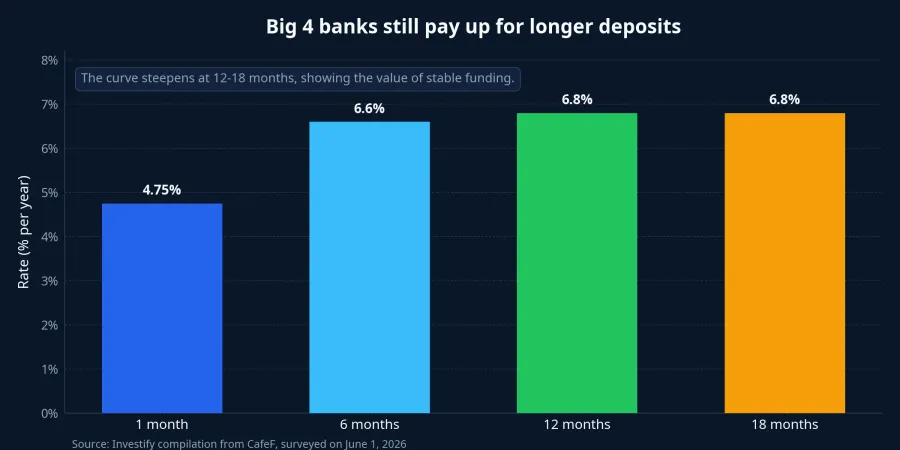

At the start of June, the most useful signal in Vietnam's deposit market is not which bank posts the single highest number. It is the curve. The four state-owned commercial banks are still offering 6.8% per year for online deposits at 12 months and 18 months, while 1-month money sits at 4.75%.CafeF

That is the cleanest way to read what banks actually want. They are still willing to pay up for money that stays longer. In plain terms, the policy push to lower rates is real, but so is the banking system's need to hold on to stable funding.

The real clue is the slope, not the headline

Retail savers usually start by asking a simple question: which bank pays the most? That is understandable, but it misses the deeper signal. What matters just as much is how much extra a bank is willing to pay when a depositor moves from a short tenor to a longer one.

CafeF's June 1 survey shows the four state-owned banks at 4.75% per year for 1-month and 3-month deposits, 6.6% for 6-month and 9-month money, and 6.8% for 12-month and 18-month terms.CafeF That progression matters more than any isolated figure because it shows banks are not merely seeking deposits. They are seeking deposits with the maturities they need.

The intuition is simple. A short deposit helps a bank manage day-to-day liquidity. A longer deposit helps it plan against a longer asset book, especially when lending demand and balance-sheet management still require stable funding. So if the long end of the deposit curve refuses to soften, the message is not subtle: those liabilities still matter.

Why the long end did not fall right away

In April and May, the State Bank of Vietnam repeatedly asked commercial banks to follow the policy line of lowering deposit and lending rates, while also tightening supervision around implementation.Báo Chính phủ But policy direction and actual funding needs do not always move at the same speed. If a bank still values stable liabilities, it will usually cut less aggressively at longer maturities than at the short end.

This is where many readers over-simplify the story. They hear that the central bank wants lower rates and assume the whole deposit table should instantly shift down in parallel. In practice, rates are still prices. They respond both to policy pressure and to the balance-sheet constraints of individual institutions.

If liquidity were abundant enough that banks no longer cared about locking in longer money, the premium on 12-month and 18-month deposits would narrow quickly. That has not happened yet. The right interpretation is not that banks are ignoring the policy signal. It is that the push for lower rates is still colliding with a live need for dependable funding at the long end.

What the spread with private banks is telling you

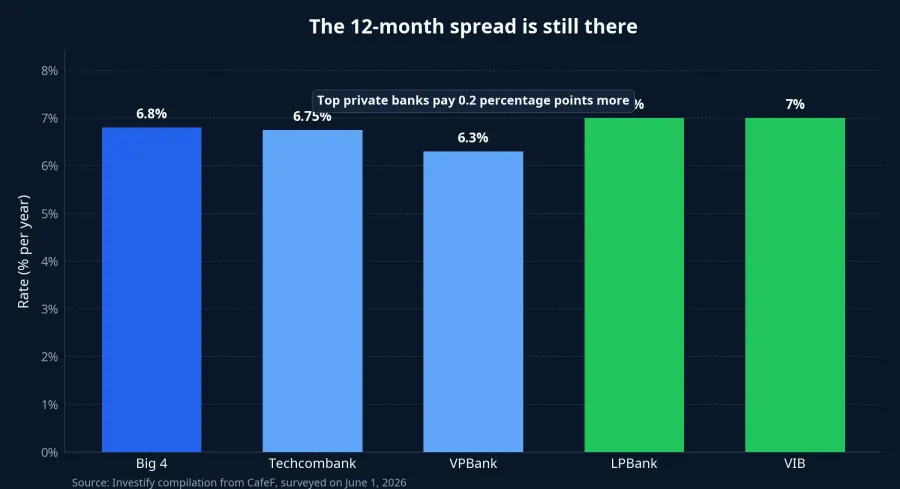

A second way to read the market is to compare the same tenor across institutions. At 12 months, Techcombank is offering 6.75% per year, VPBank 6.3%, while LPBank and VIB are both at 7.0%.CafeF The gap between the state-owned group at 6.8% and the highest private-bank offers at 7.0% is not dramatic, but it is still there.

