When more than 70% of listed stocks trade below 10x P/E, the first instinct is obvious: the market must be cheap. For newer investors, that reaction is perfectly rational. A low P/E usually feels like buying a stream of profits at a discount.CafeF

The problem is that P/E only answers part of the question. It tells you how much investors are paying for current or forward earnings. It does not tell you whether those earnings are durable, whether the benchmark index has been distorted by a handful of giant stocks, or whether institutional money is ready to re-rate the market higher.

What A Low P/E Says, And What It Does Not

In its June 2 report, VinaCapital said the VN-Index was trading at roughly 13x forward earnings while 2026 profit growth was expected at about 15%. On the surface, that looks compelling: valuations are not stretched and earnings are still projected to grow.VinaCapital

The more striking statistic sits beneath the headline index. VinaCapital and CafeF both point to a market where more than 70% of stocks trade below 10x P/E. That is a large share of listings sitting in what most investors would call a low-valuation zone.VinaCapitalCafeF

That still does not mean every low-P/E stock is genuinely cheap. Sometimes a stock trades at a low multiple because the market has overlooked a solid business. Sometimes it trades there because investors are discounting weak cash flow, leverage, unstable margins, or an industry outlook that is getting worse. The same 10x P/E can describe two very different risk profiles.

This is why the statement "many stocks are cheap" is not the same as "the whole market is cheap." A stock picker may find plenty of names in a depressed valuation bucket. An index buyer, by contrast, is buying a basket whose weights are far from evenly distributed.

When The Index Stops Representing The Median Stock

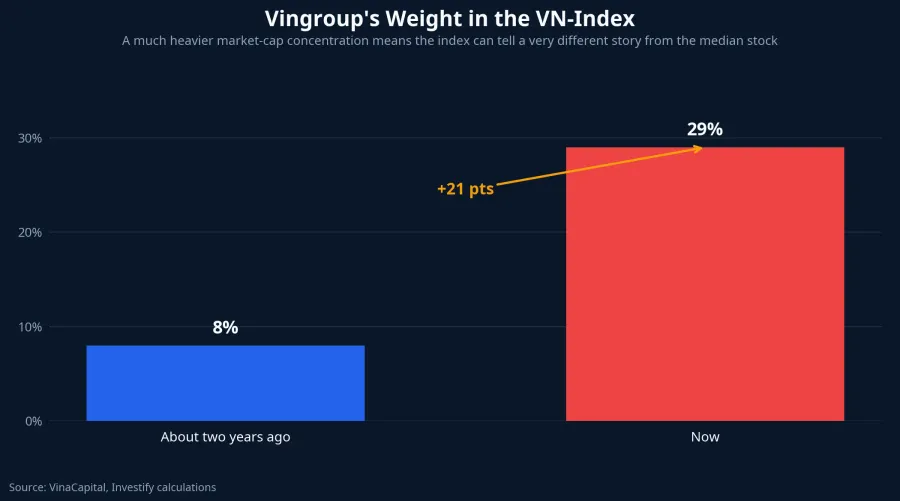

One of the report's most important details is concentration. The Vingroup complex, including VIC, VHM, VRE and VPL, now accounts for almost 30% of the VN-Index's market capitalization, up from about 8% two years ago.VinaCapital

That changes how the index should be read. Once a single corporate ecosystem becomes this large, the benchmark starts telling a different story from the average listed company. Investors can see the VN-Index holding up or climbing while large parts of their own portfolio lag behind, simply because the rest of the market is not moving in lockstep with the dominant weights.

