What changed this week was not the existence of risk itself, but the price investors were willing to pay for safety. Just a few days ago, SJC gold was trading above VND 150 million per tael. By the end of the week, that threshold was gone, while the VN-Index had also managed to break a four-week losing streak. At a glance, that combination invites an easy narrative: money is leaving gold and going back into stocks.

A closer read suggests the market is not saying that much yet. Put simply, gold has become less overheated, while equities have merely become less weak. Those are not the same thing. One points to cooling defensive demand; the other only suggests that selling pressure is no longer as aggressive as it was before.

The market is paying less for protection

On June 15, SJC gold was quoted at VND 148-150.5 million per tael, meaning the selling price had already climbed above the VND 150 million threshold.VietNamNet By the morning of June 20, that range had eased to VND 144.2-147.2 million.VietNamNet On June 19 alone, the selling price had slipped to VND 146.7 million. A retreat of several million dong per tael over a few sessions does not mean risk has disappeared, but it does show investors are less willing to pay a premium simply to own a defensive asset.

For newer investors, VND 150 million per tael works more like a psychological line than a purely numerical one. When price moves above that level, people with cash on the sidelines can quickly feel as if they are falling behind if they do not buy gold. When price drops back below it only days later, the first thing that changes is not that the world suddenly becomes safer. What changes is the premium the market attaches to safety. In other words, investors are no longer paying such an extreme price for fear.

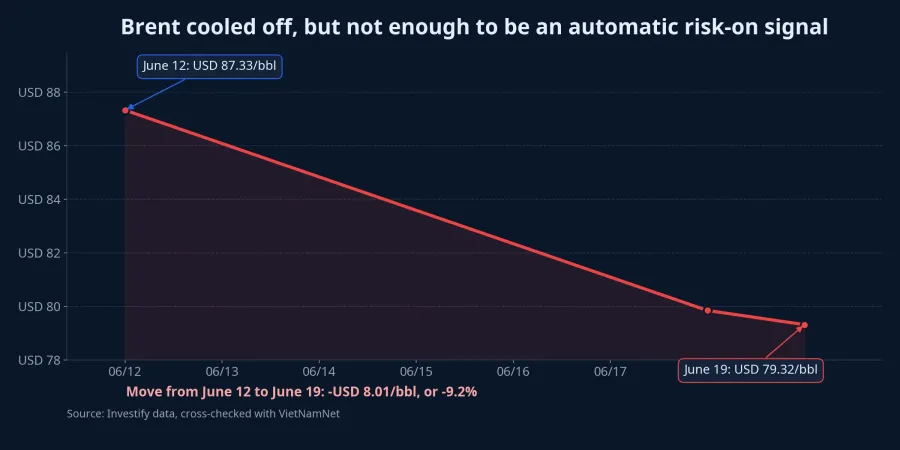

Brent crude tells a similar story, though not one that automatically validates a risk-on call. Based on Investify data, Brent fell from USD 87.33 per barrel on June 12 to USD 79.32 on June 19, a drop of 9.2%. VietNamNet separately reported Brent at USD 79.85 at the close of June 18.VietNamNet Lower oil prices reduce inflation pressure and ease geopolitical nerves. But if oil is falling because growth expectations are weakening, that is a more cautious signal. Brent therefore makes the backdrop less tense, but it does not, by itself, switch equities into a clean risk-on regime.

This is where readers can easily overstate what happened. Gold cooling off and oil moving lower can occur alongside a rebound in the index, but that still does not prove capital has decisively left its defensive posture. When one signal says fear is easing and another says selling pressure is becoming less intense, investors should be careful not to confuse “less bad” with “already good.”

The VN-Index has stopped falling, but buying has not broadened

On June 19, the VN-Index fell 5.94 points to 1,824.53. Even so, the index still gained 32.88 points over the full week, or 1.83%, enough to end a four-week losing streak.ĐTCK That matters, because after weeks of steady pressure, the market finally managed to create a clear pause in the decline. But ending a losing streak is not the same as regaining broad upward momentum, and that second step is what matters if money is truly rotating.

