Iron ore is cheaper than it was a month ago. For steel stocks, though, the key question is not how much the input cost has fallen. It is whether selling prices can hold. Investors who stop at "raw materials are down, so steel must benefit" usually miss the part of the chain that matters most: revenue per ton.

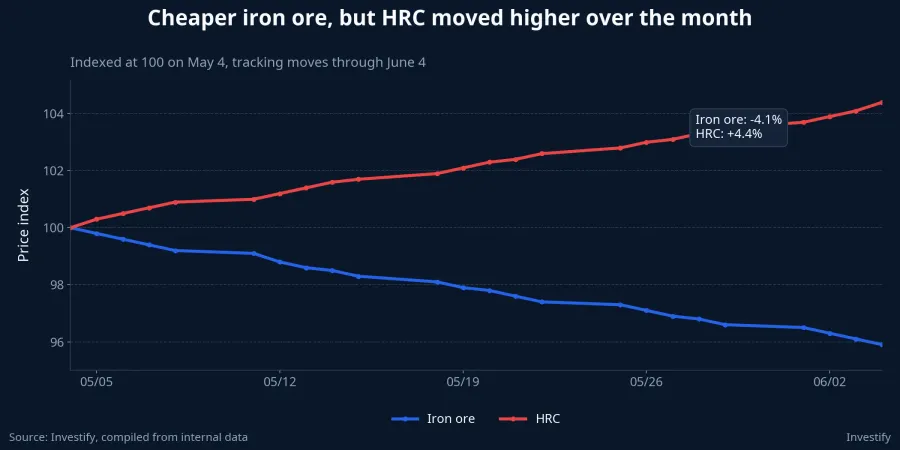

As of June 4, internal market data put iron ore at USD 103.71 per ton, down about 4.1% from May 4. Over the same stretch, hot-rolled coil, or HRC, stood at USD 1,189.07 per ton, up about 4.4%. Put side by side, those numbers make one point immediately clear: input costs and output prices do not move in lockstep.

The mechanism is straightforward. A steelmaker does not buy ore today and turn it into realized profit tomorrow. Between those two points sit raw-material inventories, production cycles, sales contracts, freight costs and end demand. Cheaper ore can help, but only as a starting condition. It is not proof that earnings are about to improve.

Selling prices matter more than the raw-material headline

If iron ore falls while steel selling prices hold, the spread can widen and margins can improve. If iron ore falls because steel demand is weakening, the story changes. A producer may buy inputs more cheaply, but it may also face softer selling conditions at exactly the same time. In that setup, the benefit on the cost side can disappear quickly.

That is why HRC deserves more attention than the simple "ore down is good" narrative. HRC is closer to the revenue line for flat-steel products and is also a direct input for coated sheet producers. When HRC stays firm or rises while iron ore declines, the market has a real basis for talking about margin support. When HRC rolls over alongside ore, the message is different: weaker demand may be filtering down to the selling side.

The past month leans more toward the first scenario: cheaper ore and firmer HRC. Even so, one month of data is not enough to turn that into a fully formed equity thesis. For that case to hold, investors still need to see the spread persist long enough to show up in actual earnings rather than just in commodity screens.

The same news does not land the same way across the sector

Not every listed steel company has the same sensitivity to iron ore. HPG runs a more integrated production chain, so ore moves feed into its cost base more directly. But even for HPG, that advantage only matters if domestic construction-steel prices and local HRC pricing do not get dragged lower by competition or weaker demand.

HSG and NKG sit closer to HRC because it is the relevant input for coated steel. In practical terms, investors tracking HSG or NKG and looking only at iron ore are still standing too far from the point where profitability is decided. For those names, HRC, export orders and selling-price discipline often tell a clearer story than ore on its own.

That difference in business mix is why one iron ore headline should not be applied across the whole group as if every stock reacts the same way. Retail investors often read sector stories too broadly. In reality, the market usually prices steel names through each company's position in the value chain, not through a single commodity move.

