A 15% credit growth headline sounds large enough to make new investors think the entire banking sector is about to move in lockstep. But in the market, credit is only the first line of the story. Stocks react when investors believe that loan growth can flow through the balance sheet, preserve margins and avoid building a bigger bad-loan problem on the other side.

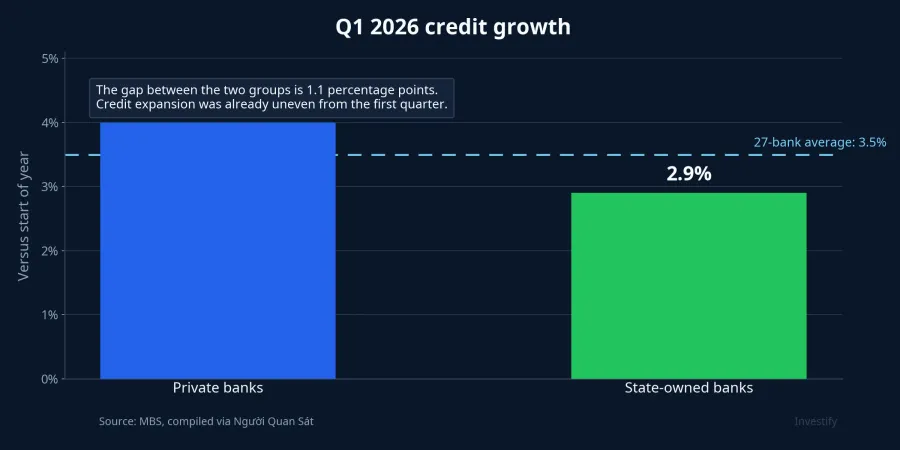

According to a June 22 Người Quan Sát article citing MBS, credit growth at 27 listed banks reached 3.5% from the start of 2026 by the end of the first quarter, versus 3.8% in the same period last year, while full-year growth is projected at around 15%. In the same dataset, private banks expanded credit by about 4.0%, while state-owned banks were at 2.9%.Người Quan Sát In plain terms, the lending cycle was already uneven in the first quarter, so there is little reason to expect bank stocks to move as one block.

For first-time investors, that is the core point: “banks” is not a single trade. The same positive headline can reward lenders that still have room to extend credit, while leaving behind banks that are still constrained by liquidity, NIM pressure or asset-quality issues. The working thesis here is straightforward: a 15% credit outlook is a favorable backdrop, but any upside in listed bank shares is still more likely to be stock-specific than sector-wide.

Credit growth does not automatically become a sector rally

The simple way to think about credit is as future revenue for a bank. Higher lending means a bigger loan book, but profit only follows if the bank does not have to pay much more for deposits, squeeze its NIM to stay competitive, or accept weaker credit quality to keep volume growing. The same top-line growth target can therefore translate into very different earnings outcomes across banks.

The striking part of the MBS data is that private lenders are currently growing faster than state-owned banks.Người Quan Sát That does not guarantee that private-bank shares will lead, but it does show that the starting point is already different across groups. Once starting points diverge, the market rarely pays for a broad “all banks are healthy” narrative. It starts asking where the growth sits and how clean that growth really is.

MBS also singled out the relative winners: banks with low LDR such as ACB and HDBank, banks with high current-account and savings-account ratios such as VCB, TCB and MBB, and banks with stronger asset quality such as CTG, VCB, ACB and TCB.Người Quan Sát In other words, investors are not just asking which bank can lend more. They are asking which bank can do it with lower funding costs and a safer balance-sheet profile.

The tape has already shown a split

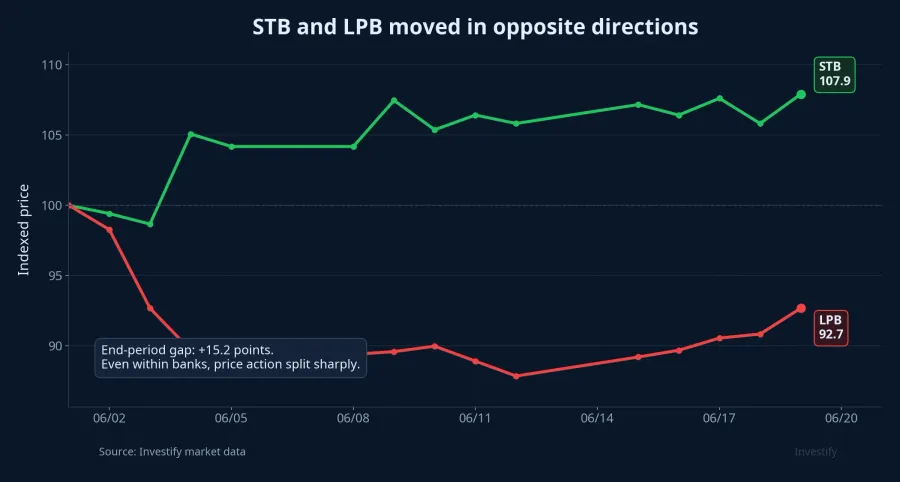

If that still sounds abstract, price action has already made the point more clearly than commentary can. From June 1 to June 19, STB rose from VND 67,000 to VND 72,300, an increase of about 7.9%. Over the same period, LPB fell from VND 51,800 to VND 48,000, or roughly 7.3%. They are both bank stocks, yet the market treated them as very different stories.

