An ESOP equal to roughly 1% of outstanding shares does not sound alarming on first read. For many newer investors, the default reaction is to file it under employee retention, management incentives, and something broadly neutral for outside shareholders. Masan's latest plan shows why that instinct only tells half the story.

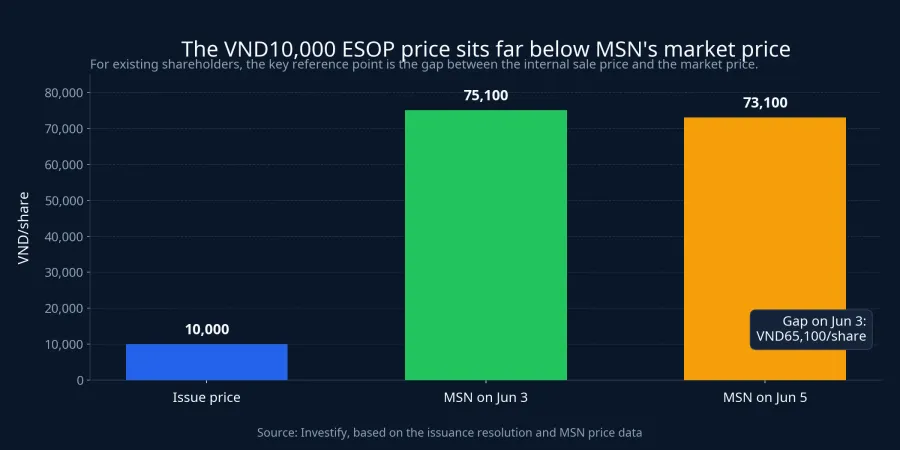

Under a plan approved after its June 1 board resolution, Masan Group plans to issue 14,459,154 shares under its employee stock ownership program, equal to about 1% of its outstanding common shares, at VND10,000 per share.Vietnambiz MSN closed at VND75,100 on June 3 and VND73,100 on June 5. In plain terms, investors should not stop at the number of shares being issued. They also need to look at the very wide gap between the internal sale price and the price the market is already paying.

Small on paper, not small in meaning

If you divide the new shares by the total share count after issuance, the dilution comes to roughly 0.99%. That is not a control shock. A shareholder who owned 1% before the deal would theoretically own about 0.99% after it, assuming no additional purchases. For a company of Masan's scale, that level of dilution alone is not enough to redraw the ownership map or overturn the valuation overnight.

The problem is that 0.99% can lull readers into underestimating the issue because it looks tiny as a ratio. What matters more is the quality of that dilution. A share issuance priced close to the market and one priced at VND10,000 create very different economic outcomes even if the headline dilution rate looks similar.

That is the part many first-time investors miss. Dilution is not only about quantity. It is also about the price of the new shares, who gets them, what conditions apply, and what long-term benefit existing shareholders are supposed to receive in return. If you stop at “it is only 1%,” you miss the more important half of the analysis.

The real transfer sits in the pricing gap

Using the June 3 closing price as the reference point, the gap between the market price of VND75,100 and the ESOP price of VND10,000 is VND65,100 per share. Multiplied by 14,459,154 shares, the theoretical value transfer comes to about VND941.3 billion. Using the June 5 close of VND73,100, the figure still works out to roughly VND912.4 billion.

That does not mean Masan is writing an immediate cash check of nearly VND1 trillion to employees. The correct way to read it is that the company is selling an asset the market values at around VND73,000 to VND75,000 for VND10,000. The right to buy at that discount has real economic value. That value does not disappear. It moves from existing shareholders to the people who receive the allocation.

In everyday terms, it is like a retailer selling a product internally at a steep discount while customers outside are willing to pay much more at the counter. The company still collects cash, but it has deliberately chosen not to collect the full value the market was ready to pay. For shareholders, that uncollected value is exactly what needs to be justified.

That is why dilution alone is not enough. The full reading frame needs one more question: how deep is the discount, and how large is the economic value being transferred. Masan's case is not simply “share issuance is bad.” It is “share issuance at a very low internal price deserves much closer scrutiny.”

When an ESOP makes sense

To be fair, an ESOP is not inherently negative. A company may need stock-based compensation to retain managers, align employees with long-term goals, and make operators think more like owners. In many growth companies, this is a familiar tool and can be entirely reasonable if it is designed well.

The issue is what “designed well” actually means. For shareholders, four layers matter. The first is the lock-up. In this case, the ESOP shares are subject to a one-year transfer restriction.Vietnambiz That does reduce one obvious risk because recipients cannot buy and immediately sell to crystallize the discount.

The second is the breadth of the allocation. According to the disclosure, 286 employees are included in the program, so the plan is not confined to an ultra-narrow group at the top of the pyramid.Vietnambiz For newer investors, that matters because it suggests the ESOP may be organizational in scope rather than purely personal.

The third is the stated use of proceeds. The company expects to raise nearly VND145 billion from the issuance, and the disclosed uses include salaries, supplier payments, loan repayments, and principal and interest obligations on bonds.Vietnambiz That is useful disclosure, but it still does not answer the central shareholder question. The core issue is not how much cash the company raises. It is how much value it gives up to raise that amount.

The fourth, and most important, layer is performance linkage. A one-year lock-up limits near-term selling pressure, but it does not tell investors what revenue, profit, cash flow, or operating targets recipients must hit. Without a clear performance structure, an ESOP can start to look less like pay-for-results and more like a broad transfer of benefits.

What retail investors should read carefully

Masan's case offers a very direct example. Danny Le, CEO of Masan Group Corporation (MSN), is entitled to buy 350,000 shares under the program.Vietnambiz At VND10,000 per share, that requires VND3.5 billion in cash. Against the June 3 closing price, the theoretical value gap on that allocation alone is about VND22.8 billion.

That detail should not be read as a personal attack. Its value is analytical. It shows investors that an ESOP is a decision about allocating economic benefits, not just a human resources headline. When the implied transfer reaches tens of billions of dong for one executive and hundreds of billions for the full program, the story has moved well beyond a routine employee reward.

So the right reading order for a retail investor is straightforward. First, identify the issuance ratio to understand the mechanical dilution. Next, compare the issue price with the market price to measure the depth of the discount. Then estimate the transfer of value by multiplying the price gap by the number of shares. Only after that should you turn to lock-up terms, recipient lists, and performance conditions.

That framework matters because it helps investors avoid two bad extremes. One is reacting to every ESOP as if it were automatically abusive to shareholders. The other is treating every ESOP as a modern governance tool that does not need much scrutiny. Both responses are too lazy for the numbers in front of you.

The thesis that matters here

The point is not that Masan must be wrong because it is issuing ESOP shares. At around 0.99% post-issuance dilution, this is not a major ownership event if you look only at the headline ratio. But because the issue price sits so far below the market price, the plan is also a large transfer of value that existing shareholders are entitled to question, especially on performance conditions and long-term payback.

Put more simply, the issue is not the ESOP label itself. It is the price attached to that label. If Masan can show that the value given up today buys a more committed workforce, stronger execution, and better business performance over the next few years, shareholders may judge the trade-off reasonable. If not, the VND10,000 price tag will keep looking like an internal privilege financed partly by outside owners.

The next signal worth watching is not whether MSN rises or falls over the next session or two. The more important signal is whether the company discloses clearer performance criteria, allocation logic, and pricing rationale for the program. For newer investors, that is the real skill to build: looking past a small dilution percentage and seeing the economic value that is actually moving underneath it.