A bank bond paying as much as 9% a year can easily look like nothing more than a high-yield savings product. It carries a bank's name, pays income on a schedule and is marketed with one familiar headline number: annual return. For first-time investors, though, the critical distinction sits beneath the headline rate. Deposits and bank bonds do not come with the same layer of capital protection.Dân trí

That is the core thesis here. The extra yield on a bank bond is not a free upgrade over a term deposit. It is compensation for taking clearer credit risk, weaker liquidity and a different legal claim on the bank. Once retail investors frame the product that way, the word "bank" becomes less comforting and the actual contract starts to matter more.

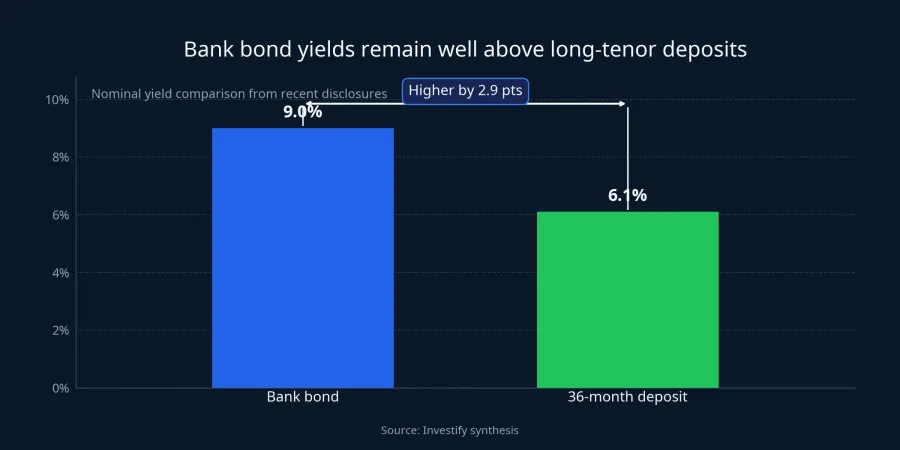

How wide is the yield gap right now

According to a June 22 report by Dân trí, several banks are issuing bonds with coupons ranging from 7.9% to 9.0% a year. VietABank had a VND 100 billion issue at 9.0%, MB completed 10 tranches totaling nearly VND 6 trillion at 8.3% to 8.4%, and VPBank raised VND 1 trillion at a fixed 8.6% for a 3-year tenor.Dân trí

The same article cited a roughly 6.1% annual rate for a 36-month deposit at the time.Dân trí A spread of about 2.9 percentage points is large enough to make any saver pause. For a novice investor, that is precisely where the framing error starts: the eye locks onto the extra yield before asking what had to be given up to earn it.

In finance, higher yield rarely arrives with identical safety. When an instrument pays almost 3 percentage points more than a long-tenor deposit, that is usually a sign that the buyer is accepting weaker liquidity, a lower place in the repayment queue, more complex contractual terms or a thinner protection layer. The headline rate is not a standalone benefit. It comes attached to a bill.

Why banks are willing to pay more

From the buyer's side, a bank bond can look like a product that simply needs a richer rate to attract money. From the bank's side, the logic is more structural. Dân trí said banks offered more than VND 61 trillion of bonds in the first 5 months of the year, while FiinRatings expects funding demand to stay elevated in the second half because the gap between deposits and credit growth may not close soon and some lenders still need more Tier 2 capital to meet safety ratios.Dân trí

In plain English, retail deposits can come in quickly but also move quickly when rates shift. Bonds help banks lock in funding for longer and under predefined terms. They also reduce the risk of early cash withdrawals in the way term deposits do not. Because bonds solve a different funding problem, banks are willing to pay more for that stability.

That point matters because it keeps investors from drawing the wrong conclusion. A higher coupon does not automatically mean a bank is suddenly unsafe, nor does it mean buyers have found a free-yield loophole. It simply means the bank and the investor are entering into a different capital contract, with a different set of rights and obligations on each side.