Price action still looks cautious

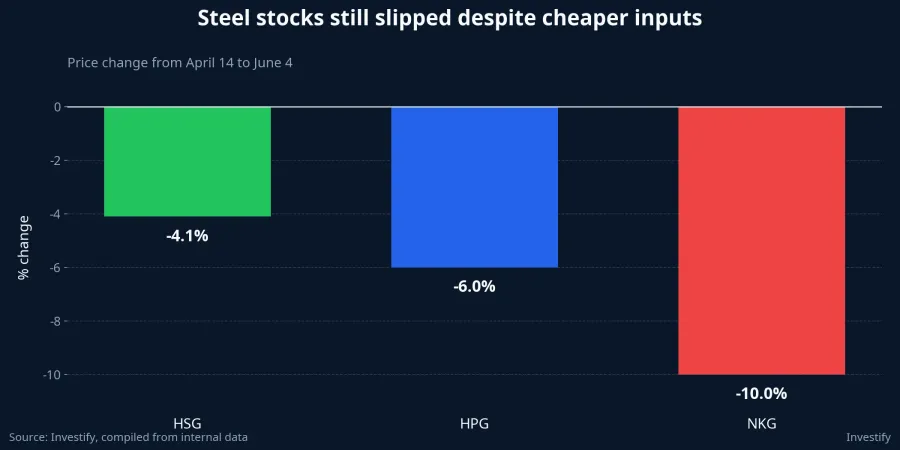

If the market truly believed that cheaper inputs were already enough to lift profits, steel equities would usually respond more positively. Instead, from April 14 to June 4, HSG fell about 4.1%, HPG fell about 6.0% and NKG dropped about 10.0%. That is not panic selling, but it is also not the pattern of a group being re-rated as a clear beneficiary.

The shorter window tells a similar story. From May 4 to June 4, HPG slipped about 2.8%, HSG lost about 3.2% and NKG declined about 5.9%. Over the same period, iron ore fell 4.1% and HRC rose 4.4%, yet steel stocks still did not deliver the kind of price response that would confirm the market had embraced the margin-recovery case.

That does not mean the sector has no upside. It means investors still want more evidence. Cyclical stocks such as steel rarely get rewarded for one favorable link in the chain alone. The market usually wants to see the whole transmission process: cheaper inputs, resilient selling prices and then visible improvement in earnings.

Domestic steel pricing is the most useful local signal

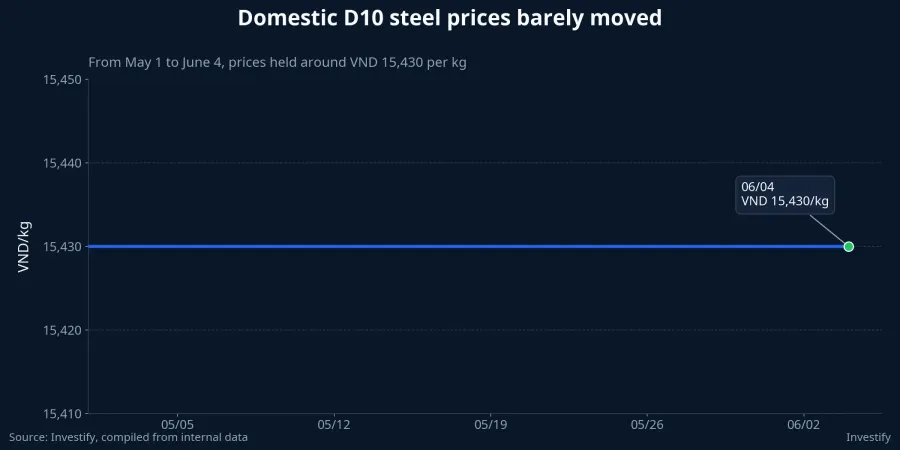

One data point deserves more attention than it usually gets: domestic D10 steel held at VND 15,430 per kg from May 1 through June 4. A flat local selling price while iron ore falls can mean two things at once. First, producers have not been forced to cut prices yet. Second, end demand may not be strong enough to push realized prices meaningfully higher either.

For newer investors, this is often a better anchor than an international commodity headline. Iron ore tells you something about costs. D10 pricing tells you something about cash generation. When realized domestic prices have not changed direction, it is too early to read a cheaper raw material as if earnings are already locked in.

If D10 begins to slide in the next few weeks while iron ore remains weak, the story becomes less constructive because the cost benefit may be offset by lower selling prices. If domestic pricing keeps holding while raw materials ease further, that is the kind of confirmation steel equities usually need.

What to monitor next

The first indicator is HRC. For flat-steel and coated-steel names, it sits closer to margins than iron ore does. If HRC holds up while ore stays soft, the margin argument gains a firmer base. If HRC turns lower, the thesis weakens quickly.

The second indicator is domestic steel pricing, especially widely watched products such as D10. This is where investors can see whether the local market is still absorbing volume at current prices. Stable selling prices matter far more than cheaper inputs that never translate into revenue and profit.

The third indicator is dispersion across HPG, HSG and NKG. If all three start improving together, the market may be reading a sector-wide recovery. If one stock firms up while the others stay soft, capital is likely differentiating by business model and end-market exposure rather than chasing the iron ore move itself.

Conclusion

The core thesis is simple: lower iron ore prices create a favorable condition, but they do not yet prove that Vietnamese steel earnings are turning higher. The market is right to wait for more than a cheaper input bill, because the decisive variables are still selling prices, HRC and each company's ability to hold margins.

So the more useful framework today is not "ore is cheaper, therefore steel stocks should work." It is "one link in the transmission chain has improved, but the next two links still need confirmation." The signals worth watching over the next two weeks are whether HRC can stay firm, whether domestic steel prices can hold and whether steel stocks begin to reflect that improvement more consistently. If those three conditions line up, the sector story becomes much stronger.