Vietnam's steel industry is no longer telling a purely defensive story. Output has rebounded visibly in the first five months of 2026, and that alone is enough to pull many newer investors toward a simple conclusion: the cycle is turning, so steel stocks should rise together. That reading is too shallow. A recovery in volume can be real while the recovery in profits remains uneven across the chain.

In plain terms, output tells you factories are running harder. Profit tells you something more selective: who sells the right product mix, who buys inputs at the right cost, and who can still protect margins once orders return. The rebound is real, but it is not a one-line bullish case for the whole sector.

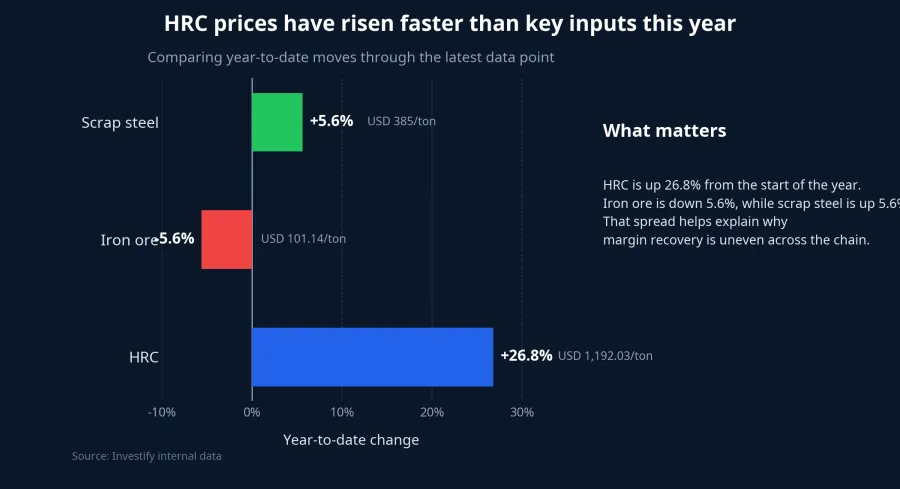

The volume rebound is now hard to ignore

In the first five months of 2026, Vietnam's crude steel output reached 12.55 million tons, up 26.4% from a year earlier. Finished steel output came in at nearly 14.91 million tons, while sales reached 14.93 million tons, also posting double-digit year-on-year growth.Dân Việt Those figures matter because they move the discussion beyond vague optimism. They show that the industry has already entered a measurable recovery in volume.

The more important detail sits inside hot-rolled coil, or HRC. Over the same period, HRC output reached 4.38 million tons, up 37.3%, while HRC sales rose 32.5%. Construction steel also improved, with output up 18.7% and sales up 14.7%.Dân Việt That is not a side note. HRC feeds coated steel, steel pipes, machinery and part of the construction chain, so a faster rebound in HRC changes how investors should read the sector.

Investify's internal pricing data adds another layer. From the start of the year to June 22, 2026, HRC rose from USD 940 per ton to USD 1,192.03 per ton, an increase of about 26.8%. Over roughly the same window, iron ore fell from USD 107.17 per ton to USD 101.14 per ton on June 18, a decline of about 5.6%, while scrap steel rose from USD 364.5 per ton to USD 385 per ton, or about 5.6%. In everyday language, one key selling price is rising much faster than most of the major inputs feeding the industry.

That spread is exactly why “higher output means everyone wins” is the wrong takeaway. A company selling HRC or construction steel may benefit when selling prices improve faster than input costs. A downstream producer that has to buy HRC first and then compete aggressively at the customer end may not keep that same advantage.

Which links are capturing the upside

The clearest beneficiaries are upstream players or businesses that control HRC capacity. When HRC output is rising quickly and HRC prices are climbing faster than iron ore and scrap, the front end of the chain gets a better chance to widen margins. This is where new investors often oversimplify the story, because sector-level output does not mean sector-wide profit symmetry.

The second group is tied more closely to domestic demand, especially construction steel. Dân Việt reported that construction steel posted gains in both output and sales during the first five months of the year.Dân Việt Domestic D10 steel prices also moved from VND 13,600 per kilogram at the start of the year to VND 15,120 per kilogram on June 22, 2026. That does not guarantee an immediate jump in earnings, but it does suggest that public investment, infrastructure work and residential construction are creating a firmer domestic floor than before.

The third group is the part of the industry still constrained by exports, especially coated steel and color-coated products. In the first five months of the year, total steel exports reached only 2.26 million tons, down 8% from a year earlier. Within that, coated steel and color-coated steel were weaker, with output down 15.1% and export value down 32.6%.Báo Xây Dựng This is the part of the picture that keeps the sector from looking flat. Domestic demand is improving, but any company still leaning heavily on overseas markets or pressure-filled coated steel segments is likely to see a slower profit recovery.

One discipline matters here: avoid forcing a single cause onto every stock move. The available evidence supports three points with reasonable confidence: sector output is recovering, HRC is the stronger link, and coated-steel exports remain weak. But there is still a large middle layer between those facts and each company's equity story: inventory, end-market contracts, financing costs and export dependence.

What newer investors should watch beyond output

For newer investors, the cleanest framework is to split the sector into three questions instead of one. First, where does the company sit in the chain: crude steel, HRC, construction steel, or downstream processing that buys HRC and resells a finished product? In the same cycle, chain position can make a major difference to margin outcomes.

Second, where does demand come from. A business tied to domestic construction can ride public investment and local project activity differently from one that depends on export orders. If the order book still leans heavily on weaker overseas markets, the recovery can remain volume-light or price-sensitive even while the domestic story improves.

Third, investors need to read margins, not just tonnage. When HRC is rising faster than iron ore and scrap, it is fair to expect that some upstream names should breathe easier. But that expectation only becomes durable if upcoming quarterly reports show better gross margins, manageable inventory and financing costs that do not erase the operating improvement.

Conclusion: The rebound is real, but it is not a sector-wide profit story

The most defensible conclusion right now is that Vietnam's steel rebound is already visible in both production and sales, not just in market sentiment. But the new cycle is not delivering profits in a straight line. The advantage appears to lean toward HRC-linked and upstream businesses, as well as companies with stronger exposure to domestic demand, while coated steel and export-heavy segments still require more caution.

So the right thesis is neither “buy steel” nor “avoid steel.” A better conclusion is this: the cycle has turned in volume, but steel equities become compelling only when a company can convert higher tonnage into real margin expansion. The signals worth monitoring over the next few quarters are the spread between HRC and its inputs, the strength of domestic construction demand, and whether export orders recover in coated steel. If those three start to move together, the story becomes more complete. For now, treating the entire sector as one uniform trade is still the easiest way to misread it.