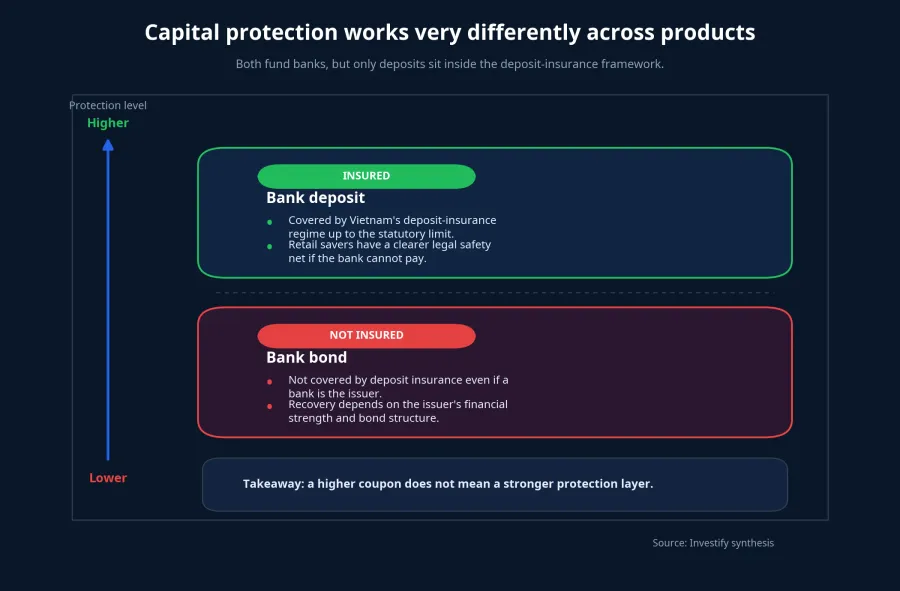

Deposits are insured, bonds are not

The biggest distinction starts with deposit insurance. Vietnam Deposit Insurance says the maximum insured amount for all covered deposits held by one individual at one participating institution is VND 125 million, including principal and interest.DIV That does not make every deposit risk-free, but it does place personal deposits inside a dedicated protection framework.

Bank bonds sit outside that framework. When investors buy a bond, they are lending money to the bank under issuance terms. They are not opening an insured deposit account. So if a bank bond is pitched using the logic of "a bank deposit, but with a better rate," that pitch is already omitting the product's most important feature.

For household money management, this difference is not abstract. If the main objective is to park cash safely, the clarity of the protection layer can matter more than the extra yield itself. A higher coupon only deserves attention once investors fully understand that they are leaving the insured-deposit bucket and moving into a credit instrument instead.

Liquidity and exit routes work differently

A term deposit can usually be broken early, even if the saver then receives a reduced rate under the bank's policy. That gives depositors a relatively clear escape route. Bonds do not work like that.

If the issuance terms include a put or a call structure that effectively creates an exit at a known point, the investor has one more option. If not, liquidity depends on the secondary market, on whether there is a willing buyer and on what price that buyer is prepared to pay. A coupon can look attractive on paper while the real-life ability to get cash out remains much weaker than it is with deposits.

This is where first-time investors most often misread the trade-off. They compare 9.0% with 6.1% and mentally book the difference as a certain annual gain. In practice, if cash is needed early and the bond is hard to sell, the original headline yield can lose much of its value. No investment product should be judged by the quoted rate alone. The exit path matters just as much.

Not every bank bond is meant for every retail buyer

Distribution rules matter too. In BIDV's public bond offering, the minimum subscription size was 100 bonds, equivalent to VND 10 million at par value.Báo Pháp luật That is a more accessible structure for individuals, at least in terms of entry.

