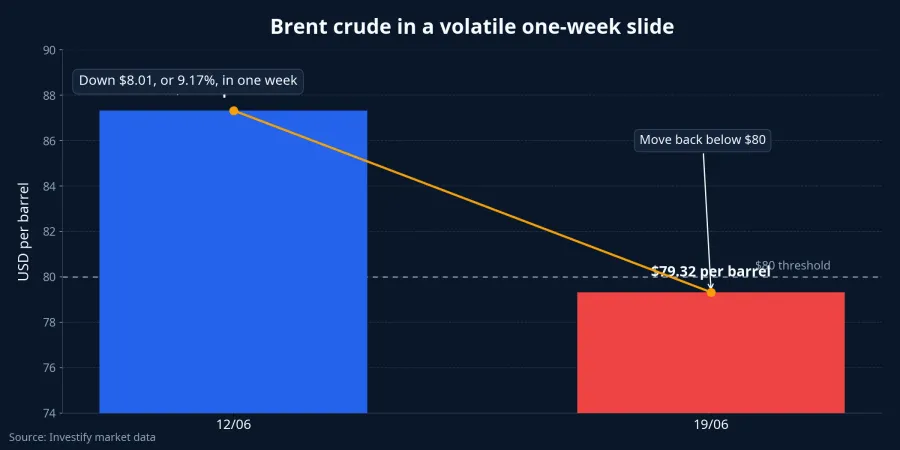

Brent closed at $79.32 a barrel on June 19, down 9.17% from June 12. Taken in isolation, that move invites a simple conclusion: the worst of the energy scare is probably over. The broader setup says something more nuanced. Prices have cooled, but the physical risk around the Strait of Hormuz has not been fully tested yet.

What matters in the new week is not just how far oil has fallen, but whether the decline can hold. On one side, the market is leaning into hopes that shipping through Hormuz will keep normalizing. On the other, Iran is still saying the strait is closed while the U.S. Central Command says commercial traffic is continuing.Guardian As long as those two narratives do not line up, oil remains an open macro trade rather than a settled story.

Why oil still sold off so quickly

The first layer of the explanation is that oil prices react to changes at the margin, not to absolute levels of risk. Once traders started to see a path toward a workable U.S.-Iran channel, some of the supply-risk premium came out of the market. Guardian reported that Brent touched $79.96 a barrel on June 16, its lowest level since early March.Guardian

Anadolu captured the same move on June 16, when Brent slipped to about $79.8 a barrel as the market bet that Gulf oil flows would gradually recover.Anadolu That is not enough to say the risk is gone. It only shows that buyers and sellers are, for now, willing to price a less severe scenario than they were a week earlier.

In other words, this drop in Brent is still a confidence trade. It reflects a belief that supply chains can keep operating, not proof that the system is already back to normal. That distinction matters for newer investors because oil can fall before supply is truly stable, and it can rebound just as quickly if that confidence breaks.

Hormuz still has to be read through real-world data

The Strait of Hormuz is not just another headline. It is a strategic chokepoint, which means the most important question is not which side is making the louder political claim. The better questions are whether tankers are still moving, whether freight costs are spiking, and whether inventories keep draining. Those are the signals that tell you whether the physical market is functioning or tightening again.

The June 20 Guardian report shows the mismatch clearly: Iran says the strait is closed, while U.S. Central Command says commercial traffic is still moving.Guardian That is why investors should avoid reacting to a single Middle East headline in isolation. In this kind of market, oil will stay highly sensitive to any confirmation that comes from actual vessel flows.

There is also a reasoning trap worth avoiding here. Brent falling does not prove Hormuz is fully open again, but there is still not enough evidence to say the market is simply being complacent. Both explanations remain plausible: one, shipping conditions really are improving; two, traders are pre-pricing that outcome before it is fully visible in the data. Next week’s data should do more to separate those two stories.

