When a large fund group shows up repeatedly on the sell side, the emotional impact on new investors is immediate. The instinct is simple: if foreign funds are trimming property stocks, the sector must be turning worse. In practice, though, investors often lose money not because they lack information, but because they stretch a narrow ownership update into a broad industry conclusion.

Put simply, a fund disclosure tells you who sold, how much they sold and how their ownership ratio changed. It does not automatically tell you why they sold, and it certainly does not prove that the entire real-estate segment is entering a fresh downcycle. In Dragon Capital's mid-June transactions, the more disciplined reading is to treat them as the starting point of a review process, not as a ready-made sell button for retail investors.

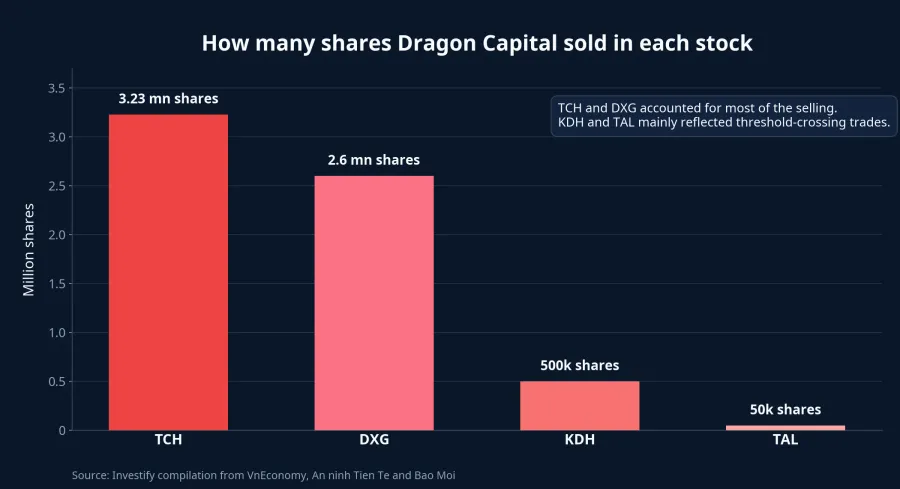

What actually happened

Among the disclosed trades, DXG was one of the bigger ones. On June 12, funds managed by Dragon Capital sold a combined 2.6 million DXG shares, lowering their ownership from 6.08% to just under 5.9% in Bluemarq Group.VnEconomy In KDH, Hanoi Investments Holdings Limited sold 500,000 shares on June 12, pulling the group’s combined stake from 6.0037% to 5.9591%.An ninh Tiền tệ

TAL involved the smallest volume, but it still drew attention because it crossed a threshold investors watch closely. On June 9, Norges Bank sold 50,000 TAL shares, which brought Dragon Capital’s combined stake down from 10.0003% to 9.9904%.An ninh Tiền tệ In TCH, the fund group sold another 3.23 million shares on June 15 and lowered its ownership to 4.7%, which means it no longer qualifies as a major shareholder.Báo Mới

Seen in isolation, those figures explain why many beginners feel uneasy. The same fund family appeared across several real-estate names in a short window, and some of the trades pushed ownership below the 10%, 6% or 5% lines. That naturally creates the impression of a broad retreat. At this point, however, it helps to slow down and separate two different ideas: the absolute size of the trade and the meaning of the ownership threshold.

Ownership thresholds matter, but they are not valuation thresholds

A move from 10.0003% to 9.9904% sounds tiny in economic terms, and in TAL it was. Just 50,000 shares were enough to push the holding below 10%, so the market saw a headline-grabbing disclosure even though the volume itself was not large. KDH had a similar shape: 500,000 shares is worth tracking, but what made the report stand out was the move from just above 6% to just below 6%.An ninh Tiền tệ

The key distinction is straightforward. Ownership thresholds are reporting thresholds, not valuation thresholds. Once a fund crosses lines such as 10%, 6% or 5%, the market pays more attention because the legal or disclosure status of that investor changes. That does not mean the stock’s fair value must immediately reset lower, and it definitely does not prove that Vietnam’s listed property sector has received one uniform negative signal.