Private placements are a different story. VnEconomy reported that Decree 200/2026/NĐ-CP classifies investors by bond type and tightens access conditions for some private bond cases.VnEconomy LuatVietnam said the professional-investor test in the relevant case includes a listed or registered securities portfolio of at least VND 2 billion, measured on average over at least 180 days.LuatVietnam

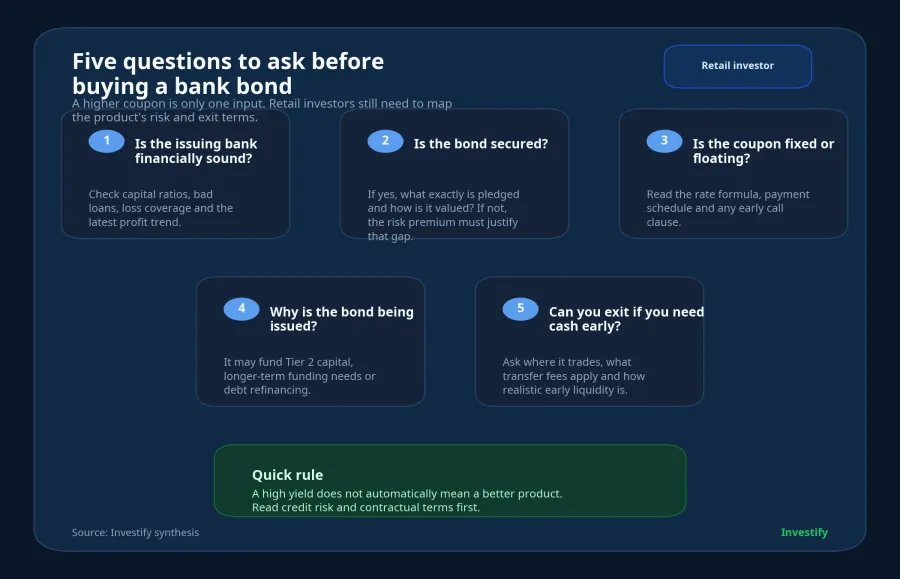

The key takeaway is that "bank bond" is not one generic label with one uniform purchase path. Some issues are public. Some are private. Some are designed to support Tier 2 capital. Others are meant to extend medium- and long-term funding. Without reading the issuance structure carefully, a retail investor can easily assume a bond is a mass-market product when it was actually built for a very different buyer profile.

The terms matter more than the headline rate

BIDV has approved a private issuance plan totaling VND 41 trillion, including VND 21 trillion with maturities longer than 5 years and VND 20 trillion with tenors from 2 to 5 years.Báo Pháp luật The same report said those tranches are subordinated debt, non-convertible, without warrants and unsecured.Báo Pháp luật

For new investors, terms such as "subordinated" or "unsecured" are easy to skim past because they sound technical. In reality, those are exactly the words that define where the investor stands inside the product's risk structure. Two bonds issued by the same bank can offer very different real protections and recovery prospects even if both are marketed with an annual percentage coupon.

That is why the first question should not be, "Which bank is paying the highest rate?" A better checklist is: Is the issue public or private? Is it covered by deposit insurance? Is there collateral? Is there an early redemption clause? If cash is needed, where does this paper actually trade? Until those questions are answered, a 9.0% coupon is just an attention-grabbing number, not a decision-ready fact.

Conclusion: the extra yield pays for a different contract

On the surface, both deposits and bank bonds are ways of placing money with a bank in exchange for income. Under the hood, they belong to different risk buckets, offer different withdrawal rights and sit inside very different legal frameworks. The most coherent conclusion, then, is not that bank bonds are categorically better than deposits or vice versa. It is that each product serves a different cash-management need.

For investors who want a place to park money, value flexibility and prefer a clearer protection layer, deposits remain the more suitable tool. For investors who understand they are buying a debt instrument, can lock up capital for longer and are disciplined enough to read issuance terms closely, the extra yield on bank bonds may be worth considering. The signals worth tracking next are not just where rates move, but how banks continue to structure new issuance terms and how regulation keeps separating retail investors across bond products.