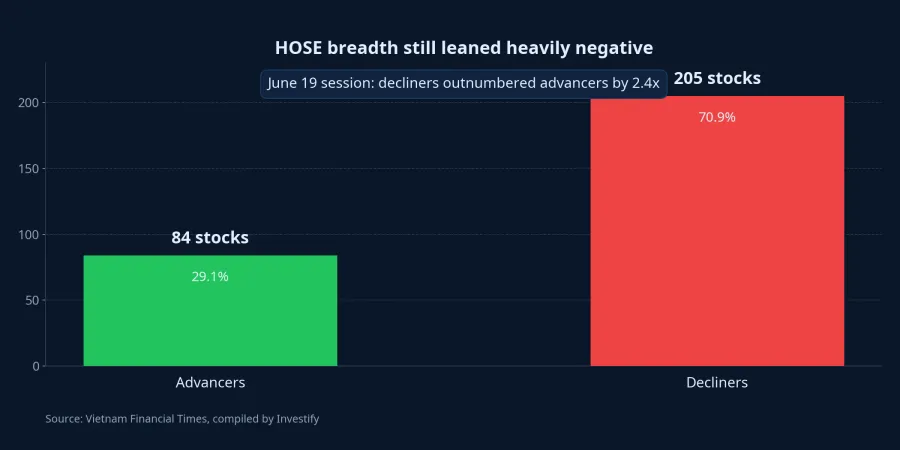

The real issue is breadth. On HOSE on June 19, there were 84 advancing stocks and 205 declining stocks.TBTCVN Matched trading value came in at roughly VND 18.803 trillion, while foreign investors posted net selling of VND 1.621 trillion.TBTCVN Those figures say something straightforward: the index may be stabilizing, but many portfolios are not recovering with it.

Think of the market as a classroom. If only a handful of students are answering correctly, it is hard to say the entire class has understood the lesson. The same logic applies here. A small group of large-cap names may be strong enough to support the headline index, but when decliners still heavily outnumber advancers, liquidity remains uneven, and foreign investors are still selling hard, the rebound is still narrow rather than broadly shared.

That distinction matters especially for retail investors, who often look at the index first and their own holdings second. That habit can easily create the impression that the market is regaining strength while they are somehow missing out. In reality, the move may still be concentrated in a limited set of heavyweight names. Until breadth improves, the green headline on the index still needs to be tested against a simple question: who is actually benefiting from that rebound?

The exchange rate remains the final filter

If gold shows that defensive demand has cooled and stocks show that broad selling has become less intense, then the exchange rate is what tells us whether that shift can last. On the morning of June 19, the State Bank of Vietnam’s central rate stood at VND 25,181 per US dollar, up by VND 8. At the same time, the free-market dollar traded around VND 26,520-26,540, while Vietcombank listed USD/VND at VND 26,081-26,431.TBTCVN

That is not a new shock, but neither is it soft enough to ignore. In plain terms, as long as the US dollar remains elevated, investors still have a reason to keep part of their money in a cautious stance. That is why I would not jump from “gold is down” to “money will flow into stocks.” If the exchange rate stays tense, short-term capital still has an incentive to preserve some defense instead of fully shifting into risk-taking.

In practice, the three asset classes in this story are sending a fairly consistent message. Gold says the most extreme fear has eased. Stocks say market-wide selling is no longer as aggressive as it was across the previous four weeks. The exchange rate reminds us that the macro tension in the background has not left the stage. Put together, the most reasonable conclusion is not that money has already changed lanes, but that investors are testing how much risk they are willing to absorb again.

Conclusion: less fear is not the same as risk-on

The clearest thesis from this week is simple: defensive money has cooled, but risk-seeking money has not yet returned in a broad enough way. SJC gold falling back below VND 150 million per tael is a real cooling signal. The VN-Index ending a four-week losing streak is also a real stabilization signal. But weak breadth, uneven liquidity, and a still-elevated exchange rate suggest the market has not entered a new wave of broad enthusiasm.

In the near term, the three signals worth watching are market breadth, the quality of liquidity, and the joint behavior of gold and USD/VND. If the index keeps holding up but the number of gainers does not expand, the rebound remains more about the index than about the average portfolio. If gold stays below VND 150 million per tael and the exchange rate does not tighten further, then defensive psychology has more room to ease. Until those pieces confirm each other, the most disciplined reading is still this: the market is less afraid, but it is not yet fully back in a risk-on mode.