U.S. inventories are a better reality check than rhetoric

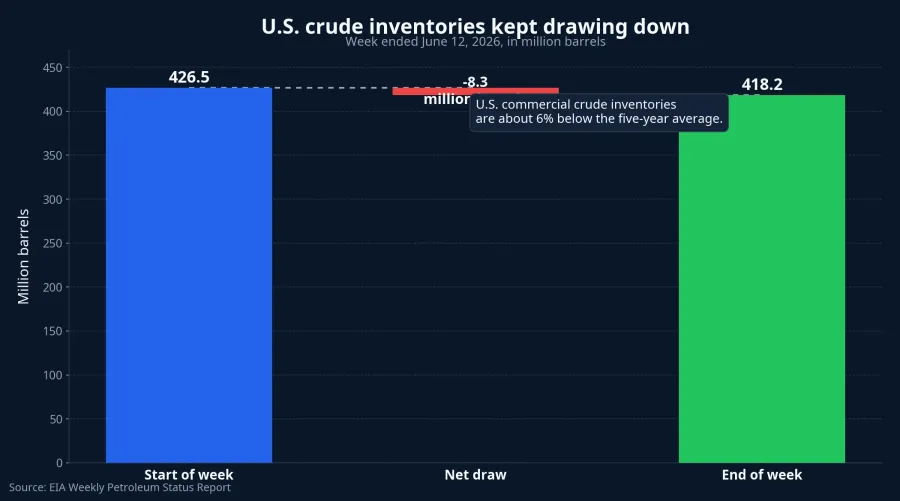

If there is one short-term filter for geopolitical noise, it is U.S. crude inventory data. The Weekly Petroleum Status Report for the week ended June 12 showed U.S. commercial crude inventories falling by 8.3 million barrels to 418.2 million barrels, about 6% below the five-year average for this time of year.EIA A market that is still drawing inventories down that quickly cannot reasonably be described as fully relaxed on supply.

It is not just inventories. U.S. refiners are also running hard. The same EIA report put refinery utilization at 96.7%, while total products supplied over the past four weeks averaged 20.6 million barrels a day, up 3.3% from a year earlier.EIA For investors, that sends a clear message: refined product demand is not weak enough to guarantee another leg lower in crude by itself.

That leaves two fairly clean paths for the coming week. The cooling scenario only becomes more credible if traffic through Hormuz stays stable and U.S. inventory draws begin to narrow. If tanker movement is disrupted in practice or inventories keep falling sharply, sub-$80 Brent is unlikely to hold for long.

The impact on Vietnam will not move in a straight line

For Vietnamese investors, oil matters beyond energy equities. Lower crude prices relieve cost pressure for transport, airlines, plastics, and chemicals, while also easing inflation expectations at the margin. That spillover usually registers more slowly with retail investors than the immediate price action in oil and gas stocks.

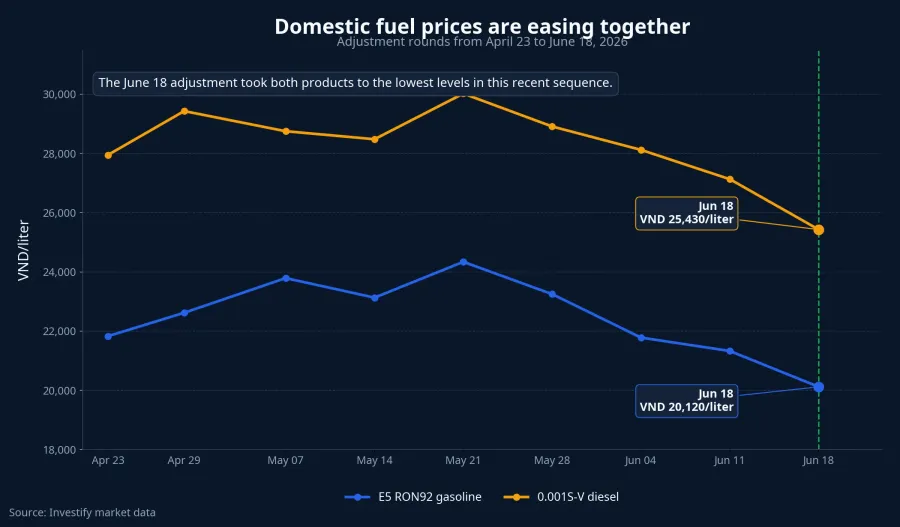

Domestically, E5 RON92 gasoline fell to VND 20,120 per liter on June 18, down 5.67% from the previous adjustment, while 0.001S-V diesel fell to VND 25,430 per liter, down 6.27%. That helps reduce input-cost pressure across several industries, but it is still not enough to declare an inflation reset if Brent turns higher again within the next few sessions.

The stock-market reaction is even less mechanical. BSR closed at VND 26,050 on June 19, down 1.33% on the day; PVS ended at VND 39,000; GAS at VND 81,200. Those prices are a reminder that oil-linked equities do not move one-for-one with Brent because inventories, refining margins, backlog quality, and investor positioning all shape the reaction.

That is the distinction worth keeping in view. A drop in crude can be supportive for fuel-consuming businesses without being uniformly bearish for every oil name. Treating Brent as a single on-off switch for the whole group is too crude a framework for the market now.

What to watch in the new week

The monitoring framework for next week is actually straightforward. The constructive setup would be continued tanker movement through Hormuz, no shock jump in freight rates, and the next U.S. inventory report showing smaller drawdowns. If those pieces line up, Brent has room to stay range-bound or cool further without requiring a dramatic new narrative.

The opposite signal is just as clear. If real-world shipping is disrupted, U.S. inventories keep drawing sharply, or refining margins start to rebound, the risk premium can return quickly. In that case, Brent below $80 would look less like a new equilibrium and more like a pause.

The core thesis for this week is not that oil has become safe again. It is that the market is testing how credible the cooling story really is. The most useful indicators over the next few sessions are tanker flows through Hormuz, the next U.S. crude inventory release, and how Vietnam’s energy-sensitive stocks behave when the commodity signal and the equity signal diverge.