The 40% headline is easy to read as a clean positive for Vietnamese banks. That instinct is understandable, but it is still incomplete. For newer investors, Circular 25/2026 matters first as a balance-sheet change that gives banks more room to manage maturities. It does not automatically turn into higher earnings or a broad rerating for every bank stock.LuatVietnam

In simple terms, most deposits are short-term while many loans run for years. When banks are allowed to use a larger share of short-term funding for medium and long-term lending, maturity pressure eases. That can create more room for credit growth, but only if funding costs stay contained and loan quality does not deteriorate in the process.

What changes on July 1?

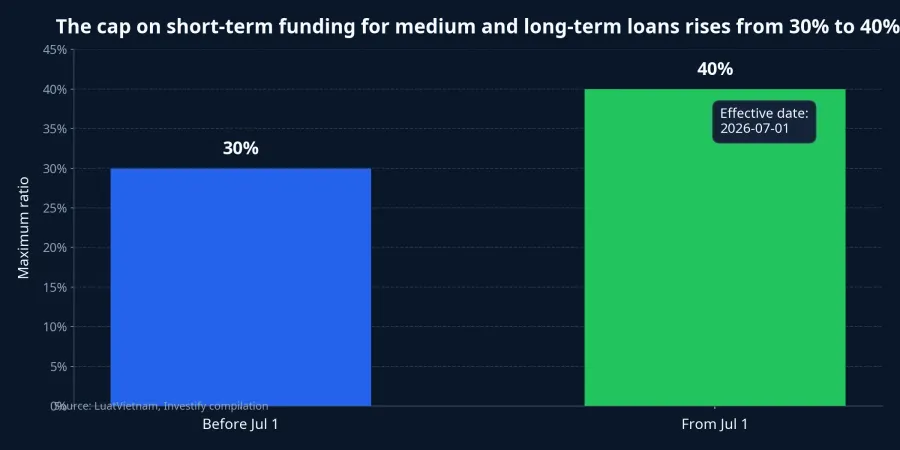

Circular 25/2026/TT-NHNN takes effect on July 1, 2026 and raises the maximum ratio of short-term funding that can be used for medium and long-term loans from 30% to 40%. This is no longer a proposal or a draft under consultation. It is an issued regulation with a clear effective date.LuatVietnam

The 40% ceiling is also not an unprecedented threshold. CafeF notes that the same level was in place in 2020 and 2021, before being reduced step by step to 37%, then 34%, and finally 30% from October 1, 2023. That context matters because it frames this move less as a radical rewrite of banking rules and more as a policy re-expansion after a period of tighter liquidity safeguards.CafeF

Put differently, moving the cap from 30% to 40% gives banks a larger buffer for long-duration loans such as mortgages, infrastructure projects, industrial parks or equipment financing. But more room is not the same as unlimited lending freedom. Banks still have to manage deposit costs, LDR, asset quality and whether loan yields are high enough to protect profitability.

LDR rules are changing as well. Deposits used in the LDR calculation still exclude escrow balances, customer funds held for specific purposes and demand deposits from the State Treasury. Term deposits from the State Treasury, however, are now only 80% excluded, meaning about 20% can be counted in the LDR denominator, or another ratio if the SBV sets one for a given period.CafeF

That sounds technical, but it matters when reading bank reports. A larger denominator makes the LDR constraint less tight on paper. Still, lower technical pressure is not the same as abundant real liquidity. If credit continues to expand faster than deposits, banks will still need to compete for funding, and the cost usually shows up in deposit rates.

The extra room will not be shared evenly

The first idea newer investors should discard is that every bank benefits equally just because the cap is being raised. That is not how the system works. Banks that were already closer to the old 30% threshold are more sensitive to the policy change because maturity pressure was more binding for them to begin with.

