The morning of June 3 produced exactly the kind of contradiction that tends to trap newer investors. Brent stood at USD 97 per barrel, up 1.04% on the day and roughly 5.15% above its May 27 level. On the surface, that sounds like a straightforward tailwind for Vietnamese oil and gas stocks. The tape said otherwise.

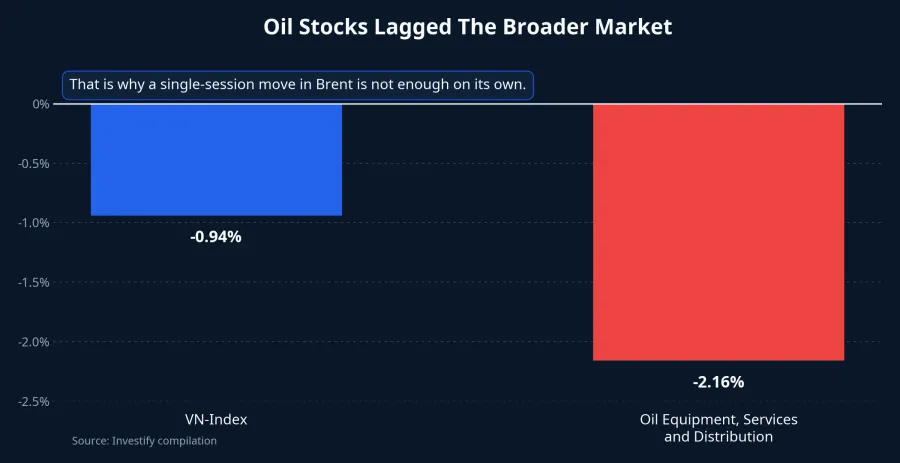

VN-Index closed the morning at 1,809.26, down 17.21 points, or 0.94%. At the same time, the Oil Equipment, Services and Distribution basket fell 2.16%, underperforming the broader market. That alone tells us the market is not treating "oil and gas" as a single trade. Investors are pricing each business link separately and asking a harder question: which companies can actually convert higher oil prices into real earnings.

The contradiction disappears once the sector is broken down

The easiest mistake is to think of oil and gas stocks as one homogeneous group. They are not. A drilling contractor, a gas distributor, a fuel retailer and an energy shipper all sit under the same broad theme, but they do not make money in the same way or on the same timeline.

That is why a move in Brent does not automatically lift every ticker at once. Equities are not barrels of oil. They are claims on future cash flow. When investors buy or sell a stock, they are not only looking at today's commodity price. They are also weighing contracts, utilization, inventory, selling prices, freight rates and the broader market's risk appetite.

Brent has rebounded, but not long enough to reset expectations

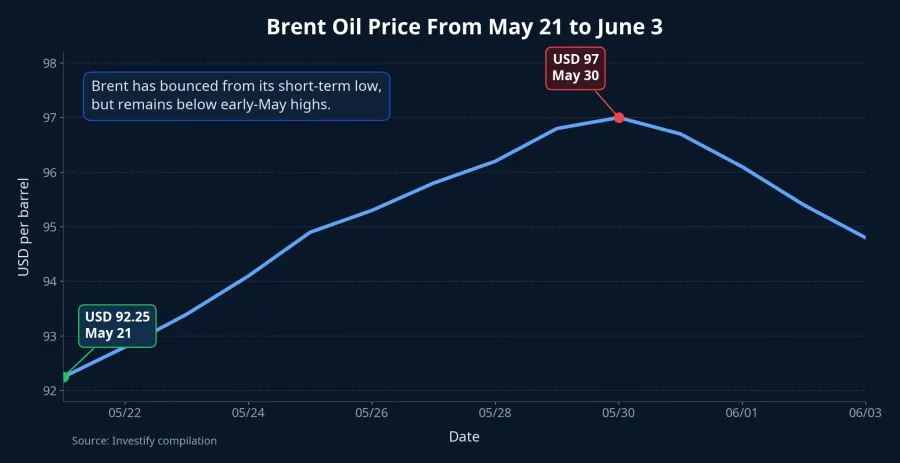

The recent price path matters here. Brent rebounded from USD 92.25 per barrel on May 21 to USD 97 on May 30, then slipped back to USD 94.8 by June 3. That is a real short-term rebound. It is not yet a durable uptrend strong enough to trigger a full rerating of the whole sector.

This is the nuance many first-time investors miss. A one-day move in oil is just a snapshot. A stock price, by contrast, reflects what investors think may happen over the next few quarters. If Brent is merely bouncing after a prior decline, money managers tend to wait for confirmation instead of repricing every oil-related name immediately.

Think of it like this: if coffee prices rise for a day, that does not mean every cafe suddenly becomes more profitable. Some operators still face weak traffic, expensive rent or inventory purchased at the wrong time. The same principle applies in oil and gas, only with far more moving parts.

