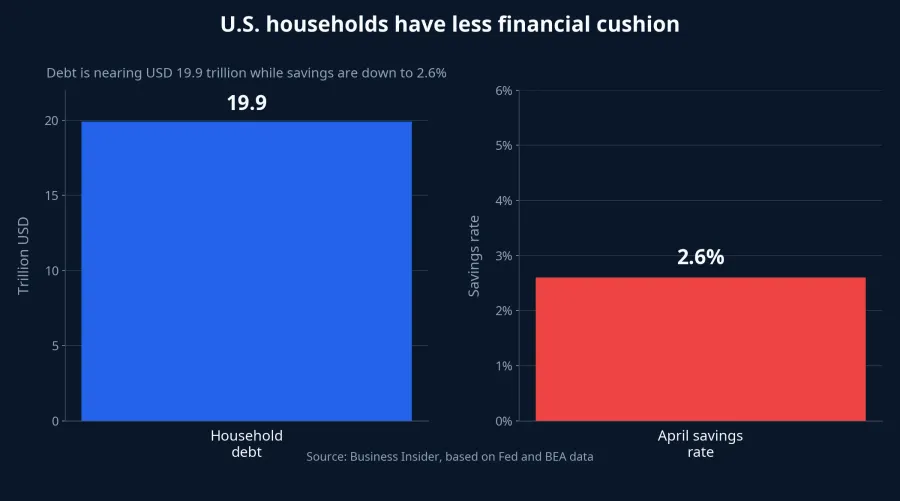

Last week looked reassuring if you watched only the index board. The Nasdaq rose 2.4%, while the S&P 500 gained 0.9% in the holiday-shortened week that ended on June 19.AP At the same time, Business Insider, citing Fed and BEA data, reported that U.S. household debt is nearing USD 19.9 trillion and that the personal savings rate has fallen to 2.6% in April.Business Insider

Those numbers do not actually contradict each other. They describe the same market from two different layers. Asset prices are still strong enough to support confidence, even as households have less cash cushion than they did before. For newer investors, that distinction matters. A rising market is not automatically proof that the consumer is getting healthier. Sometimes it simply means higher asset prices are delaying the point at which households feel forced to cut back.

What is still carrying the rally

You can think of it this way: stock indexes do not price the financial condition of each household in a straight line. In the short run, markets respond more to corporate earnings, leadership from mega-cap technology, passive flows into index funds, and technical momentum. That is why one strong week in the Nasdaq or the S&P 500 is not enough to say the consumer backdrop has improved to the same degree.

That helps explain why an uncomfortable consumer data set has not pulled the market lower right away. The major U.S. indexes are still heavily driven by companies with profit engines that look stronger than the rest of the economy. As long as those earnings expectations hold, the broader indexes can keep rising even if the average consumer is losing some room to absorb shocks.

Still, it would be too neat to claim there is only one explanation. At least three forces are operating at once: strong earnings expectations for market leaders, supportive technical positioning, and a wealth effect that is keeping households from reacting too aggressively to tighter finances. The current evidence supports that third factor as an important cushion, but not as the sole explanation for the rally.

Why thinner savings have not cracked spending yet

Business Insider captures the current U.S. contradiction well. Household debt is approaching USD 19.9 trillion, while the personal savings rate is down to just 2.6%, a very thin level by recent standards.Business Insider In plain terms, households are leaning more on credit while holding less room for error.

But spending does not break the moment savings drop. In real life, households do not base every spending decision on cash alone. They also look at retirement accounts, index-fund balances, home values, job security, and the belief that future income will still be there. When stocks keep climbing, the wealth effect kicks in. People feel richer on paper, so belt-tightening tends to arrive later than the raw savings number might suggest.

That is why a strong stock market can temporarily mask the thinner spots in the household balance sheet. Families keep dining out, replacing appliances, and carrying on with normal purchases because they do not yet feel forced to stop. The real risk is that this confidence depends on asset prices staying firm. If markets reverse or labor conditions weaken, the already-thin cushion becomes visible very quickly.

The wealth effect does not remove risk, it delays it

The simplest way to describe the wealth effect is as a temporary bridge. As long as stock prices and home values are rising, that bridge helps households move through a period of pressure without cutting spending sharply. But the bridge does not erase debt, and it does not refill savings accounts.

That is an important distinction for retail investors. A rising price trend and a durable consumer backdrop are not always the same thing. The market may be reflecting confidence that large listed companies can continue to grow earnings. Household data, meanwhile, is telling a different part of the story: the average consumer has less ability to absorb bad surprises. Both can be true for a while.

One useful framework is to split the picture into two layers. The top layer is asset prices, valuation, and momentum in market leaders. The bottom layer is savings, debt, and household resilience. As long as the top layer holds, the bottom layer may not crack immediately. But if the top layer wobbles, the lower layer no longer has much cushion left.

What newer investors should watch next

There is no need to turn this into an extreme forecast that U.S. stocks are about to collapse. A more defensible conclusion is that the rally can continue, but it is leaning on a consumer backdrop with less spare capacity. So instead of watching whether the Nasdaq closes green or red in one session, newer investors should watch the indicators that speak to how durable spending really is.

The first is the personal savings rate. When that figure stays too low for too long, even a modest shock from fuel costs, borrowing costs, tuition, or housing can force households to adjust their budgets faster. The second is the direction of consumer credit and delinquency trends. The issue is not simply that debt sounds large. The issue is that high debt combined with low savings shortens the margin of safety if the job market cools.Business Insider

The third is how discretionary consumer stocks behave. If the real consumer picture starts weakening, that is often where stress appears before it shows up clearly in broad indexes that are still being carried by a handful of very large companies. When that group loses momentum while the headline index remains positive, it can be a sign that the market's surface and its foundation are moving out of sync.

Conclusion: The rally is intact, but the margin for error is thinner

The core thesis here is straightforward. The U.S. stock rally is still intact, but it is traveling alongside a consumer with less cushion than before. That does not force an immediate reversal next week. It simply means that if asset prices stop supporting confidence, spending could react faster than it did in periods when households had more cash on hand.

The most useful checklist over the next two weeks is not a guess about the top or bottom in the S&P 500. It is a short watch list: fresh savings-rate data, consumer-credit stress, and whether market leaders can keep carrying the indexes on their own. If those three still hold together, the rally can keep running. If one of them breaks, the market will have to answer the question that last week's green screen only postponed.