May was a useful stress test for one of the most common reflexes among newer investors: if the Middle East heats up, gold and oil should rise together while stocks fall together. That logic sounds tidy when all you have is a news headline. It breaks down once you line up the three assets Vietnamese investors actually watched through the month and compare what they really delivered.

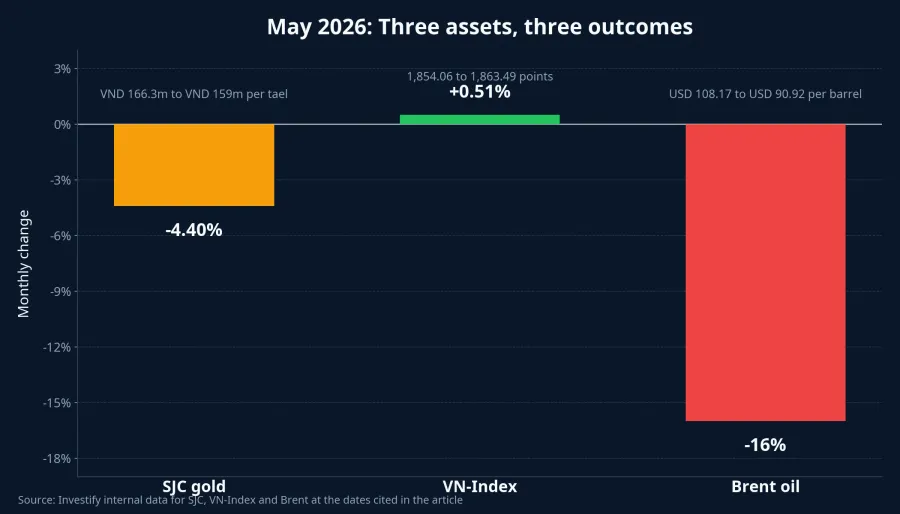

SJC gold prices moved from VND 166.3 million per tael on May 4 to VND 159 million on May 30, a decline of about 4.4% for the month. The VN-Index rose from 1,854.06 points on May 4 to 1,863.49 on May 29, or roughly 0.51%. Brent, by contrast, fell from USD 108.17 per barrel on May 1 to USD 90.92 on May 29, a drop of about 16%. The same month of war headlines, negotiation signals and easing-risk expectations produced three very different answers because those assets were responding to three different questions.

One month, three paths

The main lesson is not that one asset was simply "right" and the others were wrong. The lesson is that each market reacts to a different layer of pressure. Gold in Vietnam does not move only with international bullion prices; it also reflects domestic spreads, FX conditions and local demand to hold physical wealth. Vietnamese equities are not a single price like a commodity benchmark, but an aggregate of sectors pulling against one another. Brent, meanwhile, is a global supply-chain price, so when the market removes a geopolitical risk premium, the adjustment can be fast and brutal.

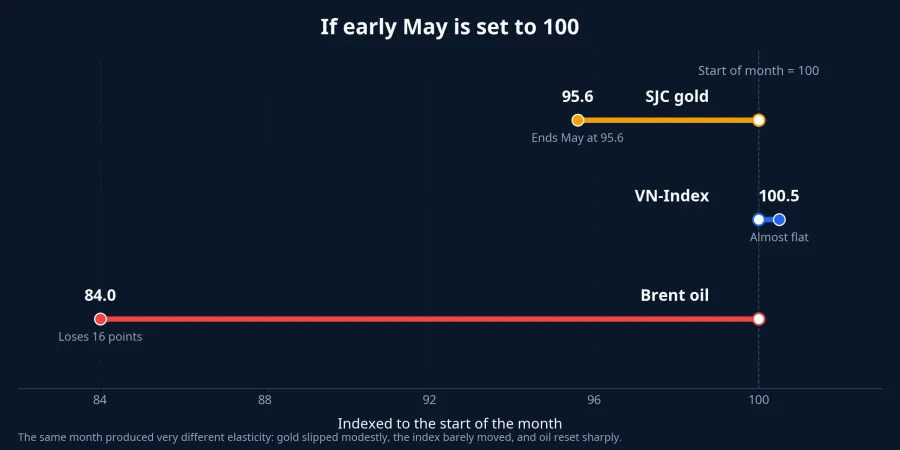

If you rebase early May to 100, the contrast becomes clear. SJC gold ends the month around 95.6, meaning it lost far less than oil. The VN-Index sits almost flat at roughly 100.5. Brent falls to about 84.0. That is not a contradiction. It is exactly what you would expect when gold is acting as a store-of-value vehicle, equities are reflecting capital flows and earnings expectations, and oil is repricing direct supply risk.

SJC gold: Better at holding value, not built for quick trading

A 4.4% monthly decline does not make gold look like a perfect haven. That observation is true, but only partly. SJC gold still held up far better than Brent and remained far less exposed than equities to a short-term correction in risk appetite. For investors whose first priority is preserving purchasing power rather than chasing immediate gains, that distinction still matters.

The complication is that buying gold in Vietnam is not the same as watching spot gold on an international chart. On the morning of May 30, CafeF reported SJC gold at VND 156 million bid and VND 159 million offered per tael, while the converted global gold price was only about VND 144.4 million.CafeF That gap of more than VND 14 million per tael means Vietnamese buyers are not just purchasing a defensive asset. They are also buying into a market with its own domestic supply-demand premium.

The more practical number for first-time investors may be the trading spread. The same CafeF report put the SJC buy-sell spread at VND 3 million per tael on May 30.CafeF In plain language, a buyer who enters in the morning and wants to sell immediately has to overcome that spread before making any real money. So yes, gold did its job better than oil in May if the job was capital preservation. No, that does not make it a friendly short-term trading instrument.

