Many savers are looking at deposit boards and reaching the same conclusion: if a few banks have already cut rates, it may be better to stay short and wait for another round. The problem is that the market is not moving in a straight line. As long as credit keeps expanding faster than deposits, banks still need funding costs that are attractive enough to hold on to liquidity.Tin Nhanh CK

That leads to a useful takeaway for first-time investors. Rates may ease at selected banks or selected tenors, but there is still little evidence of a broad, fast decline across the system. The more practical framework is not to predict the next rate cut perfectly, but to separate the cash you may need soon from the cash you can afford to lock up.

Why deposit rates are not easy to push down

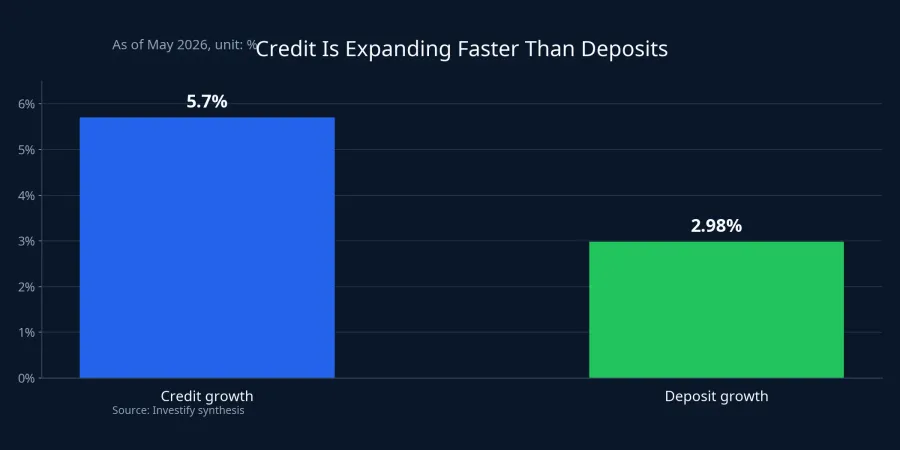

The mechanics are fairly simple. If banks want to lend more, they need enough deposits to support that loan growth. Tin Nhanh Chứng Khoán reported that credit growth had reached 5.7% year to date by the end of May, while deposit growth was only 2.98% over the same period.Tin Nhanh CK That gap does not mean the system is suddenly short of money, but it does suggest banks still have limited room to slash funding costs aggressively.

The latest cuts also need to be read in context. Vietnamnet noted that NCB reduced rates by only 0.1 percentage point on selected 6-12 month tenors, while online rate tables published the same day still showed relatively high offers at medium and longer maturities.Vietnamnet In other words, a few isolated moves do not yet amount to a system-wide easing cycle.

Inflation matters as well. The same Tin Nhanh Chứng Khoán report cited the view that inflation is approaching 4% and could move above 4.5% by year-end if imported energy and commodity pressures remain elevated.Tin Nhanh CK If deposit rates fall too quickly while price pressure remains sticky, savings become less attractive and banks may have to restore incentives later to defend funding.

The tenor premium is still visible

New investors often focus on short-tenor rates because those are easiest to compare at a glance. But the more important signal is the yield pickup available when money is locked up for longer. Vietnamnet reported that 1-3 month online deposit rates at many banks were around 4.75% per year, while ACB offered as much as 7.1% per year for 6 months and 7.3% per year for 12 months. The Big 4 banks were around 6.8% per year for 12 months, with PGBank near 7.0% and Saigonbank near 7.2%.Vietnamnet

Thời báo Tài chính Việt Nam also noted in mid-June that 6-month rates at many banks were still clearly above the 1-3 month band.Thời báo TCVN That matters because it shows what savers are really being paid for: not risk in the equity sense, but lower flexibility.

So the more useful question is not “are rates about to fall again?” but “do I actually need this money in the next few months?” If the answer is yes, the extra yield may not be worth the loss of flexibility. If the answer is no, locking in a portion of today’s rate can make far more sense than simply waiting.

Short tenors are a way to buy flexibility

Short deposits fit cash that still has an uncertain use date. That could be an emergency reserve, tuition money, a home repair budget, working capital for a small business, or simply a pile of cash waiting for another investment opportunity. The main benefit here is not the headline yield. It is the ability to move without forcing yourself into an expensive early withdrawal.