That matters because it reminds newer investors that the market moves ahead of headlines. If the 15% credit outlook were truly being priced as a sector-wide catalyst, the banking group would show much more uniformity in both price action and liquidity. The fact that STB and LPB diverged so sharply suggests that capital is still choosing specific setups, not buying banks as a single basket.

The VN-Index closed at 1,824.53 on June 19, but dispersion inside the banking group remained obvious. The confirmation signal is therefore not whether the index is green in one session. It is whether banks with similar balance-sheet advantages start moving together. If VCB, CTG, MBB, TCB, ACB and HDB all improve turnover and hold up better than the broader market, then investors are finally paying for credit headroom as a group theme.

Policy support exists, but it arrives in clusters

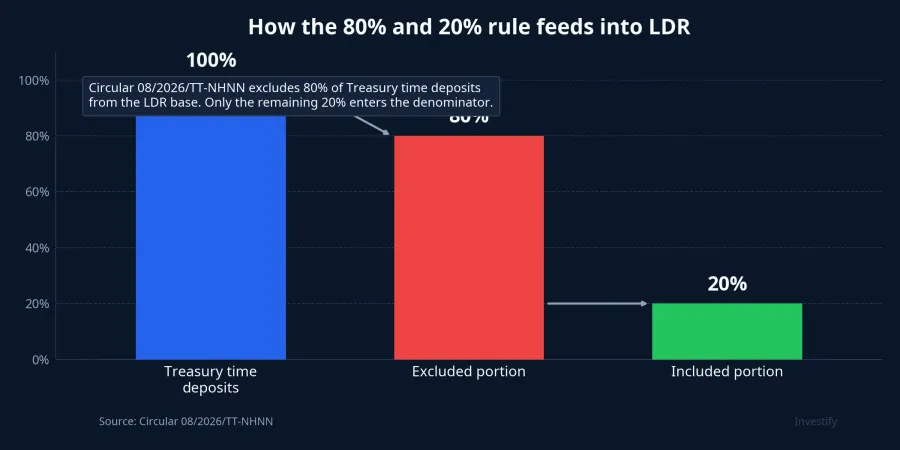

Part of the story sits in the regulatory framework. Circular 08/2026/TT-NHNN, effective from May 15, 2026, says banks must exclude 80% of Treasury time deposits when calculating LDR, while only the remaining 20% counts in the denominator.Chính phủ This is a structural rule change, and the rule itself already implies that the benefits will accrue more to lenders that can actually make use of that funding base.

The distinction that matters is between “support exists” and “support is evenly distributed.” The new LDR formula does not lift all banks to the same degree. It creates a clearer relative advantage for lenders whose funding structure matches the rule better, so stronger performance by state-owned names would be a logical response rather than a surprise.

Another layer comes from banks involved in compulsory transfers. A June 21 Người Quan Sát article, again citing MBS, says Circular 23/2025/TT-NHNN cuts reserve requirements by 50% for that group. For VND deposits with maturities below 12 months, the ratio falls from 3.0% to 1.5%, while deposits of 12 months or more drop from 1.0% to 0.5%.Người Quan Sát Put simply, less funding is locked away, which leaves more room to turn deposits into credit growth.

Foreign ownership limits are another part of the puzzle, but they need to be framed carefully. Người Quan Sát, via MBS, says Decree 69/2025/NĐ-CP raises the foreign ownership cap to 49% for banks receiving compulsory transfers, except for banks where the state owns more than 50% of charter capital. MBS highlighted HDBank, MB and VPBank as lenders that could benefit more directly from that change.Người Quan Sát The key takeaway is that this is still a cluster advantage, not a master key for the whole sector.

NIM and bad loans still cap the upside

A common mistake among newer investors is to see faster credit growth and assume profits will follow automatically. In practice, bank earnings still run through NIM and asset quality. If a lender has to pay more for deposits to support growth, or if new lending shifts toward riskier segments, the revenue benefit can be diluted very quickly lower down the income statement.

MBS argues that retail lending is recovering more cautiously because lending rates remain higher than a year ago and the legal environment has changed more meaningfully. Real-estate lending is also being steered away from speculative and high-end segments.Người Quan Sát That means higher credit volume does not automatically imply a clean NIM cycle, especially for banks that still need to fight for funding or lean on more sensitive lending books.

At a deeper level, bad-loan resolution remains a process, not an instant quarterly result. Người Quan Sát, again citing MBS, says the codification of rules previously used under Resolution 42/2017 could make collateral recovery and debt handling more transparent. Báo Chính phủ also reported that Resolution 79-NQ/TW calls for a stronger role for VAMC in resolving bad loans.Người Quan SátBáo Chính phủ But that is still a medium-term mechanism story, not proof that profits are about to jump across the board.

What investors should watch next

The clean conclusion is this: credit growth around 15% is supportive for Vietnamese banks, but any price move is still more likely to run through pockets of advantage than through a uniform sector rerating. The first pocket includes banks with liquidity room, looser LDR positions, lower funding costs and steadier asset quality. The second includes banks that benefit more clearly from regulatory adjustments, such as compulsory-transfer recipients or lenders better positioned in the funding-rule story.

What could change that picture is the second-quarter reporting season and the actual path of NIM, funding costs, newly formed bad loans and credit absorption at each bank. If those indicators improve broadly at the same time, the narrative can expand from selective stock picking to a wider group call. For now, the more defensible reading is that the positive headline belongs to the sector, but the stock-market reward still belongs mainly to banks with balance sheets strong enough to turn credit growth into real profit.