The legal door is already open. A new draft decree is also trying to connect PPP project companies with the public capital market. Yet in practice, PPP bonds still have not become a core funding channel for infrastructure in Vietnam. The real bottleneck sits elsewhere: the market still does not see a cash-flow structure clear enough to turn a long-life project into a bond investors can confidently price.

That is the point raised by Vuong Hoang Son, Director of the Investment Banking Division at VNDIRECT Securities Corporation, in a June 10 interview with Thoi bao Tai chinh Viet Nam. Son argued that most PPP project companies are newly established, lack a financial track record and generate no operating cash flow during construction, while bond investors still need credible protection around capital recovery.TBTCTVN

Put simply, PPP bonds are not difficult because the label is unfamiliar. They are difficult because investors cannot look at the coupon and stop there.

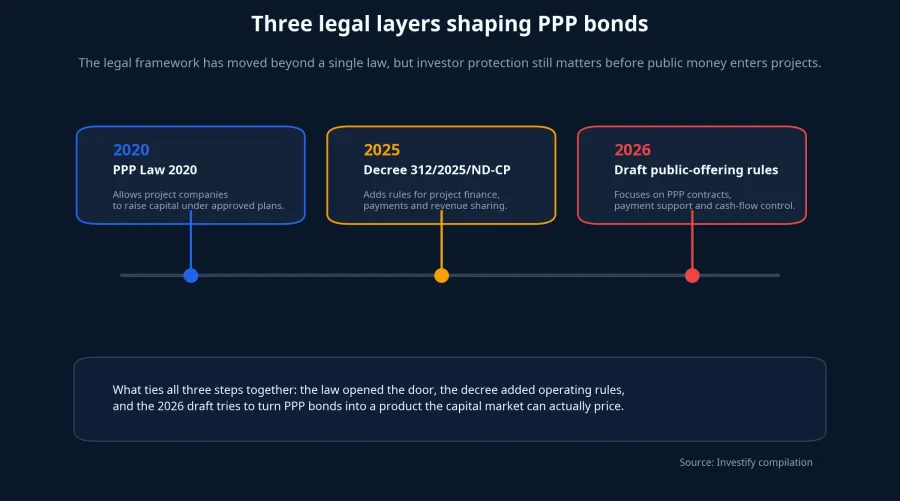

The law opened the door, but that was only the starting point

Vietnam's PPP Law 2020 allows project companies to raise capital under approved financing plans. That matters because it formally recognizes that PPP infrastructure projects can look beyond bank lending for long-term funding.Chinh phu

For retail investors, however, “allowed to raise capital” can create the wrong impression. Many people hear the word bond and immediately think of a fixed-income loan: interest arrives on schedule, principal comes back at maturity, end of story. That surface-level logic breaks down when the bond is tied to an infrastructure asset that is still being built or has only recently begun operating.

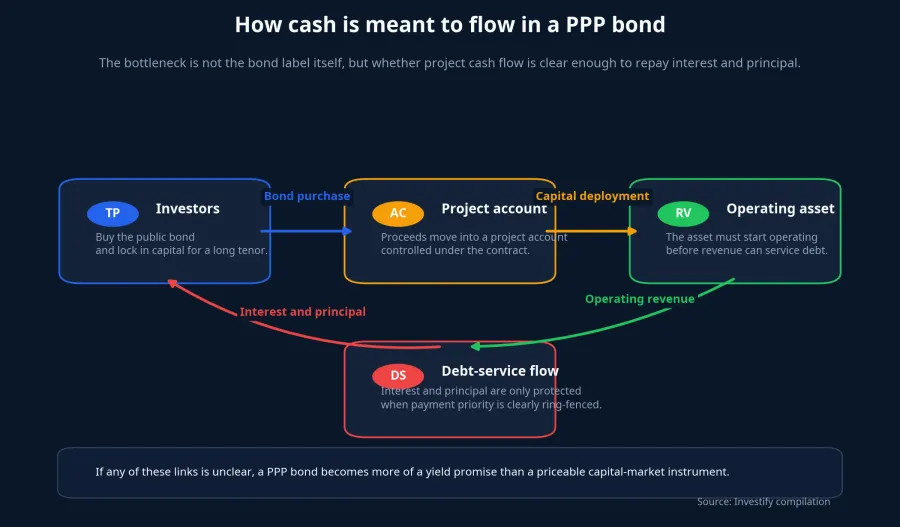

A regular company may offer years of financial statements, several revenue streams and an established repayment history. A PPP project company is different. It is usually created for one contract, built around one asset and ultimately expected to repay debt from one highly specific stream of cash flow. If that stream has not started yet, or if it exists but is not clearly protected through contracts and monitoring rules, it is hard to attract patient capital.