DXG and TCH involved larger selling volumes, so they deserve closer attention. Even there, however, the firm conclusion today is still limited: the fund group reduced exposure in several specific stocks. To jump from that fact to “foreign funds are rushing out of real estate” would require much more evidence than the current record provides.

Price action is still telling a mixed story

If this cluster of trades were already a clear bearish signal for the whole group, investors would normally expect three things to show up together: sharp declines across multiple names, visibly heavier sell-side liquidity and a broad deterioration in sector sentiment. The short-term price data here do not show that pattern yet. In the June 19 session, TAL closed at VND 27,300 and rose 0.55%; KDH stood at VND 23,000 and was flat; DXG closed at VND 13,300 and gained 0.38%; TCH slipped 1.32% to VND 14,900.

The 10-session indexed chart points in the same direction. DXG has held up better, TCH has swung around more, while TAL and KDH have been softer without collapsing into a chain-style selloff. When price reactions split that way, the cleaner reading is that the market is still pricing each company separately rather than collapsing them into a single “foreign funds are leaving property stocks” narrative.

That distinction matters a lot for new investors. Many beginners treat fund trades as if they already contain the answer. In reality, the trade itself is only a background signal. Whether the market confirms that signal depends on price action, liquidity and later fundamental data for each company.

Why funds may sell without rejecting the whole sector

Funds do not sell only because they believe a company’s story has deteriorated. They may rebalance after one holding runs ahead of the rest of the portfolio, reduce exposure to move back within internal limits, prepare liquidity for redemptions or shift capital toward a different opportunity with a better risk-reward profile. Those explanations are less dramatic than “the fund saw trouble before everyone else,” but they are often more common in real portfolio management.

That said, it would be just as sloppy to assume every trade here was purely technical. In TCH, fourth-quarter results for fiscal 2025-2026 showed revenue of only VND 394.08 billion, down 54.1% year on year, while net profit fell 63.7% to VND 92.45 billion.Báo Mới That is a meaningful company-specific fundamental signal for TCH, but it still cannot be automatically projected onto DXG, KDH or TAL.

This is where disciplined inference matters. At least three plausible explanations remain on the table: the fund is rebalancing after recent price moves, the fund is managing positions around disclosure thresholds, or the fund has become more cautious on selected company fundamentals. The evidence so far is strong enough to confirm only the first layer, which is that selling happened. The deeper question of why it happened still needs confirmation from market behavior and upcoming business results.

What this means for a beginner’s money

The practical risk is not simply that a fund sold. The real risk is reacting to that fact too broadly. If you see the Dragon Capital name and immediately sell every real-estate stock in your watchlist, you are using a very narrow signal to make a very wide decision. That is where the mistake begins.

Instead of asking, “The fund sold, should I sell now?” a better framework starts with three questions. First, did the trade materially change the ownership status, or was it just an ordinary trimming move? Second, did price action and liquidity confirm broader pressure after the news? Third, do the company’s fundamentals tell the same deteriorating story? Only when all three layers lean in the same direction does the signal begin to carry more weight.

That framework matters even more in real estate because the sector is highly fragmented. A company with projects close to handover, stronger customer prepayments and clearer legal progress is very different from one that still depends heavily on new launches or is carrying a longer capital squeeze. In other words, these stocks may all sit under the “property” label on a quote board, but the investment case behind each one is not the same.

Conclusion: a signal for deeper work, not an automatic sell command

The central thesis is straightforward. Dragon Capital’s transactions are worth tracking as ownership signals, but they are not enough to support the conclusion that the entire listed property group is entering a new weak phase. What the market has confirmed so far is that the fund reduced stakes in several names. What it has not confirmed is that those trades amount to a sector-wide bearish message.

For new investors, the sensible defense is not to mirror every fund disclosure with an instant sale. It is to match the strength of your conclusion to the strength of the evidence. Move from “the fund sold, so the sector is bad” back to “the fund trimmed several positions, so I need to watch price action and fundamentals more closely.” In long-term investing, keeping the right level of conclusion is often just as important as getting the raw information first.