Not every technical circular from the State Bank of Vietnam moves the market in a meaningful way. This one matters because it is not about a system-wide credit loosening. It is about creating a separate channel for capital to reach a defined set of projects. For investors, that is the difference between a broad macro call and a tightly targeted policy mechanism.

On June 23, VietnamBiz reported that the State Bank had sent guidance to commercial banks on lending for projects proposed by Vingroup, Masterise Airport Infrastructure and Sun Group. The list covers 18 projects linked to APEC infrastructure, high-speed rail, Gia Binh International Airport and several PPP developments.VietnamBiz

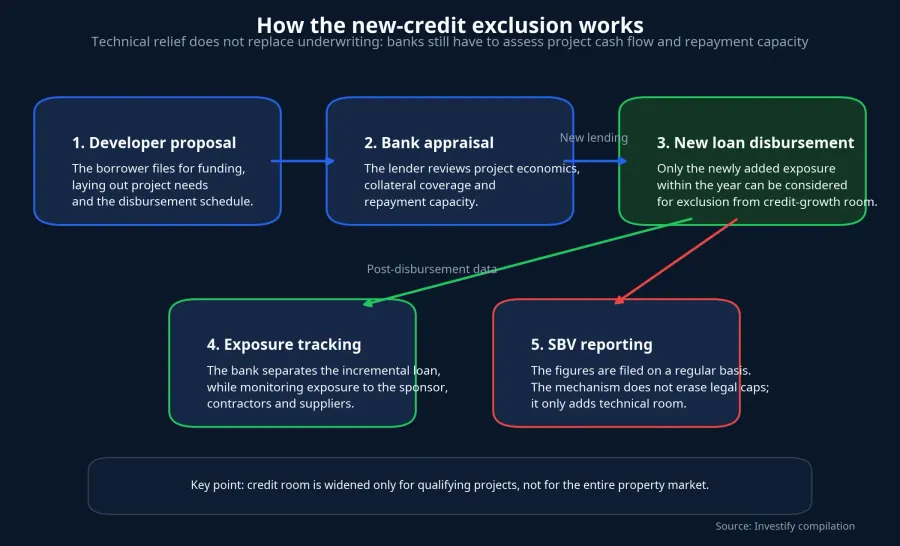

The key phrase is “newly arising credit exposure.” VietnamNet said fresh lending created each year for those projects can be excluded from a bank's annual credit-growth calculation.VietnamNet In plain English, that gives lenders a separate accounting lane for qualifying loans. It does not mean the SBV has opened the taps for the whole real-estate market.

What the mechanism actually changes

Under normal conditions, a bank making a large project loan has to manage two constraints at once. The first is credit quality: Is the project viable, will cash flow support repayment and is collateral credible. The second is annual credit-growth room: how much balance-sheet capacity remains for new lending during the year.

The new guidance does not remove the first constraint. Banks still have to assess feasibility, approve lending on their own balance sheets and protect operating safety.VietnamNet What it does ease is the second constraint, because the newly added exposure tied to those projects can sit outside the annual growth calculation. For lenders already running close to internal or regulatory limits, that technical relief can matter more than any vague talk of looser credit.

The opportunity created here is narrow but real. If legal paperwork is ready, project execution is credible and funding demand can be controlled, a project can move more quickly from expectation to disbursement. That is a very different story from saying the entire property sector has suddenly been rescued.

Who stands to benefit first

Banks are the first place investors need to read carefully. Not every lender benefits equally, because the upside exists only if the bank is actually involved in project finance, has underwriting capability in medium- and long-term loans and has enough risk capacity to stay with large exposures for years.

The June 23 trading session showed the market was already discounting that possibility. VN-Index closed at 1,869.04, up 11.13 points, or 0.60%. Among the names in focus, TCB rose 3.72% to VND 32,050 per share, VPB gained 1.92% to VND 26,500, VCB added 0.33% to VND 61,500 and VHM edged up 0.39% to VND 156,000. The numbers suggest money favored the stocks seen as more sensitive to project lending rather than buying the entire complex indiscriminately.

Still, a price reaction only tells you that investors are positioning for a more favorable disbursement path. It does not prove the benefit has already turned into earnings. A bank may gain technical room to lend, but if project approvals stall, contracts are delayed or syndication needs become too large, that extra room can remain theoretical for several quarters.

For developers and contractors, the immediate benefit is not a higher share price either. The more important shift is that access to medium- and long-term funding may no longer be squeezed inside the same annual lending envelope as ordinary commercial loans. When capital reaches projects on schedule, the beneficiaries extend beyond the sponsor to contractors, materials suppliers and infrastructure operators sitting inside the build-out chain.

Why this is not a blanket property easing

The scope of the guidance is still narrow. The source reporting makes clear that the mechanism is tied to a specific list of 18 projects, not to a broad expansion of credit for every real-estate company in the market.VietnamBiz

That matters especially for new investors because Vietnam's market often trades on keywords first and details later. Once a headline contains “property” and “credit easing,” speculative money can spread into stocks with little direct exposure. But if a project is not on the list, or if the company lacks the legal and operational readiness to turn policy into actual disbursement, the benefit is unlikely to reach financial statements.

It is also worth avoiding lazy causality. A stock rising on June 23 may reflect the new guidance, but it may also reflect broader market tone, short-term positioning or company-specific narratives. The evidence is strong enough to call the mechanism a credible catalyst. It is not strong enough to claim every rally in related names was caused directly by the SBV document.

Another layer of support for long-term lending

VietnamPlus also reported on June 23 that Circular 25/2026/TT-NHNN, amending Circular 22/2019/TT-NHNN, will take effect on July 1, 2026 and raise the cap on short-term funds used for medium- and long-term lending from 30% to 40%.VietnamPlus

Set beside the new-loan exclusion for the 18 projects, the bigger picture is that policy is moving through two separate channels. One is broader and improves the system's ability to fund medium- and long-term credit. The other is a conditional carve-out for nationally important projects. The two channels reinforce each other, but they do not make project risk disappear.

Execution risk remains the real filter. A bank may gain more technical balance-sheet room, yet still lend selectively if funding structure is fragile or liquidity pressure returns. Developers face the same reality. A more accommodating policy framework does not automatically fix permits, land clearance or end-demand cash flow.

The signals that matter next quarter

The next quarter should not be judged by how many stocks spike every time the market revisits this story. The more useful indicators are three concrete ones. First, which banks actually show up in loan commitments or syndicated deals tied to the priority project group. Second, whether disbursement progress matches construction and legal milestones. Third, whether the lending banks can expand project exposure without a deterioration in asset quality.

Those indicators answer the question the headline cannot: Is new capital reaching the right projects and generating real cash flow. If the answer is yes, the policy can create tangible upside for selected banks, infrastructure names and companies sitting inside the supply chain. If the answer is no, most of the effect will remain trapped in short-term price expectations.

Conclusion: capital priority is not profit priority

The cleanest thesis is that the SBV is creating project-level capital priority, not broad-based credit easing. That is positive for large projects with mature paperwork and for banks that can genuinely underwrite them. It does not automatically translate into profits for every bank or property stock after a few green sessions.

Over the next three to five years, Vietnam is likely to rely on more policy tools like this as infrastructure, logistics and large-scale development projects absorb more capital. For investors, though, the deciding variables remain unchanged: real disbursement, real funding capacity and real asset quality. When those three line up, policy turns into earnings. When one of them breaks, capital priority stays a paper advantage.