That is why “is issuance legally allowed” has never been a sufficient question. The real questions are these: if the project is not yet collecting fees, where will interest payments come from; if traffic or usage falls short of plan, who absorbs the gap; and if a dispute emerges, where do bondholders stand in the payment waterfall.

The legal framework is deeper now, but investor protection remains the center of gravity

After the PPP Law 2020, the framework moved one step further with Decree 312/2025/ND-CP. The decree adds rules on PPP project finance, payments, settlement and revenue-sharing between participating parties.Thu Vien Phap Luat

What matters here is that the state is not treating PPP bonds as a stand-alone financial product. The bond sits inside the full financing architecture of the project. That means leverage, tenor, project accounts, debt-service allocation and risk-sharing all have to fit together.

In May 2026, the Government portal published a draft decree on public bond offerings by PPP project companies. The shift in emphasis is important. Instead of focusing on minimum operating history or accumulated profits as it would for a regular corporate issuer, the draft leans on signed PPP contracts, borrowing limits, payment support, credit ratings and cash-flow management.Bao Chinh phu

In plain English, the market is moving away from “how old is this issuer” and toward “how trustworthy is this project contract.” For PPP bonds, the age of the legal entity matters less than the quality of the contract, the control over cash flow and the certainty of repayment support.

If the draft is eventually issued, its biggest impact will not be to launch a flashy new instrument. Its bigger contribution would be forcing more transparency into the issuance structure itself. That is what the capital market actually needs.

Why PPP bonds cannot be read like ordinary corporate bonds

A traditional corporate bond is usually read from the top down. Investors start with the issuer's financial health, leverage, repayment history, assets and reputation. PPP bonds have to be read from the bottom up. Buyers need to examine the project asset, the PPP contract, the account receiving proceeds and the order of payment before they circle back to the issuing entity.

Another way to think about it is this: lending to an established operating company is not the same as backing a cash-flow machine that is still being assembled. If that machine has not started, or has started but still lacks a tightly ring-fenced contractual structure, a higher yield may not compensate for the extra risk.

That distinction is especially important for newer investors. Infrastructure bonds sound safe because they are tied to roads, bridges, ports or water plants, all of which are tangible assets. But tangible assets do not automatically translate into safe debt service. What matters is whether cash generated by that asset is routed into the right account, whether it can be diverted to other obligations first and whether bondholders have effective monitoring rights.

That is why the PPP bond problem cannot be solved by headline yield alone. An attractive coupon says very little about capital protection if the contract structure remains loose.

International precedents show that markets need a credit-enhancement layer

In more mature PPP markets, the missing piece is often filled by credit enhancement or a specialized project-screening institution. Indonesia offers a useful example. According to the World Bank, the Indonesia Infrastructure Guarantee Fund is a state-owned company fully owned by the Indonesian government, established in December 2009 to evaluate, structure and provide guarantees for infrastructure PPP projects.World Bank

The lesson is not that the state should absorb every risk on behalf of investors. The deeper lesson is that the market benefits from a standardized gatekeeper that separates stronger projects from weaker ones. Once underwriting standards are standardized, investors do not have to navigate every legal complexity alone.

South Korea took a similar route with a credit backstop. KODIT says the Infrastructure Credit Guarantee Fund was established in August 1994 to attract private investment into infrastructure construction and operation. It also lists a maximum guarantee limit of KRW 500 billion per project, with guarantee fees ranging from 0.1% to 1.5% a year depending on the credit rating.KODIT

Those figures matter because they show that guarantees are not free gifts. They are a way to price risk. The more credible the project, the more manageable the support cost. The weaker the project, the more expensive the support becomes or the less likely it is to be granted. That is the kind of mechanism that allows the market to function through pricing rather than promises.

What will determine whether PPP bonds can scale

The core thesis is straightforward: PPP bonds are still small not because the law has failed to open the door, but because the market still lacks confidence in the underlying cash flow and in the protective layers wrapped around investors. In other words, the constraint has shifted from “is there a legal basis” to “is the framework detailed enough for public-market money to participate.”

In the near term, three signals matter most: the final wording of the decree if it is issued, the payment-support structure attached to public PPP bond offerings and the clarity of project-account controls plus the monitoring rights of bondholder representatives. If those three links remain vague, the market will struggle to treat PPP bonds as a major channel no matter how compelling the infrastructure funding story sounds.

For beginner investors, the practical takeaway is to stop reading infrastructure bonds as yield invitations. Read them as cash-flow blueprints. Only when that blueprint is clear enough can PPP bonds become a real bridge between long-term infrastructure needs and private savings. If the protective layers remain thin, the market will likely stay stuck in promise mode rather than scale mode.