Consumer finance is back in market conversations, but in a different language from the one investors heard a few years ago. Back then, the story was mostly about tighter lending, heavier provisions, and the cleanup of problem loans. In late-May updates, the emphasis shifted toward something else: small-ticket borrowing is returning, finance companies are leaning harder on digital channels and retail touchpoints, and growth is now being discussed alongside risk discipline rather than apart from it.VNBA

For newer investors, this is exactly where headline numbers can be misleading. In consumer finance, a better quarter does not automatically mean the industry is healthy again. A loan booked today can lift revenue almost immediately, but it takes several repayment cycles before anyone knows whether that loan was sound. That is why this segment has to be read on a slower clock than the one suggested by a single quarter of improved earnings.

What Is Actually Changing

The most useful signal is not a single stock move. It is the return of everyday borrowing demand. According to a VNBA summary published on May 31, consumer credit outstanding in Ho Chi Minh City and Dong Nai had risen to more than VND 1,610 trillion by the end of March 2026, up 4% from year-end. Most of that lending was tied to practical needs such as shopping, education, travel, and healthcare.VNBA

That matters because it suggests borrowing is moving back into ordinary household demand rather than merely showing up as a flattering corporate statistic. When credit is used for education, healthcare, home repairs, or small working-capital needs, the setup is very different from the old hot-growth phase that relied heavily on easy cash loans with much higher risk. The distinction is simple: borrowing to support a real need is not the same as borrowing just because money is suddenly easy to access.

Another major shift is the role of technology. VNBA, citing State Bank of Vietnam data, said more than 95% of credit institutions have implemented or are implementing digital-transformation strategies, while nearly 80% of financial transactions in Vietnam now run through digital channels. Once that infrastructure changes, consumer lending stops being mainly a branch-counter business or a field-sales business.VNBA

Digital Channels Make Growth Easier, Not Automatically Safer

This is where first-time investors often become too optimistic. It is tempting to assume digitization automatically makes consumer finance safer. It does not. Digital channels can move applications faster, reduce servicing costs per customer, and create richer datasets for credit scoring. But if underwriting standards loosen in the name of growth, technology can also scale mistakes much faster.

So the key question is not how quickly money is disbursed. The key question is who is receiving that money. VNBA's May 29 update described a shift toward borrowing for education, healthcare, home repairs, and small working-capital needs, while younger customers still spend on learning and experiences. If demand is genuinely moving toward uses with clearer repayment capacity, that supports the quality of the rebound. If lenders are simply pushing more volume because the recovery window looks open, delinquencies may show up a few quarters after profit improves.VNBA

This is also where investors need discipline around the phrase "new cycle." The sources from May 29 and May 31 both point in the same direction: expanding consumer credit has to go together with transparent pricing, tighter control over the purpose of the loan, and a realistic view of repayment capacity. In other words, the market wants growth again, but not a return to growth at any cost.VNBA

Even FE CREDIT, the example most frequently cited in recent coverage, reflects that logic. In the May 29 article, the focus was on digital customer journeys, loans embedded directly into shopping behavior, and broader partner reach, not merely on pushing more cash-loan volume. VNBA said FE CREDIT has served nearly 17 million customers across more than 28 million contracts and operates through a network of over 20,000 service points. Scale is an advantage, but it only lasts if every new touchpoint comes with better risk filters.VNBA

How The Stock Market Reads This Story

From an equity-market perspective, one fairly direct proxy is TIN. On June 2, the stock closed at VND 129,000, giving it a market capitalization of roughly VND 11.8 trillion. That is not proof that the entire industry has entered a fresh upcycle, but it does show that the market is willing to assign a distinct valuation to companies seen as representatives of the consumer-finance recovery theme.

The broader impact runs through parent banks. In the same June 2 session, VPB closed at VND 26,400, down 2.04%, while the VN-Index fell 0.98% to 1,826.47. A one-day gap does not prove anything structural. What it does show is that consumer finance never trades in isolation. It always sits inside a wider equation that includes funding costs, parent-bank risk appetite, and overall market sentiment.

That changes how investors should read price action. If the only takeaway is that consumer finance is recovering, it is easy to miss the fact that consolidated earnings are still shaped by deposit costs, asset quality at the parent bank, and the market's pricing of financial risk more broadly. For financial stocks, a rebound in household borrowing is important, but it is never the only variable.

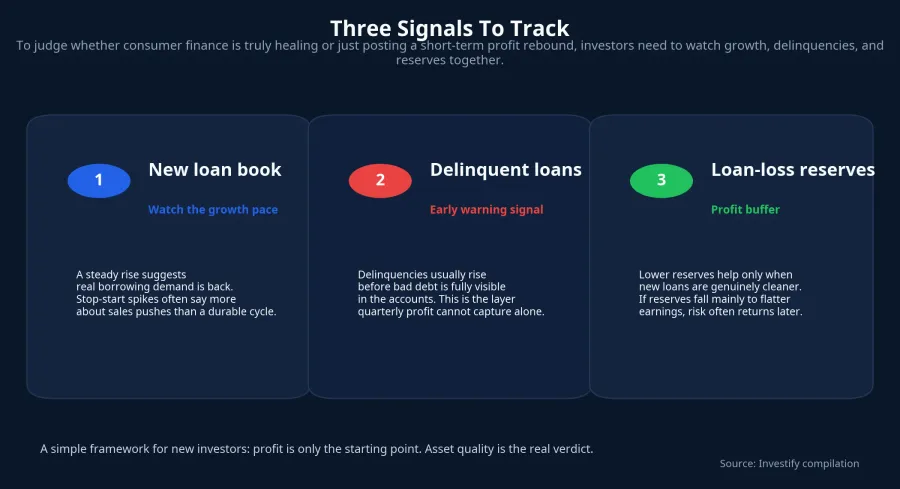

Three Better Signals Than One Quarter Of Profit

The most misleading feature of this industry is that profit often recovers faster than confidence should. A strong quarter can come from lower costs, a weak comparison base, or a burst of short-term disbursement growth. To judge whether the picture is durable, investors are better off returning to three simpler signals.

First, is the new loan book rising steadily or only in bursts. Steady growth suggests real demand is coming back. Jerky growth often signals a sales campaign rather than a durable cycle. Second, are delinquent loans rising faster than the loan book. That is the early-warning layer before bad debt becomes fully visible in reported numbers. Third, are reserves falling because new loans are genuinely cleaner, or because management wants earnings to look better. Those three questions are usually more useful than looking at net profit alone.

Conclusion: The Worst Phase Is Over, But The New Cycle Still Needs Proof

The most defensible thesis right now is not that Vietnamese consumer finance has already entered a full new upcycle. It is that the sector has moved past its worst phase and is now trying to build a more selective one. The evidence for the first half of that statement is fairly solid: essential borrowing demand is returning, digital channels are now real infrastructure rather than a side feature, and retail-linked distribution is helping lenders expand their reach again.VNBAVNBA

The evidence for the second half is still incomplete. This becomes a credible new cycle only if loan growth comes with intact risk discipline, if delinquencies do not accelerate faster than expansion, and if the new profit pool is not later reversed by heavier provisioning. That is why this theme is worth following closely. Not because the answer is already obvious, but because the market is moving into the stage where the quality of the rebound is about to become visible.