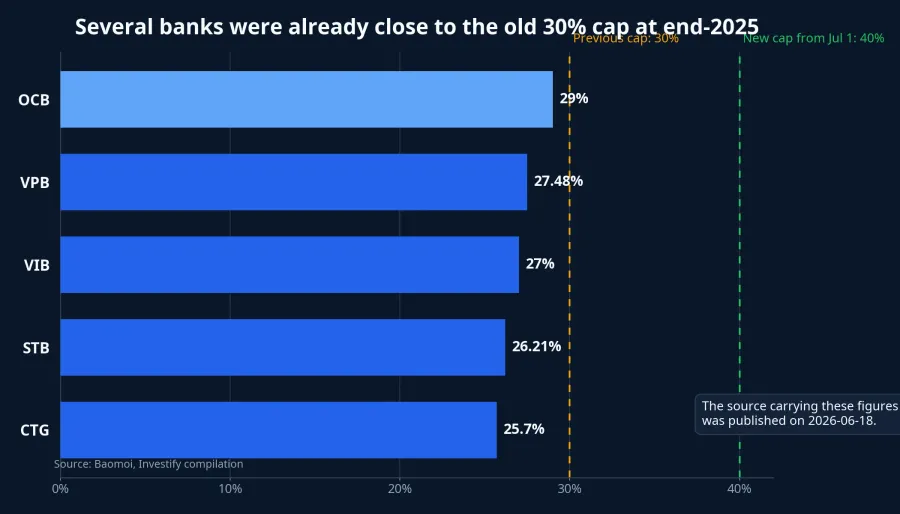

Baomoi reported on June 18 that medium and long-term credit grew by about 27% in 2025, faster than overall system credit growth. The same source said that by the end of 2025, roughly two-thirds of banks had seen their short-term funding ratio for medium and long-term loans rise versus the start of the year.Baomoi

Within that same data set, OCB stood at 29%, VPBank at 27.48%, VIB at 27%, Sacombank at 26.21% and VietinBank at 25.7%. Those levels were still below the old 30% ceiling, but close enough to show why restoring the cap to 40% could create a noticeable operating difference for selected banks.Baomoi

Still, being more sensitive to the policy change is not the same as saying those stocks will automatically outperform. Some of the expectation may already be priced in before the rule takes effect. The bigger question is how banks use the new capacity. If the additional room supports secured lending with clear repayment cash flow and manageable funding costs, the earnings effect becomes more credible. If growth comes at the cost of expensive deposits or weaker asset quality, the policy benefit can narrow quickly.

On the borrower side, sectors that rely heavily on long-duration capital such as real estate, manufacturing, infrastructure and industrial parks could benefit from the looser cap.Đầu tư But the inference still needs discipline. Easier funding does not turn a weak project into a strong one. Companies still need demand, cash flow and repayment capacity, and banks still have to underwrite risk the old-fashioned way.

Three signals newer investors should watch after July 1

The first signal is long-term deposit rates. If the circular genuinely reduces the need to fight for long-duration funding at any cost, funding pressure should ease. If 12-month and 24-month deposit rates remain elevated at banks that were near the old cap, the market will conclude that the structural funding problem has not really gone away.

The second signal is the composition of credit growth in quarterly reports. Many first-time investors stop at the headline number, asking only how many percent lending grew. That misses half the story. What matters is where the growth sits: mortgages, industrial parks, production lending or riskier segments. If credit expands while asset quality stays stable, then the policy room is starting to translate into operating value.

The third signal is NIM. It rarely gets the same attention as top-line credit growth, but it is the cleaner read on whether banks are preserving their earning spread. A bank can lend more after the cap is lifted, yet if it has to pay up for deposits and NIM contracts, the earnings story is still unresolved.

That is why July 1 should not be read as a sector-wide buy signal. It is better understood as the start of a test. The question is whether banks can convert this new technical room into good credit growth without losing control of funding costs. Newer investors do not need to predict the full outcome today. They only need to track these three operating signals over the next few reporting cycles.

Conclusion: a starting point, not an end result

Circular 25/2026 gives Vietnam’s banking system more operating space, especially for institutions that had moved close to the old 30% ceiling. It is a real policy change in technical terms because it reduces maturity pressure and loosens parts of the LDR calculation for certain deposit components.LuatVietnam

But the more important point for individual investors is this: technical room is not the same as earnings already delivered. If long-term deposit rates do not cool, if credit quality weakens, or if NIM compresses, the upside from the circular will narrow. The disciplined reading after July 1 is therefore not “banks got relief so the whole sector wins,” but “banks gained more technical room, and now the operating data has to confirm the rest.”