Some sessions are easy to misread, especially for newer investors. June 23 was one of them: while major Asian benchmarks fell, the VN-Index still closed at 1,869.04, up 11.13 points, or 0.60%.Nhân Dân At first glance, the message looks simple. Vietnam was stronger than the rest of the region.

That reading is incomplete. An index can rise because the whole market is improving, but it can also rise because a small group of large-cap stocks is strong enough to pull the benchmark higher while much of the board remains weak. For investors who only watch the headline number, those two situations can feel the same. In practice, they are not.

That is what made June 23 worth unpacking. Vietnam did diverge from Asia at the index level, but the quality of that move was still narrow. In plain language, the green close did not mean money had spread evenly across the market.

Diverging from Asia did not mean broad strength

On the same day, the Nikkei 225 fell 3.5%, the KOSPI dropped 10.0%, and the Hang Seng lost 1.8%. Asia Financial tied that regional weakness to pressure on technology and semiconductor stocks, which hit North Asian benchmarks particularly hard.Asia Financial Vietnam stood out because its benchmark moved in the opposite direction.

But divergence is an observation, not yet an explanation. The next question is whether Vietnam moved higher because risk appetite broadened across the market or because the index is still heavily shaped by a small cluster of domestic heavyweights. In Vietnam, where index concentration matters, that distinction is critical.

If the first explanation were true, investors would expect more sectors to rise together, advancing stocks to outnumber decliners, and gains to show up well beyond the largest names. If the second explanation were true, the index could still climb even while many portfolios lagged behind. June 23 looked far closer to the second case.

Breadth was the number that mattered most

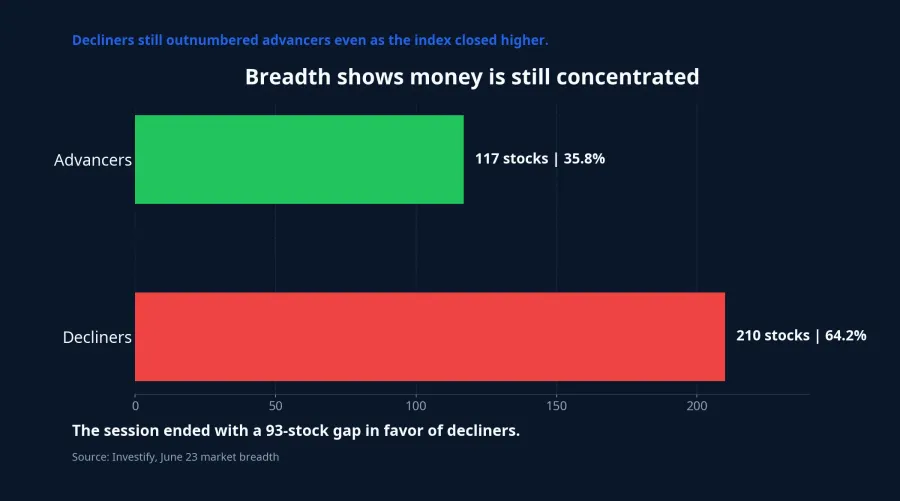

The easiest detail to miss in a positive index session is market breadth. By the close, HoSE recorded 117 advancing stocks against 210 decliners.Nhân Dân That means the average stock did not confirm the story told by the benchmark.

For newer investors, this is the real lesson. When the index is green but breadth is still red, the market is telling two stories at once. The benchmark says support is still there. Breadth says money is still highly selective and has not yet spread across the board.

That difference matters for real portfolios. If you owned the names attracting capital, the session felt constructive. If you were sitting in the larger pool of stocks outside the leadership group, the market may have felt much weaker than the headline move suggested.

Domestic heavyweights did the lifting

So where did the support come from? Nhân Dân reported that banks and real estate stocks were the main engines behind the gain, while HoSE turnover reached more than 945.41 million shares, with trading value above VND 30,989.01 billion.Nhân Dân Liquidity was not weak. It was simply concentrated.

