New investors tend to react quickly when a bank announces a share issuance. The instinct is understandable: the share count goes up, EPS may thin out, and the stock price often has to absorb a technical adjustment. But for banks, stopping at the word "dilution" means stopping too early.

The simpler way to think about it is this. A manufacturer that wants to expand can buy more machinery. A bank that wants to lend more needs more equity capital to support a larger pool of risk-weighted assets. So the right question is not whether dilution exists. In most stock-based capital raises, it does. The better question is what that dilution is buying for shareholders over the next few quarters.

This article’s thesis is straightforward: a bank capital raise only deserves a positive reading when return on equity remains productive and provisioning pressure stays contained. If those two indicators weaken, fresh capital may be buying balance-sheet breathing room rather than future earnings power.

Two fresh examples: the same capital story can lead to very different outcomes

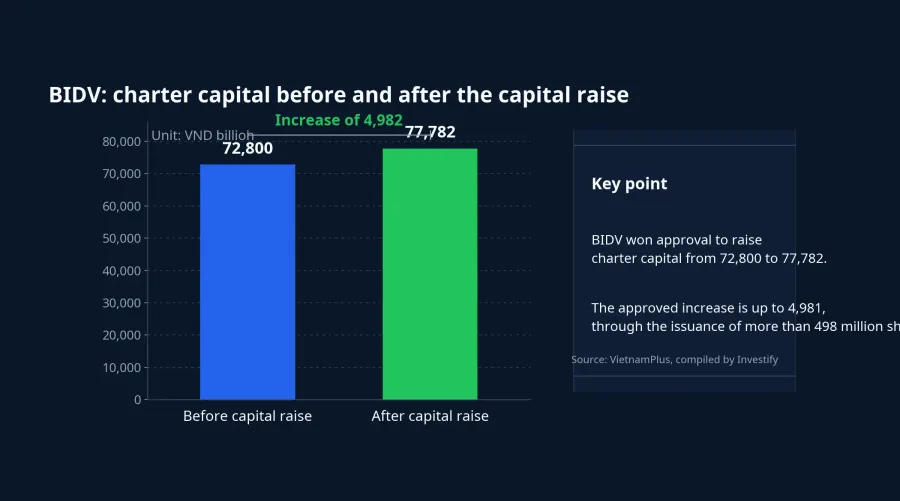

BIDV is the clearest recent case. VietnamPlus reported that the State Bank of Vietnam approved the bank’s charter capital increase from VND 72,800 billion to VND 77,782 billion, with the approved step covering up to VND 4,981 billion through the issuance of more than 498 million shares to existing shareholders, equivalent to a 6.8433% ratio.VietnamPlus On the surface, shareholders immediately see a larger share count. At a deeper level, BIDV is adding capital cushion at a time when lending capacity remains a central issue for Vietnam’s banking system in 2026.

Bac A Bank offers a smaller but similar case. CafeF reported that the bank is about to close the rights date for a 7.5% stock dividend, which would lift charter capital from more than VND 10,721 billion to more than VND 11,525 billion, an increase of more than VND 804 billion.CafeF Mechanically, this is also a conversion of retained earnings into charter capital. It does not create fresh cash on day one, but it does strengthen the capital layer that supports lending growth and safety ratios.

These examples highlight the point many first-time investors miss. An issuance announcement only tells you that capital is going up. It does not tell you where that capital will go or whether it is enough to offset dilution. To answer that, you have to move on to capital efficiency and asset quality.

Why banks need fresh capital in the first place

Banks earn money by combining equity with customer funding to make loans, invest, and provide services. As loan books expand, risk-weighted assets rise with them. If equity capital fails to keep pace, safety ratios come under pressure and the bank’s room to expand credit narrows, even if demand from households and businesses remains healthy.

In plain terms, bank capital works like a building’s foundation. The taller the structure, the stronger the base has to be. A capital raise can therefore signal preparation for a new credit cycle, especially when a bank sees room to grow lending or invest in technology. In that scenario, shareholders accept near-term dilution in exchange for the possibility of stronger future earnings.

But there is another scenario. A bank may raise capital not because it is ready to run faster, but because it needs more room to breathe. If bad loans, provisioning needs, or legacy balance-sheet issues remain heavy, new capital first serves to relieve pressure. That still matters, but it means something very different for shareholders than a raise aimed at expansion.

ROE tells you whether the new capital is actually working

ROE is one of the most useful metrics for retail investors because it answers a practical question: how much profit is each unit of shareholder capital producing? When a bank raises capital, the denominator of ROE expands almost immediately. That means the real issue is not whether ROE slips for a quarter, but whether it stays high enough and stable enough over time.

