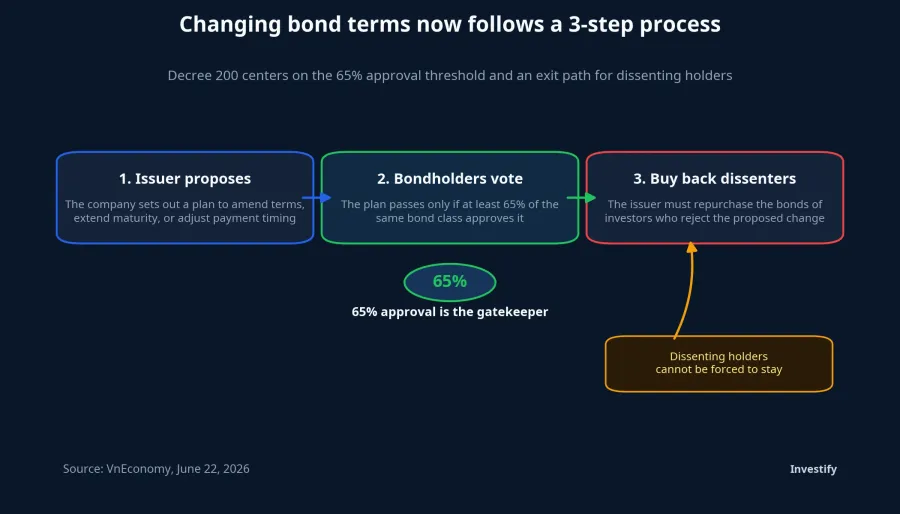

The second layer of discipline sits in how bond terms can be changed. According to VnEconomy, if an issuer wants to amend bond conditions or change the issuance purpose, it must obtain approval from holders representing at least 65% of the same bond class outstanding. Just as importantly, investors who disagree cannot simply be dragged along: the issuer must repurchase their bonds early.VnEconomy

For first-time investors, this may be the most practical protection in the decree. The 65% threshold does not eliminate conflict, but it makes amendments less arbitrary and gives dissenting holders a cleaner exit path.

There is also a tighter gate for issuers. Under the new rules, total liabilities, including the value of the planned bond issuance, cannot exceed 5 times equity, except for several special groups such as credit institutions, insurers, state-owned enterprises, and issuers raising funds for real-estate projects.VnEconomy In practice, that means the bond window has narrowed for many highly leveraged companies.

What remains unrepaired is risk pricing

If you only look at the legal side, it is easy to conclude that private placements are now much safer. But the more important question is whether the market has become better at reading risk. For now, the answer is not enough.

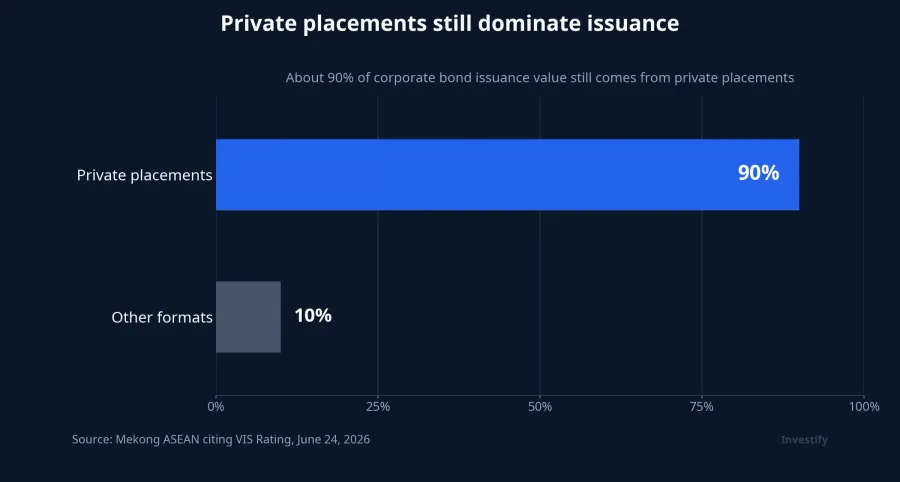

Mekong ASEAN, citing VIS Rating, reported that private placements still account for about 90% of total corporate bond issuance value.Mekong ASEAN That means any change to the private-placement framework reaches the bulk of the market. At the same time, VIS Rating also argued that the biggest structural weakness remains risk-based pricing, because credit-rating coverage is still thin and Vietnam still lacks a reliable corporate bond yield curve segmented by credit quality and tenor.Mekong ASEAN

That is where many new investors get tripped up. Better disclosure does not automatically mean better pricing. A bond can come with more detail on use of proceeds, collateral, and debt obligations, yet the offered yield may still fail to capture the true credit risk if the market does not have a solid benchmark for what that risk should cost. Đầu tư Chứng khoán, citing VIS Rating, said bonds that have actually been credit-rated account for only about 1% of total corporate bonds outstanding, while more than half of private placements in recent years were sold to institutional investors and were not required to carry a credit rating.ĐTCK

In practical terms, the room is better lit than before, but the ruler is still weak. Investors can see more data, yet they still may not know what level of danger that data is signaling.

How a new investor should read a bond

If the process has to be reduced to a simple order, start with repayment capacity and only then move to the coupon. A bond is debt. It is only as sound as the issuer's ability to generate steady cash flow or convert real assets into cash when needed.

The second layer is the issuance purpose. Funding for a project with a clear legal status, visible progress, and a plausible future revenue stream is very different from borrowing that mainly refinances old debt under vague language. Decree 200 makes that disclosure clearer, but investors still need to ask whether the new money creates new cash flow or merely pushes an old liability further into the future.VnEconomy

The third layer is collateral. Collateral has never meant automatic recovery. Investors need to know whether the asset is legally clean, whether it has already been pledged elsewhere, and whether today's valuation would still hold in a weaker market. Only after that should investors look at credit ratings and yield. A rating is not an ironclad guarantee, but it is still a better reference point than a sales pitch.

Conclusion: trust returns only when pricing improves

The core thesis is straightforward. Decree 200 has repaired the issuance-discipline side of the market: proceeds are tracked more clearly, term changes are harder to push through, highly leveraged issuers face a narrower funding window, and bondholders are less exposed to unilateral changes.

But trust in Vietnam's corporate bond market will only return in a durable way when the missing pieces are built out as well: wider credit-rating coverage, better secondary-market data, and a yield curve strong enough to tell investors whether a quoted return is truly compensating for risk. Until that happens, the right response is to read each bond as a separate debt instrument, with its own cash-flow profile, collateral quality, and risk structure.