An 11% print just showed up in Vietnam's money market, and it is easy to jump straight to a dramatic conclusion: a new rate cycle has started. But if you separate the signals properly, this is first a story about a short-term VND funding squeeze between banks, not proof that deposit rates or borrowing costs across the economy have already turned higher.CafeF

The first thing new investors need to remember is simple. The overnight interbank rate is not the savings rate that retail depositors see on a banking app. It is the price banks pay to borrow from one another for a very short period to smooth payments and plug day-to-day funding gaps. So when that number spikes, the cleanest reading is pressure in system liquidity.

The core thesis here is narrow by design: 11% is a warning light at the short end of the funding market. It only becomes evidence of a broader rate reset if the pressure spreads to the one-week, two-week, and one-month tenors and stays elevated after open-market operations inject more liquidity.

What the 11% print actually means

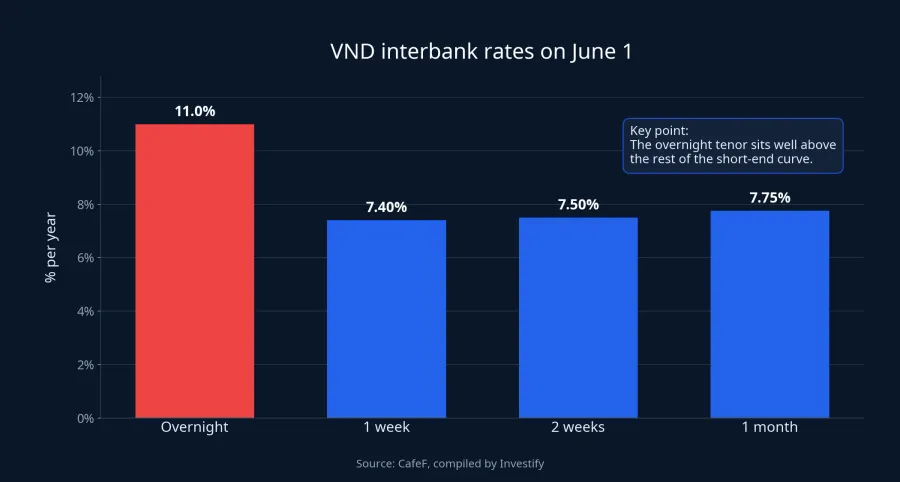

According to CafeF, the average VND overnight interbank rate jumped 4 percentage points from the previous session to 11% per year on June 1, while the one-week tenor stood at 7.4%, the two-week tenor at 7.5%, and the one-month tenor at 7.75%.CafeF The shape of that move matters more than the headline itself. The real spike was concentrated in the overnight tenor, while the rest of the short-end curve stayed high but did not steepen enough to prove that the entire funding base is moving into a new upcycle.

That distinction matters because markets tend to overreact to standout numbers. Eleven percent sounds like a full-blown rate shock, but inside the plumbing of the money market it looks more like a localized stress point than a verdict on every lending and deposit rate in the system.

Báo Đầu tư shows this pressure did not appear out of nowhere. On May 26, the overnight rate was already at 7.7% per year, while the one-week and two-week tenors both stood at 7.5% and the one-month tenor at 7.2%.Báo Đầu tư The better reading, then, is not that the market suddenly panicked on June 1. It is that funding pressure had been building since late May, and the 11% print simply made the bottleneck impossible to ignore.

