MWG plans to issue 7.34 million shares to 66 employees at VND 10,000 per share.CafeF That price sits far below MWG's VND 76,000 closing price on June 23, so it is easy for new investors to react with the same thought: this looks abnormally cheap. The problem is that an employee stock plan is not supposed to function as a price tag for the whole market.

The cleaner way to read this deal is as a long-term compensation package. MWG is using low-priced shares to retain the managers it believes are most important to the business. For outside shareholders, the useful questions are different: who is the company trying to keep, how long are those incentives locked up, and does the dilution buy enough future performance to be worth it?

Why the VND 10,000 price can mislead investors

The gap between the issue price and the stock's market price is the part that draws the most attention. Set against the June 23 close of VND 76,000, the ESOP price is only about 13.2% of the market value. That is a wide enough gap to make retail investors think insiders are getting access to something unusually cheap.

But that is not what the ESOP is designed to say. It does not say MWG stock is cheap for everyone else in the market. It says the company is willing to transfer some future value to employees in exchange for loyalty, execution, and continuity. In other words, VND 10,000 is better read as an internal incentive price than as a fair market valuation.

That distinction matters even more for a retailer like MWG. The company's value does not sit only in the brand or store count. It also sits in running thousands of sales points, managing inventory turns, negotiating with suppliers, keeping working capital moving, and maintaining service quality across chains. In a tougher competitive phase, losing key operators can cost more than a small amount of paper dilution.

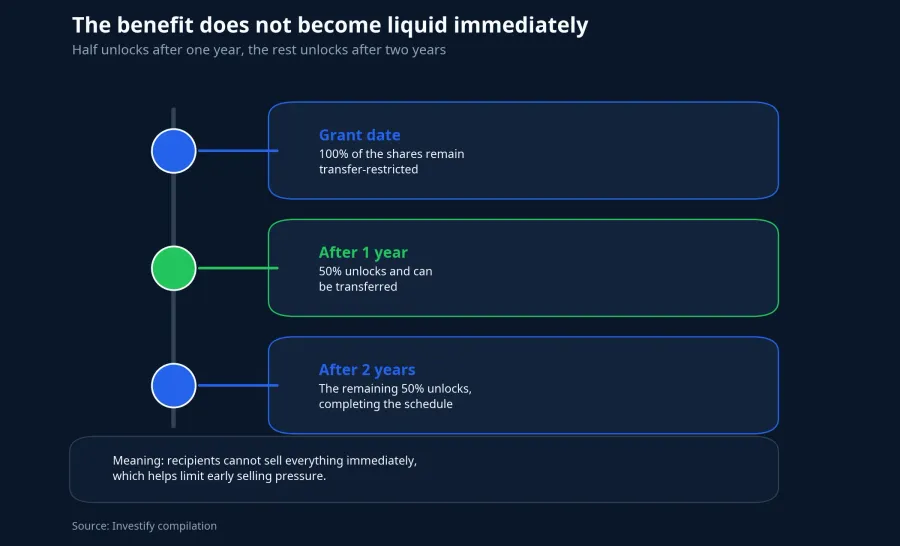

This is a retention package, not an instantly liquid benefit

The allocation list is concentrated in MWG's core management ranks rather than spread broadly across employees. Đoàn Văn Hiểu Em, CEO of Công ty CP Đầu tư Điện Máy Xanh (DMX), received the largest allocation at nearly 722,000 shares. Vũ Đăng Linh, CEO of Công ty CP Đầu tư Thế Giới Di Động (MWG), is set to buy 275,409 shares, while Nguyễn Đức Tài, Chairman of Công ty CP Đầu tư Thế Giới Di Động (MWG), is not included in the list.CafeF

That tells shareholders which parts of the organization MWG is trying hardest to keep. For newer investors, this says more than the VND 10,000 headline ever could. If the company is directing shares toward the people who run store operations, product categories, and execution on the ground, then the message is that operating capability is the asset management wants to protect most.

The benefit also does not unlock right away. Under the announced plan, 50% of the shares can be transferred after one year, while the remaining 50% unlock after two years. The issuance is expected in the second or third quarter of 2026, subject to approval from the State Securities Commission of Vietnam.CafeF

That structure matters in two ways. Yes, recipients are clearly receiving a major advantage relative to outside shareholders. But no, they cannot simply take the shares and sell everything immediately. The actual contract MWG is offering is a cheap entry price today in exchange for staying and delivering over the next one to two years.