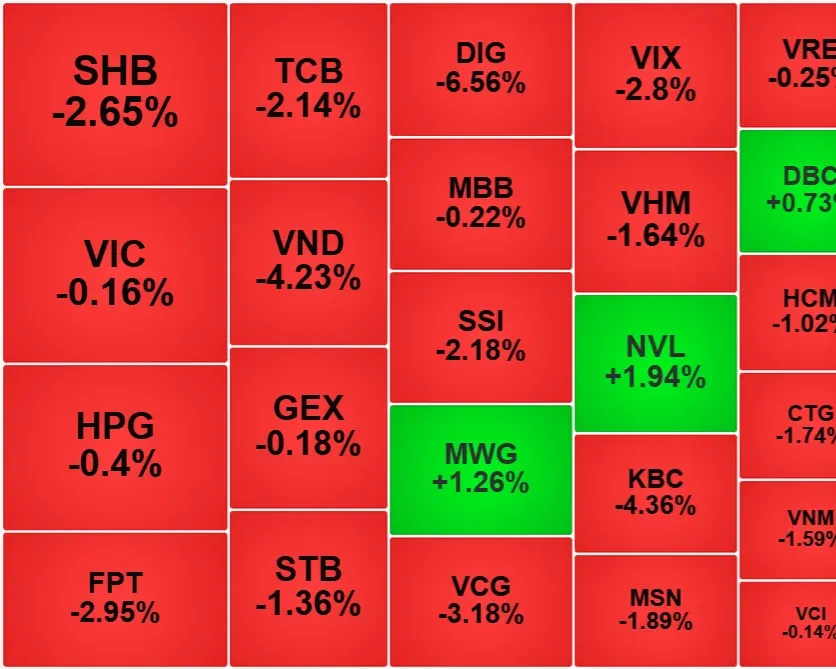

VinaCapital said the VN-Index gained about 41% last year, but only around 10% if Vingroup-related stocks were excluded. This year, the headline index has still been outperforming the ex-Vingroup version by roughly 4-5 percentage points.CafeFVinaCapital In the latest session, the VN-Index closed at 1,838.90 points, up 0.40%.

For beginners, this is one of the easiest traps to miss. An index trading at 13x forward earnings does not mean each of its components tells the same valuation story. As market-cap concentration rises, the benchmark can look healthier or more expensive than the broader field of stocks underneath it. That is why any claim that "the market is cheap" has to be split into two separate claims: what the index looks like, and what the typical stock looks like.

Strong Earnings Still Need A Quality Check

There is a real positive underneath the market. VinaCapital said VN-Index earnings rose 51% year over year in the first quarter of 2026, far above the roughly 15% consensus expectation. Even after excluding VHM, earnings growth still came in at about 30%.VinaCapital

That matters because it tells us the market is not sitting on a completely hollow earnings base. The rebound was genuine. Growth excluding VHM was still strong enough to reject the idea that the whole market is living off a single price-led surge in a few names.

But the same report also highlights why headline growth should not be read lazily. VHM alone posted profit growth of 850% in the first quarter, and VinaCapital noted that real-estate earnings can swing sharply depending on revenue recognition timing.VinaCapital

In practice, that means the denominator in the P/E ratio is not fixed. If one quarter's earnings are boosted by project handovers, accounting timing, or one very large contributor, the current multiple can look cheaper than the underlying durability of earnings across the rest of the market. A low P/E becomes more trustworthy only when it sits alongside recurring operating profits, healthy cash flow, and a pattern that survives across several quarters.

Why Cheap Valuations Have Not Pulled Money Back In

If you only looked at valuation and first-quarter earnings, you might expect money to return more aggressively. Yet VinaCapital describes a market facing several simultaneous pressures: disruption around the Strait of Hormuz, Vietnam's trade deficit widening from about 3% of GDP before the conflict to above 6% of GDP by mid-May, inflation running above 5%, and foreign investors net selling roughly USD 2 billion so far this year after around USD 5 billion of net selling in 2025.VinaCapital

That should not be reduced to a single neat causal story. It is not accurate to say the market stays cheap only because of Hormuz, or only because of foreign selling. The more defensible reading is that several headwinds are acting at once: inflation can keep funding costs elevated, trade and currency pressures can make investors more cautious, and persistent foreign outflows can weigh on the largest stocks. The evidence is strong enough to explain why the market has not been re-rated yet, but not strong enough to assign exact weights to each driver.

That is the real distinction between "cheap" and "ready to rise." An asset can look inexpensive versus history and still remain stuck there if the cost of capital has not eased, institutional flows have not turned, and future earnings have not confirmed the first-quarter strength.

A Simpler Framework For New Investors

For first-time investors, the safer way to use P/E is as an entry filter. Start by using it to screen for businesses or sectors the market is pricing cheaply. Then check whether the earnings come from core operations or one-off factors. After that, look at debt, cash flow, margins, and the industry's position before concluding that the market has truly mispriced the company.

The final step is to place each stock back into the broader market context. If the benchmark is increasingly dominated by a small cluster of mega-caps, you cannot use the VN-Index alone to describe the opportunity set. If foreign investors are still selling and the rate backdrop remains uncertain, you should not assume every low-P/E stock will be re-rated at the same time.

The cleanest conclusion is also the most useful one: a low P/E is a good starting point, but it is not enough to call the whole market cheap. The current evidence supports a narrower claim instead. Vietnam's market contains many low-valued stocks, but the real opportunity lies in separating stocks that are neglected from stocks that are cheap because the market is already pricing in genuine risk. The next signals worth tracking are earnings quality over the coming quarters, the pace of foreign outflows, and whether inflation proves sticky.VinaCapital