If you are new to markets, it is easy to build a rule that sounds perfectly logical: when war risk rises, gold should go up immediately. From there, a few down sessions can feel like proof that gold is no longer doing its job as a safe-haven asset. The problem is that this conclusion uses a short-term market signal to judge a structural story that unfolds over years.

Put simply, gold is living on two different clocks at the same time. The first clock moves from session to session, reacting to rates, the US dollar, oil prices, and short-term positioning. The second clock moves much more slowly and reflects how central banks and large institutions build reserves to guard against system-level risk. Once those two clocks are mixed into one conclusion, investors start reading the signal incorrectly.

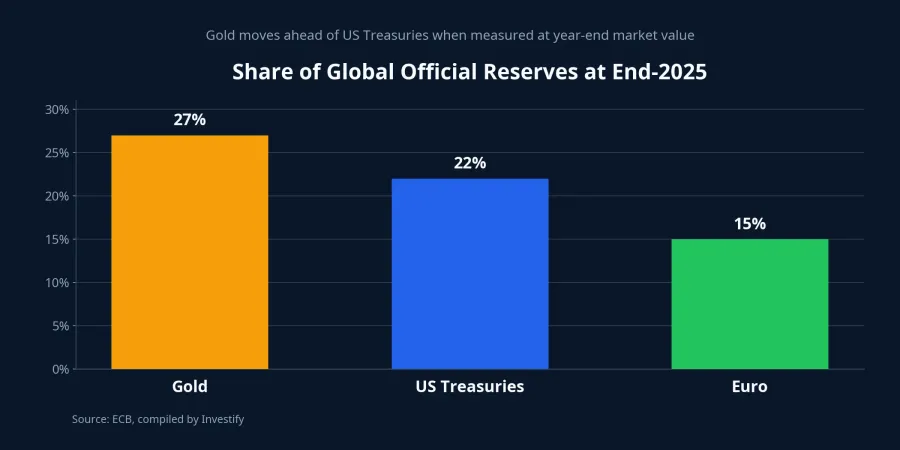

The most important development this week sits on the second clock. The ECB’s The international role of the euro, published on June 2, shows gold accounting for 27% of global official reserves at the end of 2025, ahead of US Treasuries at 22% and the euro at 15% on the same measure.ECB That is a large enough shift to challenge the old idea that gold is only a psychological hedge.

What the ECB report really says

If you stop at the 27% headline, the obvious temptation is to say gold has already replaced US Treasuries inside the global reserve system. But that is only half the story. The ECB is explicit that the jump reflects both stronger demand for gold holdings and a valuation effect, meaning the sharp rise in gold prices mechanically lifted the dollar value of reserves already sitting in vaults.ECB

That matters because official reserves are measured in market value, not in narrative. When nominal gold prices rose by about 60% in 2025 and about 30% in 2024, the stock of gold already held by central banks was repriced upward as well.ECB In other words, gold moved higher in reserve share not only because central banks bought more of it, but also because every ounce they already owned became more valuable.

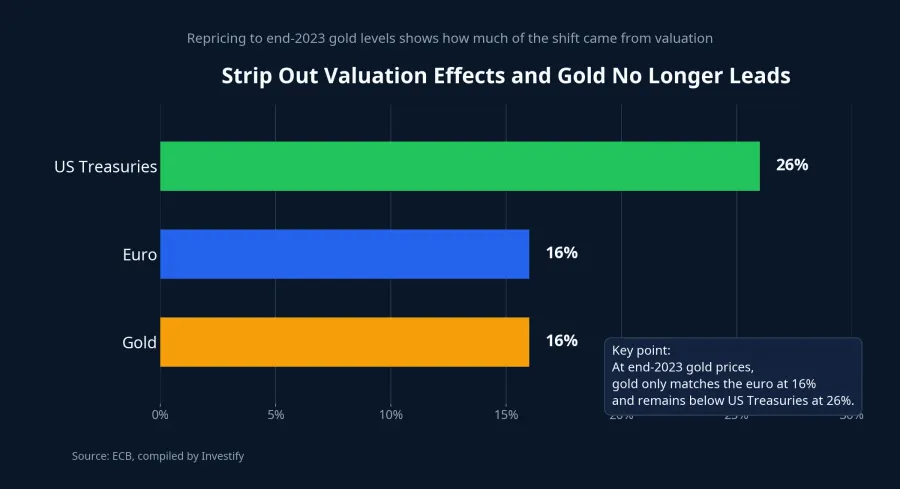

The ECB also provides a very useful stress test for retail readers. If gold is recalculated at end-2023 prices, its share falls back to 16%, matching the euro, while US Treasuries remain at 26%.ECB The right takeaway is not that gold has decisively displaced Treasuries. It is that gold’s role in official reserves is rising, but a meaningful part of that rise came from market valuation rather than pure accumulation.

Why gold can still slip over a few sessions

This is where the first clock comes back in. On June 2, CafeF cited international market moves showing gold under pressure as rising Middle East tensions revived inflation concerns, reinforcing expectations that central banks may need to keep monetary policy tighter for longer.CafeF It sounds counterintuitive, but that is exactly the mechanism many first-time investors miss.

Gold does not generate periodic cash flow the way bonds or deposits do. So when safe yields rise, or when markets start to believe rates will stay higher for longer, the opportunity cost of holding gold rises as well. A geopolitical shock can therefore push oil prices higher, revive inflation worries, and ultimately put short-term pressure on gold instead of lifting it immediately.