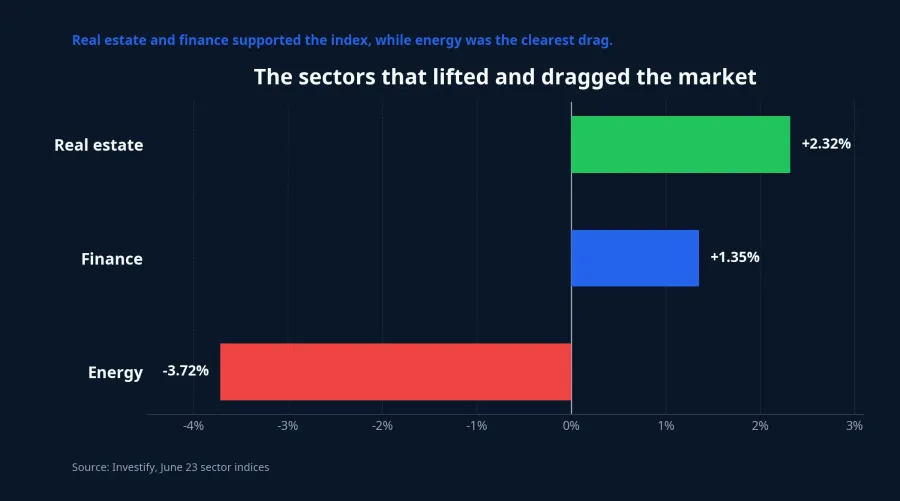

At the sector-index level, real estate rose 2.32%, finance gained 1.35%, and energy fell 3.72%. VNDIRECT described the same structure from a broader sector view: real estate rose 2.3%, banks added 1.1%, and only 4 of 19 sectors finished higher.VNDIRECT That 4-of-19 split alone tells you this was not a session where investors bought the whole market.

The stock-level picture made the mechanism even clearer. VIC rose 4.19%, VHM added 0.39%, VCB gained 0.33%, and BID increased 0.47%. These were not huge percentage moves, but they did not need to be. Their heavy weight in the index meant even modest gains could keep the benchmark moving higher.

In other words, VN-Index did not rise because hundreds of stocks improved together. It rose because a few large names were strong enough to lift the average. For retail investors, that is the difference between a broad-based market turn and an index move still driven by leadership concentration.

Foreign buying helped, but did not change the character of the rally

Another important part of the June 23 story was foreign flow. VNDIRECT said foreign investors were net buyers of VND 1,512.1 billion, with VIC alone drawing net purchases of VND 2,771.3 billion.VNDIRECT That helps explain why the leadership group had extra support even as regional sentiment stayed weak.

Still, it is important to separate “support” from “a change in market state.” Strong net buying in a handful of large-cap names can improve the index quickly. But if that capital does not spread to the rest of the board, the quality of the move remains narrow.

That is why the foreign-buying figure should not be treated as proof that the market has already entered a new, broad uptrend. The cleaner reading is more modest: foreign money supported the heavyweight complex, and that support was enough to let Vietnam outperform Asia at the index level. Evidence of a broader turn is still missing.

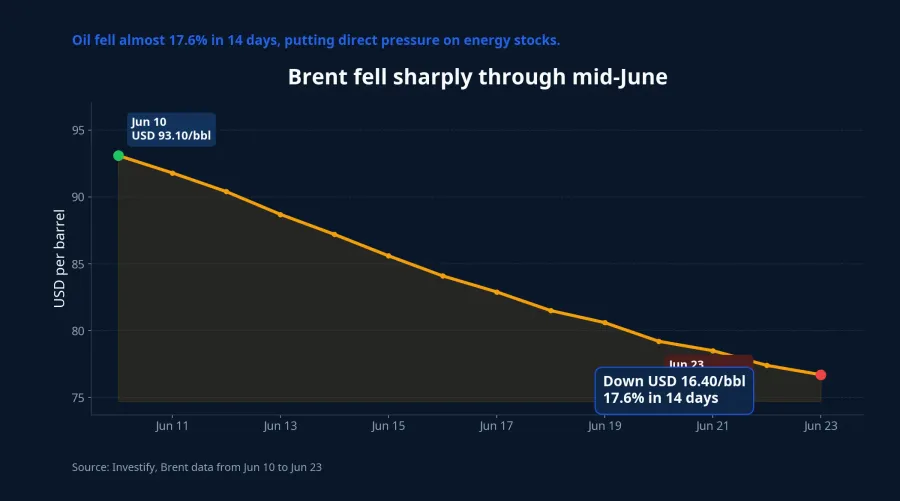

Energy showed external risk still mattered

If banks and real estate were the supportive side of the session, energy was the reminder that Vietnam was not insulated from external risk. Brent closed on June 23 at USD 76.70 per barrel, down from USD 93.10 on June 10. That was a decline of USD 16.40 per barrel, or 17.6%, in just 14 days.

The impact on Vietnamese equities was direct. The energy index dropped 3.72%, GAS lost 3.43%, and PVD fell 3.73%. VNDIRECT also identified oil and gas as the worst-performing group of the day, down 4.0%.VNDIRECT

That detail matters because it keeps the broader interpretation grounded. If Vietnam had fully detached from regional and global risk, the commodity-sensitive and sentiment-sensitive parts of the market would not have reacted that sharply. June 23 was better understood as a session with strong domestic support, not as proof that external risk had stopped shaping Vietnam's market.

What investors should watch after a session like this

After a day when Vietnam moves against the region, the key signal is not simply whether the benchmark stays green in the next session. The better test is whether breadth improves, whether more sectors participate, and whether stocks outside the heavyweight group begin to confirm the move. If those things do not change, the rally is still mostly an index-support story.

That leads to the clearest conclusion from June 23: Vietnam truly diverged from Asia at the benchmark level, but the move was still narrow in quality. Real estate, banks, and foreign buying did their job in supporting VN-Index. Until breadth becomes less skewed and sector participation broadens, the core market story remains the same: money is still choosing the pillars, not yet the whole market.