More credit for social housing sounds like an instant fix. In practice, it is not. Money does not move straight from a policy letter to apartment keys. It still has to clear three gates: projects that are legally ready, banks that can underwrite the risk, and households that can live with a mortgage stretching over many years.

Put simply, policy is opening a wider lane for capital, not guaranteeing that capital will move quickly. If one of those three links stays weak, the headline will look better than the lived result. That distinction matters because retail readers often hear "credit easing" and assume supply, affordability, and sales will all improve at once.

The credit door is opening wider

The newest policy shift is about how the State Bank of Vietnam treats real-estate credit in 2026. Per a document cited by Thanh Niên, from January 1, 2026 through December 31, 2026, the increase in outstanding loans for social housing, industrial parks, and export processing zones versus the end of 2025 will be excluded from real-estate credit balances when authorities monitor credit growth in that sector.Thanh Niên

In plain English, banks now have more room to lend into priority segments without hitting the same real-estate bucket. That matters because social housing is not speculative land or premium apartments. It is a real-demand product, and it usually needs longer loan tenors and steadier repayment structures.

This is not a market starting from zero. By mid-March, outstanding social housing loans had already reached roughly VND 41 trillion, including more than VND 25 trillion at the Vietnam Bank for Social Policies and over VND 16 trillion at commercial banks.Thanh Niên So the question is not whether capital exists. The question is how fast it moves and who receives it first.

The bottleneck is bigger than the word "easing"

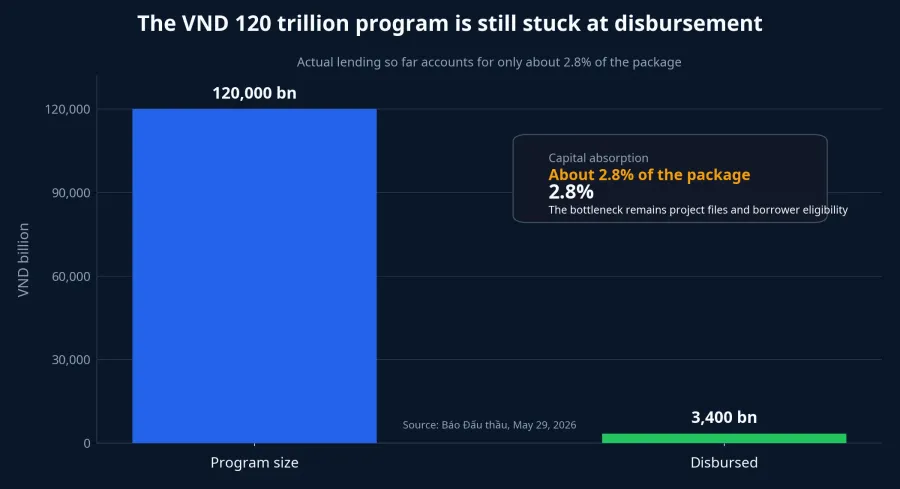

The easiest mistake is to see a large policy program and assume disbursement must also be large. Báo Đấu thầu reports that the VND 120 trillion credit package for social housing was meant to be the key lever for the segment. Yet by late May, only 38 out of 63 provinces and cities had published lists of eligible projects, equal to about 100 projects with borrowing demand of roughly VND 70 trillion.Báo Đấu thầu

On its own, "100 eligible projects" still sounds encouraging. But the picture changes once you compare that with actual lending. Total disbursement has reached only around VND 3.4 trillion, which is still below 3% of the full package.Báo Đấu thầu

That gap tells us the real issue is no longer whether the package exists. It does. Whether initial project lists exist. They do. The problem is that money still moves slowly through legal approvals, project readiness, collateral requirements, construction progress, and borrower repayment capacity.

The internal split of disbursement adds another important layer. Of the VND 3.4 trillion already disbursed, about VND 2.94 trillion went to developers across 21 projects, while homebuyers received only around VND 460 billion across 19 projects.Báo Đấu thầu In other words, money is flowing more easily to the supply side than to the end-user side. For a program with a clear social mandate, that is not a small detail.

Why buyers still do not feel relief

Many people assume that if banks are allowed to lend more, buyers will immediately feel lighter pressure. That misses the structure of a social housing mortgage. Báo Đấu thầu says the current preferential rate is only about 1.5 to 2 percentage points below average commercial lending rates.Báo Đấu thầu

That affects household cash flow in a very direct way. If the discount only feels comfortable in the early phase while repayment pressure remains heavy later on, buyers will still hesitate even if, on paper, the package is available to them. For end-users, the real decision is not whether a program exists. It is whether they can map a stable repayment path over many years.

Banks face a constraint of their own. This is still lending capital that has to be recovered, so credit officers must look at project documentation, collateral, construction timelines, and the borrower profile. Policy support makes the door easier to open, but underwriting standards still decide whether someone walks through it.

The real squeeze sits between projects and borrowers

When a large credit package disburses slowly, there are at least two ways to read it. The lazy reading is that the market cannot absorb the capital. The more accurate reading for social housing is that the pipeline is still narrow in multiple places: localities publish project lists slowly, the number of bankable projects remains limited, and the distance from "eligible project" to "buyer receives funds" is still long.

That is why the 38 localities with published lists and the roughly 100 eligible projects should be treated only as the first layer of confirmation. The more important second layer is how many projects have homebuyers who actually received disbursement. By late May, that number was still just 19 projects.Báo Đấu thầu

For investors, this is where the lens needs to change. Markets react quickly to "more credit" headlines, but policy effectiveness shows up much later and only when execution works from end to end. In social housing, extra lending room is not a substitute for proof on legal readiness, actual disbursement, and eventual delivery.

What to watch next

Three signals matter from here. First, whether the list of eligible projects broadens steadily across localities. Second, whether the VND 120 trillion package moves clearly beyond the current sub-3% disbursement zone.Báo Đấu thầu

The third signal is the one that matters most: whether lending to homebuyers starts rising faster than lending to developers. If capital continues to stop mainly at the project level, the market may gain more hope but not necessarily more completed transactions. Real impact appears only when buyers can borrow, service the loan, and receive the home on schedule.

The bottom line is straightforward. Credit easing for social housing is a necessary condition because it removes one layer of pressure on the banking side. It is not a sufficient condition for supply to accelerate right away. The most credible proof in the next few months will not be another policy headline. It will be faster capital flowing to legally clean projects and then all the way through to borrowers who can actually repay.