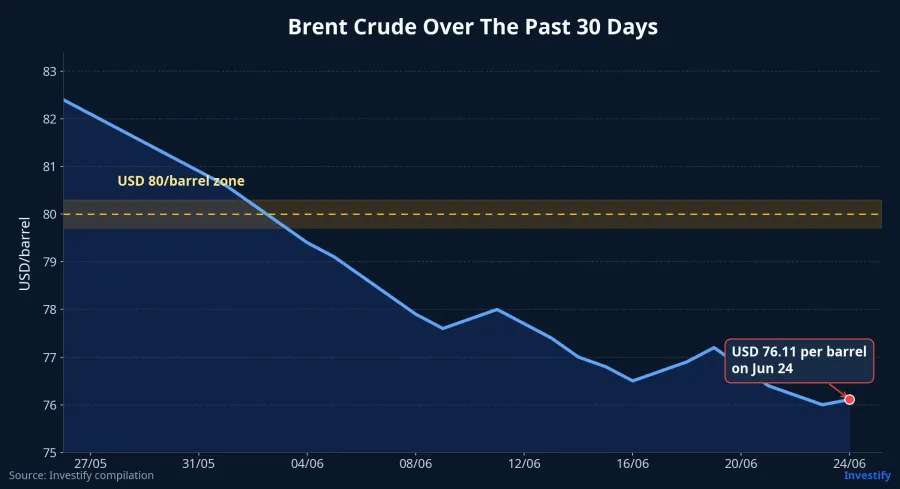

Some market sessions force new investors to drop the habit of treating an entire sector as one trade. June 24 was one of those sessions. The VN-Index still closed at 1,878.02 points, up from the prior session, while Brent crude slipped to USD 76.11 per barrel, well below the USD 80.59 level seen on June 19. If you looked only at oil, you might have expected a broad sell-off across Vietnam's oil and gas names. The tape said otherwise.

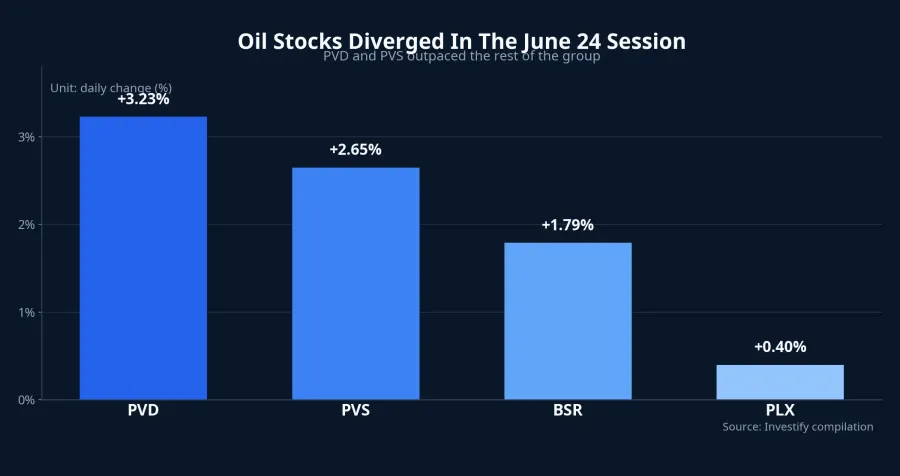

PVD rose 3.23% to VND 31,950 per share, PVS gained 2.65% to VND 38,800, BSR added 1.79% to VND 25,550, and PLX edged up just 0.40% to VND 37,850 in the same June 24 session. One input, four very different reactions. For first-time investors, that matters more than the headline number of USD 76 per barrel, because it shows that oil is only the starting signal. The outcome depends on where each company actually makes money inside the value chain.

What the market is really repricing

The simplest way to think about it is this: when Brent drops back below the USD 80 area, the market is not asking a vague question like "is the oil sector turning bad?" The sharper question is which company depends on new drilling decisions, which one depends on signed backlog, which one depends on refining spreads, and which one is more exposed to regulated retail fuel pricing.

That is why June 24 should not be read as a day when the whole sector either rose or fell together. It looked more like a classification test. Companies whose earnings are tightly linked to future exploration spending will be more sensitive to the risk of Brent staying below USD 80 for too long. Names with existing contracts, project execution, or their own pricing buffers can hold up better in the short run.

