Vietnam Electricity has crossed a line that looked distant only a few years ago. Its audited 2025 consolidated statements show that the group has moved out of accumulated losses and into positive retained earnings of VND 5.533 trillion.VTC News For investors, especially newer ones, that is more than a cleaner accounting headline. It signals that the power-sector debate is moving away from repairing old damage and toward a harder question: how to prevent a new loss cycle from forming.

As long as EVN was still carrying accumulated losses, every discussion around electricity prices naturally revolved around the legacy gap. Once those losses have been absorbed at the consolidated level, the market has to ask something else: is the current tariff framework flexible enough to reflect fuel costs, hydrology and demand pressure in time?

EVN's financial position has clearly changed

The first thing worth noting is the quality of the turnaround. In 2025, EVN reported net revenue of VND 645.658 trillion, up by more than VND 65 trillion from a year earlier, while after-tax profit reached VND 51.881 trillion, 5.3 times the 2024 level.VTC News This was not a marginal improvement designed to make the statements look better. It was large enough to flip retained earnings from negative to positive.

The change also shows up on the balance sheet. By the end of 2025, EVN's total assets had risen to more than VND 783 trillion, up 16% from the start of the year. Cash and cash equivalents stood at VND 20.055 trillion, while term deposits at banks climbed to VND 132.388 trillion.VTC News That matters because it suggests EVN is not only out of the accumulated-loss zone on paper. It has also rebuilt a more visible liquidity buffer.

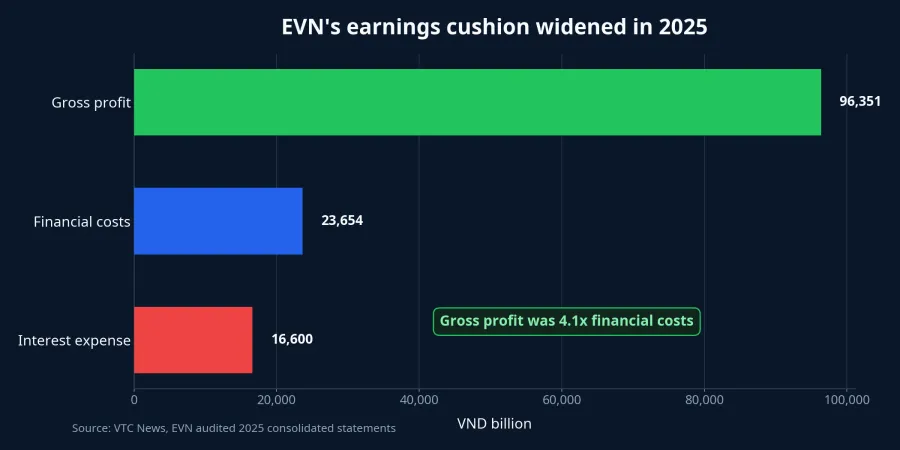

Where the turnaround came from

There was no single miracle behind the reversal. Two moving parts improved at the same time. The first was gross profit. In 2025, EVN's cost of goods sold came in at VND 549.071 trillion, leaving gross profit at VND 96.351 trillion, nearly double the VND 49.588 trillion recorded in 2024.VTC News

For less experienced readers, gross profit is the first cushion between the selling price and the core operating cost of supplying electricity. When that cushion gets thicker, the company has more room to absorb interest expense, foreign-exchange swings and other financial charges. In EVN's case, that is the most important part of the story because it suggests the improvement was not just about cost control. It was also about selling power under a more favorable price backdrop than before.

The second moving part was that financial costs, while still heavy, no longer swallowed the operating gain. EVN booked VND 23.654 trillion of financial costs in 2025, including more than VND 16.6 trillion in interest expense.VTC News In other words, the capital burden remained substantial, but gross profit was finally large enough to clear that layer instead of being buried under it.

That is the detail investors can miss if they stop at the bottom-line number. Large infrastructure groups rarely move from distress to stability because of one isolated decision. The real signal lies in the structure underneath: once gross profit grows faster than financing pressure, the balance sheet starts to change character.

Clearing losses does not mean pricing pressure is gone

This is where the story becomes more interesting. It would be too simplistic to conclude that because EVN is healthier, electricity-price pressure should now fade. A better reading is that the issue has changed phase: from handling legacy losses to testing whether the current tariff mechanism can keep pace with new cost swings.

Vietnam's average retail electricity tariff is currently around VND 2,204.07 per kWh, the pricing basis that has remained in force for 2026 after the adjustment applied from May 10, 2025.VTC News That level matters because it anchors both household utility bills and the cost base of power-intensive listed companies. If tariffs lag input costs for long enough, pressure can build back up inside EVN. If tariffs move too quickly, the burden shows up more directly in CPI and in the margins of electricity-heavy industries.

The broader policy backdrop also points to a more market-oriented and more transparent system. On June 5, the Ministry of Industry and Trade issued Circular 29/2026/TT-BCT, setting detailed rules for the competitive wholesale electricity market, including price determination, settlement and operational data disclosure.Báo Chính phủ That does not mean electricity prices will suddenly become fully market-driven. It does mean that the next stage of the EVN story is about transparent cost recognition and payment mechanics, not merely the cleanup of old losses.

The biggest variables are still fuel costs and weather

Power-sector input costs rarely move in a straight line. Internal data show coal at USD 147.55 per ton on June 4, 2026, well above the USD 105.00 per ton level seen on June 5, 2025. Natural gas, by contrast, stood at USD 3.29 per MMBtu on June 5, 2026, below USD 3.78 per MMBtu a year earlier. These are not direct contract prices for EVN in Vietnam, but they are useful signals that global energy costs are diverging rather than cooling in a uniform way.

Weather is the second variable that outsiders tend to underestimate. Báo Chính phủ reported that at the June 3 government meeting, electricity demand in May had run hotter than expected because the heat wave arrived early, especially in northern Vietnam.Báo Chính phủ When load rises quickly while hydrological conditions are less favorable, the system may have to call on more high-cost generation. That is exactly when the financial cushion rebuilt in 2025 starts to face a real test.

This is also why investors should not treat the power sector as one homogeneous trade. Hydropower companies are usually more sensitive to water conditions and dispatch volume. Thermal power producers react more sharply to fuel prices and power purchase agreements. Grid, equipment and construction-related names care more about whether EVN can keep investment spending on a steadier track now that its balance sheet is less strained.

What investors should watch next

The central thesis is straightforward. EVN's move out of accumulated losses does not end the electricity-pricing debate. It changes the core question: can Vietnam's pricing and market framework absorb new cost pressure quickly enough to avoid recreating another round of losses?

Three signals matter most over the next few quarters. The first is the gap between the average retail tariff and cost pressure from coal, gas and the dispatch mix. The second is the pace of market-rule adjustments, because better transparency on data and settlement should improve how both companies and investors price risk. The third is whether EVN can preserve its liquidity cushion and gross-profit buffer if summer demand remains elevated.

If those three lines move in the same direction, 2025 could mark the start of a more stable phase for EVN and for businesses tied to the power value chain. If they fall out of sync, especially if fuel costs rise again while tariffs react slowly, then EVN's strong 2025 result will look less like a final resolution and more like an important recovery inside a system that is still being tested.