When a money-market indicator drops sharply in a single session, the instinctive reaction is relief. But with Vietnam's overnight interbank rate, the more useful question is not just where it ended the day, but why it fell so quickly. The move from 11.0% to 6.60% over the first two days of June suggests that the State Bank of Vietnam stepped in at the right moment to inject short-term dong liquidity, rather than signaling that every funding concern in the banking system has already faded.CafeFCafeF

That distinction matters because the interbank rate is not the deposit rate retail savers see on their banking apps. It is the price banks charge one another for very short-term funding. When that price jumps, the market is usually saying either that some institutions suddenly need dong liquidity, or that institutions holding dong have become more cautious about lending it out.

What the quick drop actually tells us

The first takeaway from the early-June data is that the short-term squeeze was real. CafeF reported that the overnight VND interbank rate surged to 11.0% a year on June 1, up 4 percentage points from the previous session. The next session, the average rate fell by 4.40 percentage points to 6.60% a year, while the 1-week, 2-week, and 1-month tenors also eased to a 6.95% to 7.30% range.CafeFCafeF

Put simply, if a bank has to borrow dong overnight at 11.0%, that is a stress signal, not routine noise. When the rate then retreats to 6.60%, the market is telling us that the immediate bottleneck has eased. But "eased" is not the same as "gone." It is closer to opening a window in a hot room: the air improves quickly, but that does not mean the weather outside has fundamentally changed.

The mistake investors should avoid is jumping straight from that move to a broader conclusion that deposit rates will fall, the exchange rate will settle, or bank stocks will automatically re-rate. Bank liquidity has layers. The interbank market is the fastest-moving and most sensitive layer, which is exactly why it can also be the most misleading if viewed without the policy tools operating behind it.

How the SBV supplied dong liquidity

The most important part of the story is not the rate decline itself, but the mechanism behind it. According to CafeF, the SBV reopened a 14-day USD/VND swap operation, structured as a spot purchase of USD followed by a forward sale. The maximum size of the swap operation was USD 1 billion, equivalent to roughly VND 23,932 billion if fully used; the spot purchase rate was VND 23,932 per dollar and the forward sale rate was VND 23,944 per dollar.CafeF

In practical terms, banks that already hold dollars can temporarily turn that position into dong funding. At maturity, they buy the dollars back and return the dong. This is why the facility should be read as time-bound liquidity support. It addresses an immediate shortage of dong funding without implying that the central bank has opened a long-term easing channel for the entire system.

That also explains why the implied cost of funds through the swap channel was estimated at around 5% a year, well below the 11.0% overnight interbank rate seen earlier.CafeF For banks with USD on hand, the swap became a cheaper route into dong liquidity than borrowing directly in the interbank market at stressed rates. For investors, that is evidence that the SBV addressed a short-term funding layer, not that it reset the banking system's broader cost of capital.

Why it is too early to declare the pressure over

If a short-term support channel had to be reopened, the next question is why the system needed it in the first place. The answer does not sit inside a single trading day. CafeF cited market analysis suggesting that faster credit growth has pushed up banks' funding needs, while deposit rates have stopped falling after an earlier easing phase. VnBusiness also reported that BIDV raised its online deposit rate for 6-month to 11-month terms to 6.6% a year from June 1, up 1.2 percentage points from the previous schedule.CafeFVnBusiness

That detail matters for newer investors. If the interbank rate falls while medium-term and longer-term deposit rates still edge higher at some lenders, the market is pointing to two different layers of pressure operating on different timelines. One is an immediate shortage of tradable dong between banks. The other is the need for more stable funding to support credit growth over the coming months. The SBV can relieve the first layer quickly with market operations, but the second depends on credit demand, deposit competition, and the exchange-rate backdrop.

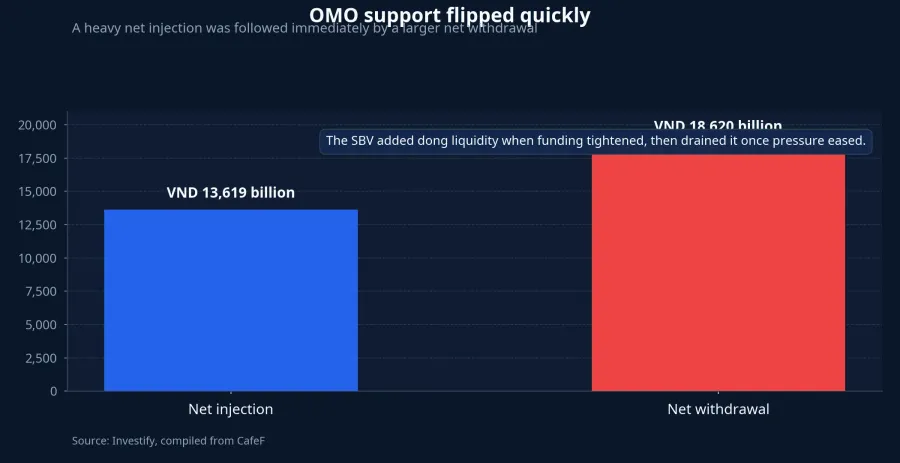

The pattern on the repo channel reinforces that reading. In the session when rates spiked, the SBV offered VND 46,000 billion at 4.5% a year and injected net liquidity of roughly VND 13,619 billion, lifting outstanding balances on that channel to VND 345,931 billion. The very next session, however, winning bids were only slightly above VND 6,000 billion while maturing paper totaled VND 24,646 billion, producing a net withdrawal of VND 18,620 billion and reducing the outstanding balance to VND 327,311 billion.CafeFCafeF

The policy message is fairly clear. The SBV is willing to add liquidity when the market is short of dong, but it is not trying to keep the system in an aggressively funded state once the immediate tension recedes. That is different from a broad monetary easing cycle. For investors, the distinction matters because it shapes how bank stocks should be read. Technical support for short-term liquidity is not the same as immediate relief for NIM, funding costs, or sector-wide earnings.

What investors should monitor next

So the bigger picture should not be reduced to a single 6.60% print. Investify data showed USD/VND at 26,333.50 on June 2, up 0.10% from the prior session. At the same time, the VN-Index closed at 1,819.01 on June 3, down 7.46 points, yet the largest bank stocks did not see uniform selling pressure: VCB rose 0.49%, BID gained 0.48%, and CTG added 0.30%. That suggests the equity market is reading the move as evidence that a policy backstop is in place, rather than as a sign of a funding break.

Still, there is not enough evidence yet to say the risk is fully behind the system. An equally valid reading is that the market has only addressed the short-term "cash thirst," while the deeper funding question remains. If overnight rates stay lower over the next few sessions, USD/VND does not come under fresh strain, and the SBV does not need to expand support aggressively, investors will have a stronger basis to say this stress episode is genuinely fading. If short-term rates jump back while the exchange rate stays under pressure, the interpretation changes: the latest decline treated the symptom more than the cause.

The most coherent conclusion for now is that short-term liquidity pressure has eased, but the system does not yet have a clean bill of health. For retail investors, the overnight rate should be treated as a sensitive gauge of short-end funding stress. The gauge is cooler than it was. To know whether it is truly back in a safe zone, investors still need to watch three signals over the next few sessions: USD/VND, medium-term and long-term deposit pricing, and how the SBV continues to inject or drain dong liquidity through market operations.