Drilling and technical services: The most exposed to the second half

PV Drilling describes itself as a provider of drilling rigs, drilling technical services and well services.PV Drilling In plain English, PVD does not live or die on the oil price of a single morning. It lives on rig dayrates, rig utilization and whether upstream operators still want to commit to new drilling campaigns. When Brent falls quickly over a few sessions, current-quarter earnings do not necessarily change on the spot. But the market immediately starts asking whether lower oil prices might delay future drilling plans if they persist for several weeks or months.

That makes PVD's main risk a forward-looking one, not an instant hit to booked revenue. If rigs remain busy, dayrates stay firm and new contracts keep appearing, the stock can hold up better than newer investors might expect. If Brent stays weak and operators begin to cut capital spending, pressure can move from expectations into valuation very quickly.

PVS looks similar to PVD at first glance, but the business model is not the same. PTSC operates across oil and gas engineering, procurement, fabrication, transportation, installation and offshore project commissioning.PTSC That means PVS is more exposed to project schedules, signed work volume and the pace at which offshore developments keep moving. It still reacts to Brent, but not necessarily in the same way or at the same speed as PVD.

For retail investors, the key takeaway is that drilling and technical services are usually judged by one forward question: how full is the work book for the second half of the year? That is a very different lens from simply glancing at oil and deciding the sector has turned weak. Brent's drop is a warning signal. The real trigger for a deeper repricing is whether work schedules, new contracts and offshore project momentum start to soften as well.

BSR: The real story is not crude oil alone

BSR is where the usual "oil down is bad" reflex becomes even less reliable. BSR sits in refining, so the critical variable is not just whether crude is cheaper or more expensive. Investors need to watch the spread between crude input costs and output product prices, along with inventory revaluation risk.

Put simply, falling crude can be helpful if feedstock gets cheaper while product prices do not fall just as fast. It can also become a headwind if the company is carrying higher-cost inventory or if refined product prices fall faster than raw materials. That is why BSR's 1.79% gain on June 24 does not automatically look contradictory. The market does not seem to be reading lower oil prices as an immediate negative for refiners.

This is where more experienced investors often stay calmer than newer ones. They do not stop at the direction of Brent. They look next at crack spreads, operating rates and the risk of inventory markdowns. If those variables are not deteriorating, BSR can stay steadier than a knee-jerk oil-price reaction would suggest.

PLX: The lag comes from the pricing cycle

Petrolimex says its core businesses include importing and trading petroleum products, refining and related activities.Petrolimex For PLX, the variables worth reading are not daily Brent moves but the domestic pricing cycle, the speed at which lower oil feeds into retail prices, and the distribution margin left behind.

Inside Vietnam, E5 RON 92 stood at VND 20,120 per liter in the June 18 pricing period, down 5.67% from June 11. RON 95-V was VND 21,670 per liter, down 5.62% over the same span. That matters because the path from oil to PLX earnings runs through a regulated pricing schedule and retail margins, not directly from Brent into same-day profit expectations.

That helps explain why PLX rose only 0.40% on June 24. The market is reading PLX through a different earnings mechanism than PVD or PVS. Here, investors should track inventory, the pace of retail price adjustments and whether distribution margins get squeezed harder.

Three signals that are enough for new investors

If I had to reduce the whole sector to a short watchlist, I would keep three signals. First, does Brent stay below the USD 80 per barrel area for long enough? One or two weak sessions do not mean much, but several weeks below that zone would force the market to reassess new drilling demand and upstream capital spending.

Second, watch contract flow, backlog and offshore project execution. For PVD and PVS, that is the layer of data that will determine whether the current move is just short-term noise or the first stage of a deeper repricing. Weak Brent with stable backlog is very different from weak Brent with fading work visibility.

Third, track refining margins, inventory and the retail pricing cycle. That is the filter needed for BSR and PLX. If you look only at Brent, you miss where profits are actually created or eroded.

Bottom line: This is not a single on-off switch

What affects your portfolio is not just whether Brent is at USD 76 or USD 80. More important is that the market is now using that price level to sort business models inside Vietnam's oil and gas sector. PVD and PVS are more sensitive to capital spending and work visibility. BSR is more sensitive to refining spreads and inventory. PLX is more sensitive to regulated pricing and distribution margins.

The cleanest conclusion after June 24 is that Vietnam's oil and gas stocks have entered a split-phase repricing, not a sector-wide verdict. Brent below USD 80 is the zone to monitor. But only if low oil prices persist and operating signals weaken at the same time does the market gain a strong case for a broader, deeper reset across the group. Over the next few sessions, the three signals that matter most are Brent, offshore work visibility, and margins in refining and fuel distribution.