This is where investors often overstate the message. Gold holding up better does not mean gold must always rise whenever the world turns unstable. What May shows instead is that gold absorbs stress in a slower, thicker and less linear way than oil does. It can still decline, but its path is cushioned by local hoarding demand and the structure of the domestic market.

VN-Index: A flat index does not mean a calm portfolio

The VN-Index is the easiest asset in this group to misread. The benchmark ended May at 1,863.49 points, up 0.51% from April.Nhân Dân On the surface, that could suggest Vietnamese equities largely shrugged off the geopolitical noise. That is too flat a reading for a market whose direction depends on breadth, sector rotation and who is supplying the money.

In the final week of the month alone, the VN-Index fell 0.73% and foreign investors sold a net VND 4,920 billion on HoSE.Nhân Dân For the full month, VIX calculated net foreign selling at VND 19,828 billion.VIX Yet the broader index still did not break down. That tells you the market had offsetting support inside it: domestic money absorbed part of the pressure, some sectors still held their ground, and foreign outflows were not large enough by themselves to drag the whole market into a single-direction move.

For newer investors, this is where the distinction between "the index" and "my portfolio" matters. An index can look flat because one group rises while another group falls. If your holdings are concentrated in the wrong pocket of the market, your lived result can look nothing like the benchmark’s headline. In that sense, the VN-Index in May did not disprove risk. It simply showed that equity risk often arrives in layers rather than through one number.

The month also argues against drawing a straight line from geopolitics to all Vietnamese equities. The relationship exists, but it is not linear. Stocks still have to pass through interest-rate expectations, earnings quality, foreign selling pressure and domestic risk appetite. When those variables are not moving in one direction together, the index can stay roughly flat even as investor emotions do not.

Brent: Direct exposure to the supply-risk premium

Brent was the cleanest and sharpest mover of the month because its pricing is tied directly to the global energy flow. Brent slid from USD 108.17 per barrel on May 1 to USD 90.92 on May 29, a monthly decline of about 16%. That is not a trivial move, but it is still better described as a powerful repricing than as panic. The market was steadily taking geopolitical risk premium back out of the barrel price as expectations tilted toward de-escalation.

Đại Đoàn Kết reported that front-month Brent settled at USD 92.05 per barrel on May 30 and that May was the steepest monthly drop since March 2020.Đại Đoàn Kết The same report tied that decline to expectations that the Middle East conflict could ease and that traffic through the Strait of Hormuz could normalize again.Đại Đoàn Kết The causal chain is clearer here than in gold or equities because oil is answering a very physical question: can cargo move, is supply blocked, and how much extra does the buyer still have to pay for transport and disruption risk?

That is exactly why oil is the easiest asset to misclassify if you come to it with a capital-preservation mindset. When risk rises, oil can jump fast. When that premium fades, the market can give it back just as quickly. That does not make oil a bad asset. It just means oil suits investors who are deliberately tracking commodity risk and can tolerate sharp swings, not investors looking for a stable buffer inside a household portfolio.

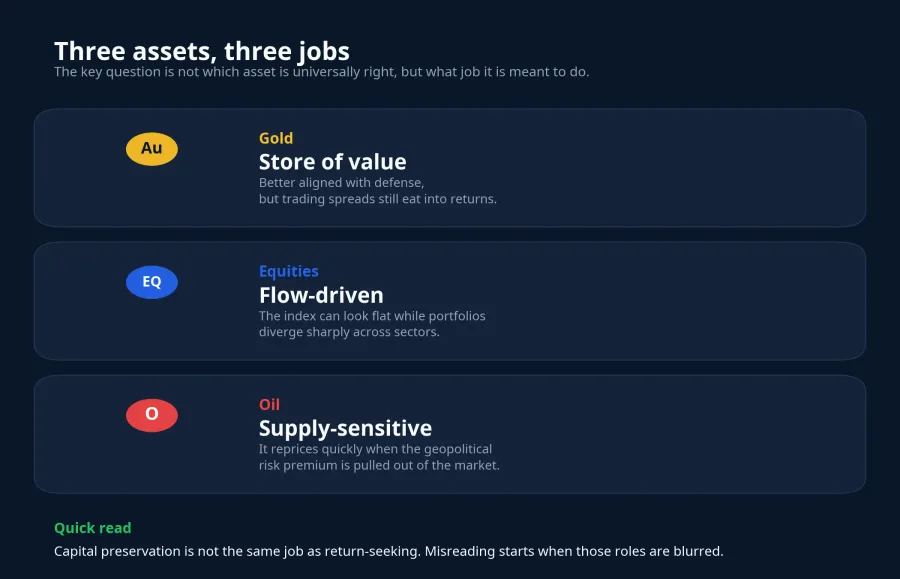

Conclusion: Match the asset to the job

If the month supports one conclusion, it is that investors should stop throwing gold, stocks and oil into the same reflex bucket. One geopolitical backdrop does not produce one shared outcome across all asset classes. SJC gold did a reasonably good job of preserving value, but its domestic premium and trading spread matter. The VN-Index showed resilience through internal offsets, but a flat benchmark is not the same thing as portfolio safety. Brent moved the fastest because it was tied most directly to global supply expectations.

That has a very practical consequence for any investor. If the goal is to preserve purchasing power, read gold through the lens of spreads and local premium, not just through the word "haven." If the goal is to seek growth, equities remain the core channel, but they need to be read through sector breadth and money flows rather than through the index alone. And if the goal is to trade commodities, oil demands acceptance that a single shift in supply expectations can compress price very quickly.

Markets will keep handing investors messy months like May. The most useful watch list for the next one or two weeks is therefore separate by asset: the SJC-versus-world spread for gold, breadth and flows inside the VN-Index, and the evolution of Hormuz-related risk for Brent. Investors make fewer mistakes when they ask each asset the right question.