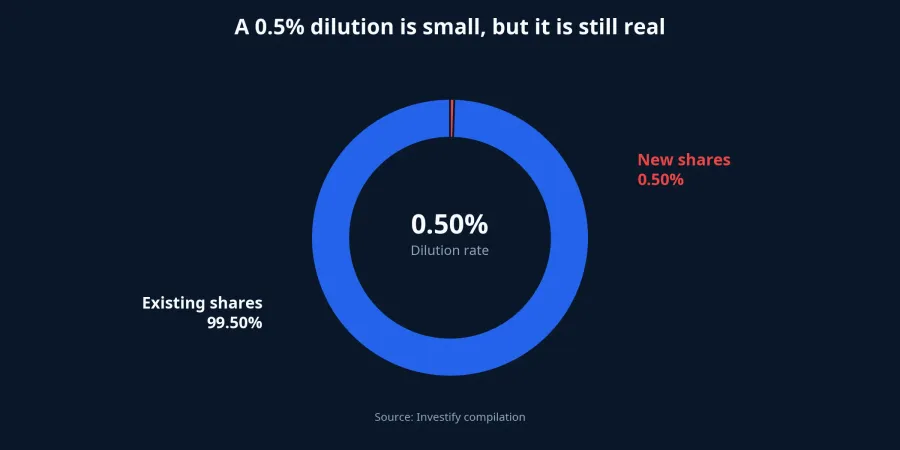

A small dilution is still a real one

MWG currently has more than 1.468 billion shares outstanding. If it issues another 7.34 million shares, the post-issuance total would rise to roughly 1.476 billion shares, implying dilution of about 0.5%.Thời báo Tài chính Việt Nam For a small outside shareholder, that is not a large mechanical hit.

If everything else stayed unchanged, earnings per share would face only a roughly similar reduction. So it would be overstated to call this heavy dilution. Still, calling it irrelevant would also be too casual, because even a 0.5% issuance means existing shareholders are giving up a slice of value in exchange for retaining staff.

That is why the issue is not the percentage by itself, but the quality of the trade-off. If the ESOP recipients help sustain growth, improve margins, and strengthen execution, shareholders can treat the dilution as an investment in organizational capability. If earnings fail to improve while ESOP grants keep showing up year after year, the cumulative effect becomes a different story.

What outside shareholders should track next

This is where the harder part begins. An ESOP is only defensible if it is matched by business results strong enough to offset the value transferred to insiders. "Talented managers got a cheap price" is not a reason for outside shareholders to celebrate. The reason only appears if profitability, chain performance, and growth quality improve afterward.

MWG has set a 2026 plan of VND 185,000 billion in net revenue and VND 9,200 billion in consolidated net profit, up 18% and 30% from the previous year, respectively. In the first five months of 2026, net revenue reached VND 79,159 billion, up 29% year on year and equal to 43% of the full-year target.CafeF That is the real scorecard for judging whether this employee share issuance makes sense.

It is also worth keeping some analytical discipline here. MWG trading at VND 75,300 in the morning session on June 24 is not enough evidence to say the market rejected the ESOP plan, just as a short-term bounce would not prove investors endorsed it. One trading session can still reflect broader retail-sector sentiment, index moves, and short-term positioning, so the evidence is too thin to assign a single cause.

For new investors, a steadier approach is to watch three indicators after the headline fades. First, does profit stay on track with management's 2026 target. Second, do core chains such as Điện Máy Xanh and Bách Hóa Xanh continue to improve their operating performance. Third, does MWG keep ESOP issuance disciplined and small, or does it let equity compensation become a repeated transfer of value that grows too frequent.

The core conclusion is straightforward: VND 10,000 is not a bargain invitation for the market to buy MWG shares. It is the price of a stock-based retention contract. For outside shareholders today, this ESOP looks like a long-term personnel cost accompanied by small dilution. That thesis holds only if the next few quarters show that the concession actually buys better execution, rather than simply moving more value from shareholders to insiders.