Different links in the chain respond to Brent in different ways

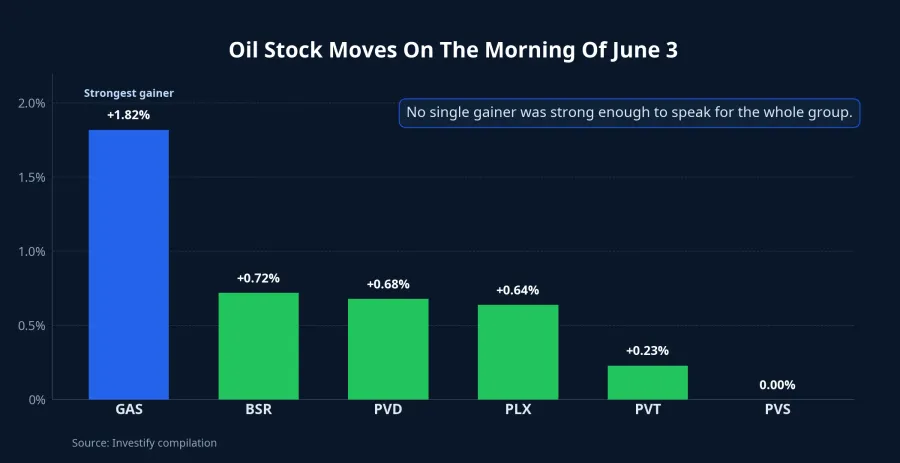

The June 3 morning session showed that divergence clearly. GAS rose 1.82% to VND 83,700 per share. BSR gained 0.72% to VND 27,900. PVD added 0.68% to VND 29,450. PLX increased 0.64% to VND 39,100. PVT edged up just 0.23%, while PVS was unchanged at VND 37,800.

That line-up makes one point obvious: no single stock was strong enough to represent the whole group. A handful of green names does not invalidate a weak sector index. And a weak sector index does not mean every company inside it is under the same pressure. Money is flowing through separate theses, not through a mechanical "buy oil stocks because oil is up" rule.

Take PVD first. Brent matters, but not in a direct same-day way. Investors care more about day rates, new contracts and when rigs are actually deployed. Higher oil prices can improve the operating backdrop, yet revenue does not jump the next morning simply because Brent prints a higher number.

PVS faces a similar time-lag issue in a different business model. Its story is tied more closely to engineering services, offshore project work and large contract execution. A stronger oil price environment may improve sentiment, but the market still wants to see project progress and contract visibility before lifting earnings expectations in a meaningful way.

GAS is another case altogether. A gas company can benefit from firmer selling prices, but results still depend on sales volumes, gas-fired power demand and margin structure across different product lines. GAS outperforming in the morning session may therefore reflect selective demand for a large-cap defensive name, not just a simplistic Brent trade.

PLX sits closer to distribution and inventory management. When oil prices rise, a fuel retailer may benefit if domestic pricing adjustments and inventory timing work in its favor. But margins do not improve automatically if global prices move faster than local retail adjustments. PVT is even more indirect. Its earnings are more exposed to shipping demand, charter rates and route volumes than to Brent itself.

The market is testing the quality of the rebound

Another reason oil names have not rallied in unison is that many had already weakened before this rebound in Brent. Over the last 10 sessions, PVD fell about 10.08%, from VND 32,750 on May 21 to VND 29,450 on June 3. PVS dropped about 6.44%, from VND 40,400 to VND 37,800. BSR lost about 9.12%, from VND 30,700 to VND 27,900.

When a group has already been sliding, one stronger commodity session is rarely enough to flip sentiment. The market usually wants to test three things. First, can oil hold higher levels for more than a few sessions? Second, can the stocks keep their gains after short-term trading flows fade? Third, will the earnings story be validated by contracts, volumes or reported results?

In other words, investors are evaluating the quality of the rebound, not just the height of Brent. That is a more demanding framework, but it is also the one that keeps people from making the lazy mistake of treating a commodity bounce as a blanket signal for every stock in the chain.

Why the sector index stayed red even with some green leaders

This is another place where the screen can mislead newer investors. A sector index is not a snapshot of the five or six names most people recognize. It is a weighted basket. If enough mid-cap and smaller names are falling, the sector index can stay red even while several large names post small gains.

That is exactly what happened on the morning of June 3. VN-Index was down 0.94%, and decliners outnumbered advancers by 158 to 130. In a market that is still this soft, a few positive oil names are not enough to confirm a broad trend reversal. Money remains selective, and selective money is usually skeptical money.

So the better question is not, "Oil is up, why aren't oil stocks all rising?" The better question is, "Which part of the oil and gas chain now has the clearest earnings evidence?" Once that becomes the frame, the morning tape looks a lot less irrational.

What investors should watch next

If you are tracking this group over the next few sessions, there are three layers worth watching beyond Brent alone. The first is the oil price itself: can it hold a higher range for several sessions rather than bounce briefly after a prior decline? A short rebound and a durable trend do not deserve the same level of confidence.

The second layer is company-specific evidence. For drilling and service names, that means contracts, day rates and project execution. For gas businesses, it means sales volumes and margin dynamics. For distributors, it means inventory, domestic pricing cycles and fuel demand. For transport names, it means charter rates and shipping demand.

The third layer is the broader market tape. When VN-Index is still weak and market breadth has not repaired, it is difficult for a sector to mount a durable move on one commodity input alone. If overall liquidity does not return, isolated green prints tend to remain isolated.

The cleanest conclusion for now is that Brent at USD 97 is only an opening signal, not a complete answer for Vietnamese oil stocks. The evidence still supports a selective view: the market is pricing this sector link by link and still demanding harder proof of earnings before it buys into a group-wide rally. Over the next few sessions, the key signals remain Brent's staying power, contract visibility and whether individual names can hold their rebound once the first burst of momentum fades.