The SBV response still points to a liquidity problem

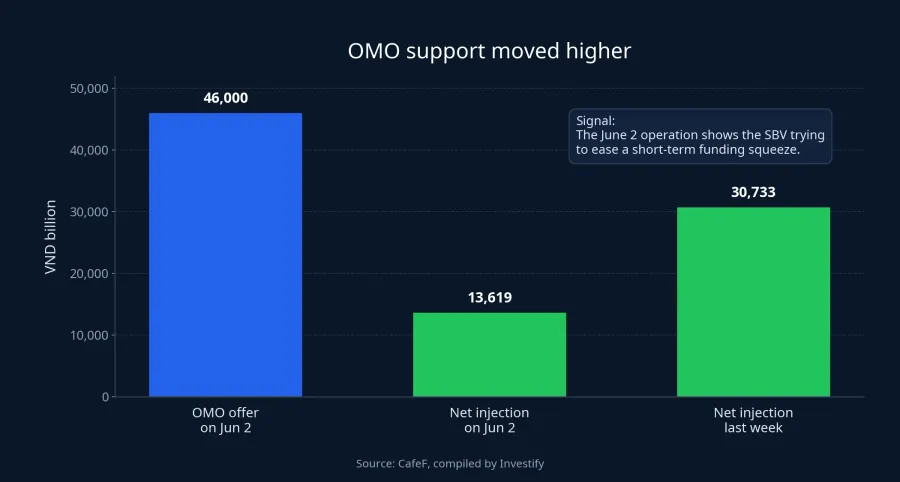

CafeF reported that on June 2, the State Bank of Vietnam offered a total of VND 46,000 billion through its collateralized lending channel at 4.5% per year; after maturities rolled off, the net injection into the system was approximately VND 13,619 billion.CafeF That makes the policy response at least as important as the headline rate itself.

Think of the banking system as a cluster of buildings sharing one emergency water line. OMO is the valve the regulator can open when pressure in that network drops too quickly. A larger operation does not mean rates will instantly fall, but it does show that the policy priority right now is to soften a short-term funding squeeze.

Earlier data reinforce the same point. CafeF said the SBV injected a net VND 30,733 billion through open-market operations over the most recent week, while Báo Đầu tư reported that the first two sessions of the prior week had already seen net injections of more than VND 13,000 billion.CafeFBáo Đầu tư In plain terms, the regulator is trying to reduce friction in the very short-dated funding layer, not signal that retail deposit rates should move materially higher.

Why depositors should not overread the signal

This is where new investors most often get tripped up. Retail deposit rates respond to a different equation: what tenor banks need to fund, how fast credit is growing, how intense competition for deposits is, and whether balance-sheet pressure lasts long enough to force a repricing. A one- or two-session spike in the overnight market may make banks more cautious, but it does not automatically force the whole system to raise publicly posted deposit rates.

One way to frame it is this: the interbank market is the basement of the system, while retail deposit rates are the price board in the storefront. Heat in the basement does not guarantee the storefront changes its sticker price immediately, because there is always lag between those layers.

Even the CafeF source carries that broader nuance. It cited VDSC as saying room for further rate cuts is limited in the near term because foreign-currency inflows are not strong, the Fed has not cut rates, and the Fed Funds Rate remains around 3.5% to 3.75%.CafeF That is a statement about the wider funding environment, not confirmation that savings rates will rise immediately after one overnight print at 11%.

So the real thing to watch is not fear of higher rates in the abstract. It is the durability of the pressure. If the overnight rate cools quickly after more OMO support, this was probably a temporary cash squeeze.

How bank stocks and margin loans actually feel it

Another common mistake is to see higher interbank rates and immediately conclude that bank stocks must fall. In reality, elevated short-end rates first hit sentiment because investors worry that funding costs will squeeze NIM. But pressure on earnings does not come from one sharp overnight print.

The same logic applies to margin lending. Margin costs also depend on each broker's funding sources, banking relationships, promotional programs, and competitive strategy. So one shock in the interbank market does not automatically turn margin rates higher, though persistent pressure would make further cuts harder to sustain.

There are at least two plausible explanations moving together here, and investors should keep both in view. One is that the market is reacting to a real liquidity issue inside the banking system. The other is that traders are over-amplifying a striking number in an already defensive tape. The evidence right now leans more toward the first explanation in the money market itself, but it is still not enough to pin every move in bank shares on a single cause.

The right checklist for the next few sessions

If this entire story has to be reduced to one practical checklist, it comes down to three layers. First is the interbank layer: does the overnight rate cool, do the one-week and one-month tenors move in the same direction, and does OMO support remain in place. Second is the retail funding layer: do banks broadly raise public deposit rates, or are changes still isolated. Only the third layer is market impact: do funding costs and risk appetite actually deteriorate, or are prices merely swinging on emotion.

That is why the right conclusion is not to dismiss the 11% print. It is worth watching because it says something real about a short-term funding squeeze in the system. But it still does not prove that deposit rates will rise immediately, that borrowing costs will move higher right away, or that bank stocks have already entered a new valuation regime. The most coherent thesis for now is to watch whether the pressure fades after OMO support, or whether it spreads deeper into the rest of the curve. Only the second scenario would truly change how investors should read Vietnam's rate story in June.