The early-withdrawal rule is exactly where many beginners make mistakes. Vietnam Deposit Insurance notes that under the current rules, a full early withdrawal is typically paid at no more than the institution’s lowest non-term deposit rate at the time of withdrawal, while a partial early withdrawal may still allow the remaining balance to keep the originally agreed rate depending on the product terms.BHTG Việt Nam

Put simply, a short tenor can protect you from a costly mistake: locking money away because the quoted rate looks better, only to pull it out weeks later and give back most of the promised interest. The price of that protection is a lower yield. That is a real trade-off, not a sign that the shorter option is inferior.

Locking yield early means giving up flexibility for certainty

The picture changes if part of your cash is genuinely not needed for the next 6-12 months. At that point, you are not paying for the option to wait. You are paying for certainty in future cash flow. In a market where deposit rates may stay sticky, locking in a fixed yield early can make financial planning easier, especially for people who value predictable income and do not want to monitor deposit tables every week.

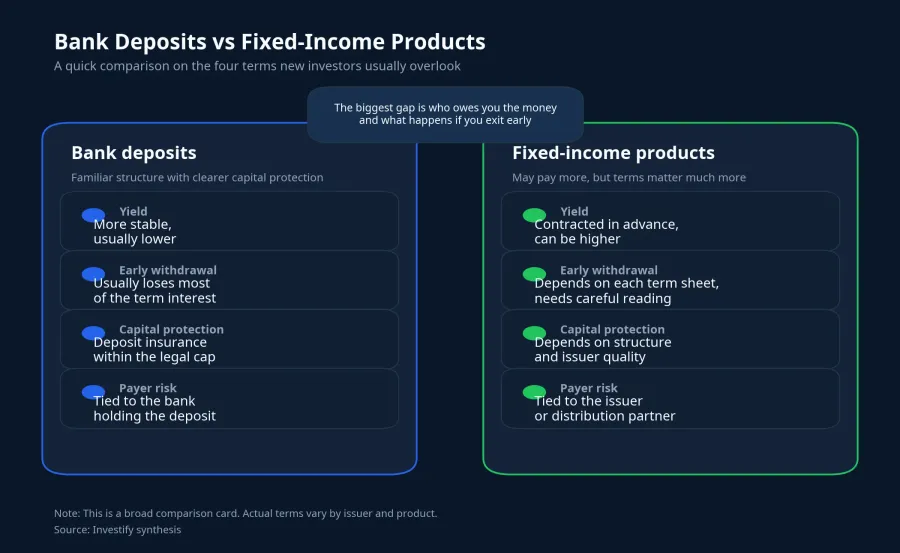

Still, “fixed income” does not automatically mean “same risk as a bank deposit.” The Government News portal says the current deposit insurance payout cap is VND 125 million per person per participating institution, covering both principal and interest.Báo Chính phủ Bank deposits come with a relatively clear legal protection layer. Fixed-income products outside traditional deposits require a different checklist: who ultimately owes you the money, whether there is collateral, how buyback or exit works, and what penalties apply if you need liquidity early.

That distinction matters even more in the private bond market. A LuatVietnam legal update published on June 5, 2026 says individuals must qualify as professional investors to buy, trade, or transfer privately placed corporate bonds, including maintaining a securities portfolio worth at least VND 2 billion for a minimum of 180 days.LuatVietnam The access rule alone shows that this is not simply a higher-yield version of a savings account.

A practical cash-bucketing framework

The simplest useful framework is to split money by the date you may need it, not by whichever institution posts the highest advertised rate. Cash that might be needed within 1-3 months is better suited to shorter tenors. Cash that is clearly not needed for 6-12 months is the portion that can be compared against medium tenors or more transparent fixed-income products.

When comparing those options, stop at neither the advertised yield nor the marketing label. Ask four questions instead: can you exit early, how much interest do you lose if you do, who is legally responsible for repayment, and where does capital protection actually come from. An 8.0% annual return is not automatically better than 6.8% if the withdrawal terms, payer risk, and protection layer are fundamentally different.

The core thesis is straightforward. With credit still expanding faster than deposits and the gap between short and longer tenors still wide, the market does not yet support a fast, broad-based drop in deposit rates. That is why the better move for idle cash is not trying to time the next cut, but building tenors around your own liquidity schedule and tolerance for contractual constraints. The signals worth watching in the next few weeks are the credit-deposit growth gap, inflation, and whether rate cuts start spreading across a wider group of banks.