Think of it this way: markets do not only ask whether risk has increased. They also ask what that risk does to inflation, interest rates, and the dollar. If the answer is stickier inflation and a longer period of elevated rates, gold can easily stall or fall for a few sessions even though its long-term insurance role remains intact.

Daily price action does not cancel the long-cycle story

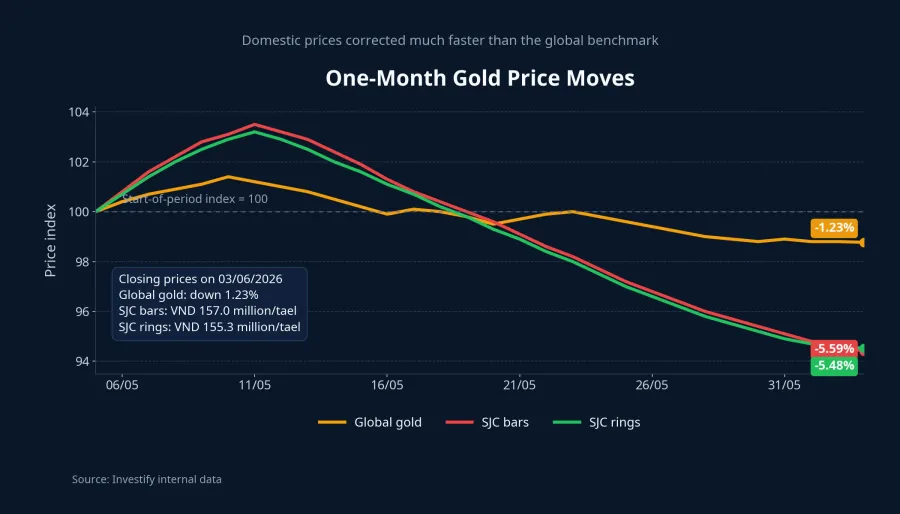

Investify’s internal data shows global gold at USD 4,467.74 per ounce on June 3, down 0.50% on the day. Versus May 4, the one-month decline is 1.23%. That matters for short-term traders, but it is still a small move when placed next to a reserve-allocation story measured by the ECB using end-2025 data.

The difference is time scale. A reserve report is describing how central banks accumulate assets over years to reduce dependence on debt instruments issued by a single sovereign. Daily gold prices, by contrast, reflect an ongoing negotiation among rates, the dollar, inflation expectations, and speculative flow. The two layers are related, but they cannot be collapsed into one conclusion for every moment in time.

This is precisely where new investors tend to make an emotional mistake. When price moves against expectation for a session or two, there is a strong urge to scrap the bigger thesis because the brain prefers simple and decisive explanations. But gold investing, like market reading in general, rarely works that way.

In Vietnam, there is an extra domestic pricing layer

Vietnamese investors do not buy “global gold” on a chart. Most people interact with SJC bars or SJC rings, which means every judgment about whether gold is rising or falling passes through an additional local premium. On June 3, SJC bars were offered at VND 157,000,000 per tael, while SJC 99.99% rings stood at VND 155,300,000. On the same day, global gold converted at the June 2 USD/VND exchange rate came to approximately VND 141,846,560 per tael.

That gap means a domestic buyer is paying not only for the global gold price, but also for branding, local supply-demand conditions, bid-ask spread, and market psychology. When that domestic premium is wide, a compression in the premium can make SJC fall much faster than global gold without saying much about gold’s safe-haven role at the global level.

Over one month, Investify’s internal data shows SJC bars down 5.59%, SJC rings down 5.48%, while global gold is down only 1.23%. That is a wide enough divergence to remind readers that the same asset called “gold” can produce very different price experiences for domestic Vietnamese buyers and for investors watching the international benchmark.

How new investors should read the three layers

The first layer is the global gold price. This is where fast reactions to rates, the dollar, Treasury yields, and geopolitics show up. If you want to understand whether the market is pricing fear or pricing inflation, this is the first layer to watch.

The second layer is domestic SJC and ring pricing. This layer is closer to the wallet of a Vietnamese investor, but it is no longer just about gold. When the domestic premium widens or narrows, the return and risk profile of local buyers can diverge sharply from the move in global gold itself.

The third layer is the reserve behavior of central banks. This is not a daily trading signal. It is longer-cycle evidence showing where gold sits inside the world’s architecture of safe assets. When the ECB shows gold at 27% of official reserves at end-2025 market values, the sensible message is that gold’s strategic role has not disappeared. The discipline investors need is to avoid turning that message into a justification for buying gold at any price.

Conclusion

A few down sessions are not enough to invalidate gold’s long-term reserve or safe-haven role. They only show that, right now, the market is reacting more aggressively to rates, the dollar, and the opportunity cost of holding a non-yielding asset. At the same time, the ECB data shows large institutions still assigning gold a meaningful place in global reserve construction.

The most coherent thesis, then, is that short-term pricing and long-cycle reserve behavior are telling two different stories, and new investors need two different sets of questions for each. The most useful signals to monitor over the next one to two weeks are the US dollar, US Treasury yields, and the premium of SJC prices over converted global gold. Those three variables will say far more about whether this is just a short correction or the start of a broader change in how domestic buyers are using gold.