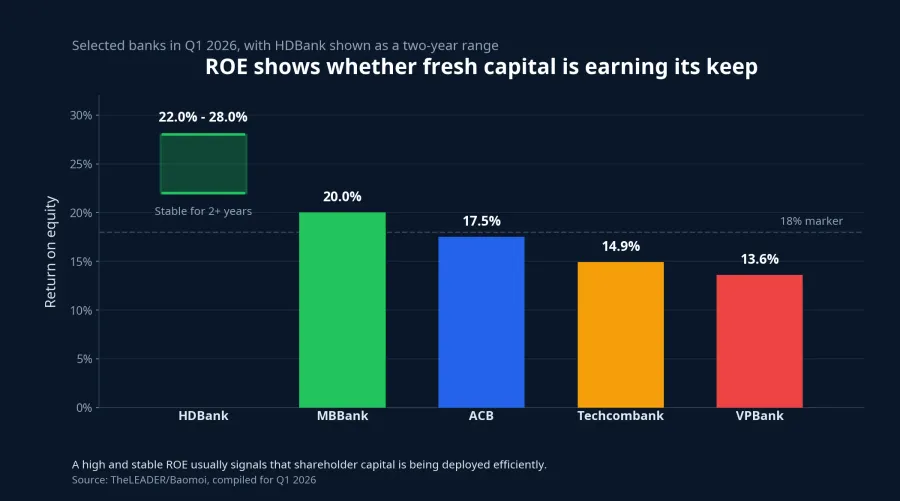

Baomoi’s Q1 2026 data shows a sharply divided picture. ABBank led with a 26.8% ROE, but its result has been volatile across quarters. HDBank, by contrast, has held ROE in a 22% to 28% range for more than two years, while MBBank has stayed around 20%. Among the larger private banks, ACB stood at about 17.5%, Techcombank at about 14.9%, and VPBank at about 13.6%.Baomoi

The key point is not which bank tops the table in one quarter. The key point is which bank can sustain a strong ROE over a long enough period. A high ROE that swings wildly may reflect one-off items. A lower ROE that keeps drifting down after a capital raise may indicate that fresh equity has not yet been turned into sufficiently productive earnings.

From a shareholder perspective, ROE helps separate two stories that can look similar at first glance. A bank that raises capital and still preserves healthy ROE is showing that the new equity base is participating in profit creation. A bank that raises capital but then posts a prolonged ROE slide deserves a more careful reading.

Provisioning reveals whether capital is funding growth or defense

If ROE answers the efficiency question, provisioning answers the quality question. In banking, provisioning is the share of earnings that has to be set aside to cover credit risk. When that number grows too large, the portion that truly becomes shareholder value is much thinner.

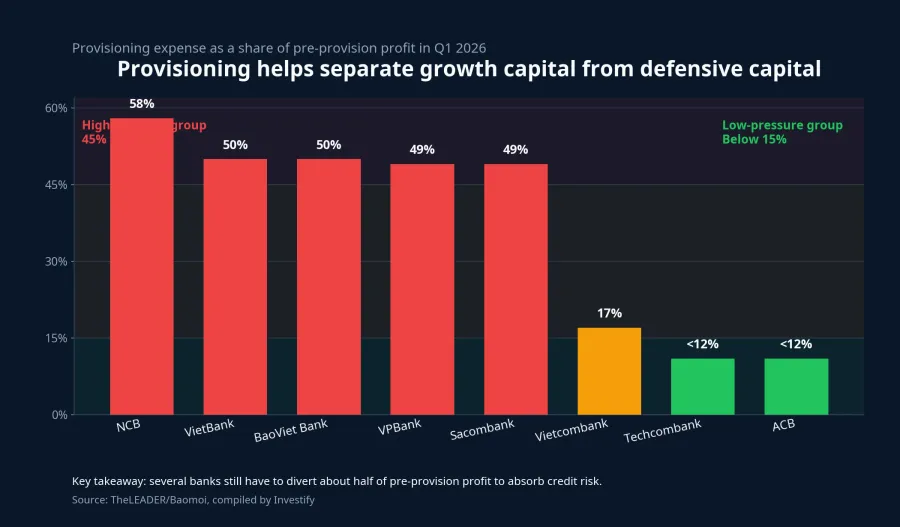

Baomoi’s June 9 data shows that NCB had to devote nearly 58% of pre-provision profit to provisioning expense in Q1 2026. VietBank and BaoViet Bank were both near 50%, while VPBank and Sacombank were also around 49%. On the other side, Vietcombank was only about 17%, while Techcombank and ACB were below 12%.Baomoi

That is why a capital raise cannot be judged by issuance size alone. A bank that raises capital while keeping provisioning pressure low has a better chance of turning the new buffer into cleaner earnings growth. By contrast, if provisioning still consumes about half of operating profit, fresh capital may be acting more like a balance-sheet shock absorber.

This also helps avoid a common mistake. A smaller issuance is not automatically safer, and a bigger issuance is not automatically worse. What investors should compare is the quality of each unit of capital after the issuance.

How new investors can read a bank capital season

Instead of reacting immediately to dilution, new investors can work through a short checklist. Where is the capital coming from: retained earnings, a stock dividend, a rights issue for existing shareholders, or a private placement? Does the bank clearly explain what the capital will be used for? Does ROE have a path to staying stable after the raise? And is provisioning pressure low, moderate, or high?

That is the most useful framework because this is really a test of growth quality. Strong banks raise capital to go further. Pressured banks raise capital to stay on their feet. Those two announcements can look almost identical on a headline, but they mean very different things once you move into ROE and provisioning.

Conclusion: dilution is only the arithmetic

For bank stocks, fear of dilution is a reasonable starting instinct, but it is not a conclusion. The more important issue is whether the bank can convert new capital into new profit. If ROE remains healthy and provisioning stays under control, a capital raise can be read as preparation for a broader credit cycle. If ROE weakens while provisioning continues to eat into earnings, the new capital is mostly buying resilience.

So this should not be reduced to a simple good-or-bad call after one issuance notice. For new investors, the signals worth tracking over the next few quarters are concrete: whether ROE recovers or stabilizes, whether provisioning pressure cools, and whether the thicker capital base actually starts generating more profit for shareholders.