A 0.2 percentage point difference may look minor on paper. For a larger deposit held over a full year, it is enough to change behavior at the margin. For banks, it is an extra funding cost accepted in exchange for greater stability. When several lenders are still willing to pay that premium, the message is that competition for longer money has cooled from crisis levels, but it has not disappeared.

CafeF's survey suggests the gap between the state-owned group and private banks still ranges around 0.2 to 0.5 percentage points at maturities of 12 months and above.CafeF That matters because it keeps the interpretation disciplined. The market is no longer in an obvious funding race, but there is still not enough evidence to say that the long-term funding premium has fully faded.

Interbank rates say short money is not exactly cheap

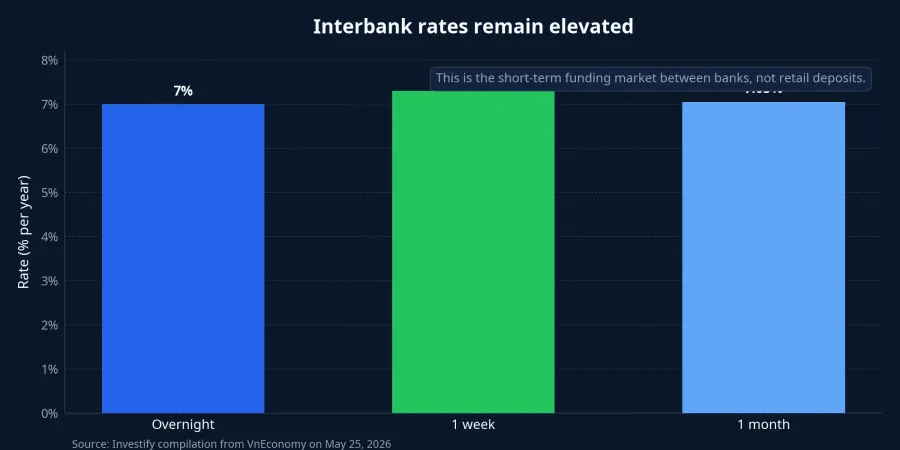

To understand why the long end remains firm, it helps to look at the interbank market as well. On May 25, overnight VND interbank rates stood at 7.0% per year, the 1-week tenor at 7.3%, and the 1-month tenor at 7.05%. On the same day, the State Bank injected a net VND 4,552.09 billion through the repo channel, taking outstanding balances there to VND 306,130.92 billion.VnEconomy

This is not the retail deposit market. It is the short-term funding market between banks. Even so, it remains a useful thermometer. When short-dated funding still trades in elevated territory, it becomes harder to argue that the entire deposit curve should fall quickly and uniformly.

That does not mean deposit rates mechanically mirror interbank rates. The two markets serve different functions. But they do point in the same direction: funding conditions are not loose enough yet for banks to stop rewarding longer-term deposits without thinking about stability.

What this means for savers and first-time investors

If you are primarily a saver, the better question is not whether rates will instantly rise or fall next week. The better question is which maturities banks are still willing to reward. If the premium still sits at 12 months and 18 months, the market is telling you that stable deposits still carry value. The trade-off is lower flexibility if the rate backdrop shifts later.

If you are comparing deposits with other assets, long-term deposit yields around 6.8% to 7.1% per year now set a serious hurdle rate.CafeF Equities, mutual funds, bonds, or other fixed-income products need to justify why their expected return is worth the extra volatility, liquidity risk, and uncertainty.

This is where many first-time investors misread the environment. Higher bank rates do not automatically mean money vanishes from risk assets. Some cash will stay parked in deposits for longer, yes. But some will still move into higher-risk products if the expected payoff remains compelling enough. What changes is not the existence of capital. What changes is the return threshold investors demand before taking risk.

Conclusion: Read the slope before you predict the direction

The evidence points to one main conclusion: early June does not show that the pressure to retain long-term funding has gone away. It shows that the easing process is uneven across maturities. The short end may soften sooner. The long end is still holding because banks are not yet ready to give up stable liabilities.

The most useful signals to monitor over the next few weeks are the slope between short maturities and the 12-18 month bucket, and the spread between state-owned banks and private lenders. If both narrow at the same time, the case for easing funding pressure becomes stronger. If long deposit rates stay sticky while short rates only drift lower slowly, the core message remains intact: in Vietnam's banking system, stability still commands a price.