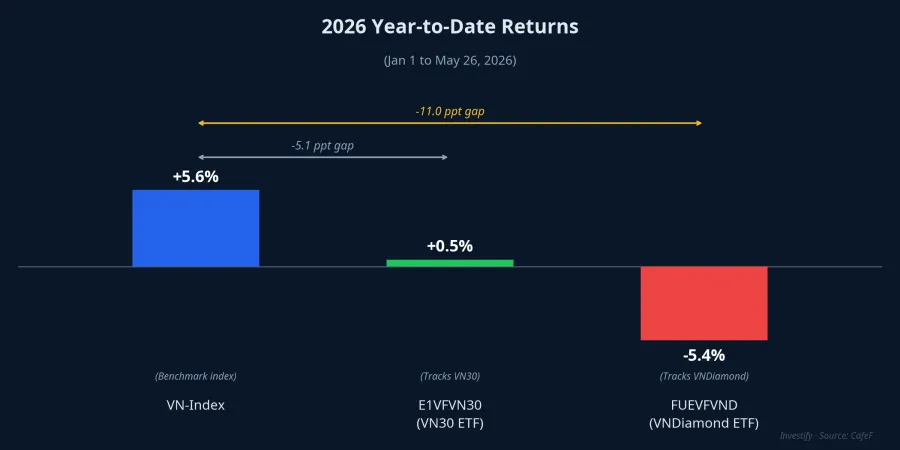

"Buy an ETF and follow the market" is the most common piece of advice given to new investors. But results from the start of 2026 through May 26 are raising eyebrows. The E1VFVN30 fund (tracking VN30) has gained only about 0.5% for the year, while FUEVFVND (tracking VNDiamond) is down roughly 5.4%. Meanwhile, VN-Index has risen approximately 5.6% over the same period.CafeF A performance gap of 5 to 11 percentage points does not mean the funds are poorly managed, nor is it a reason to panic. Understanding what is actually driving this gap is far more useful than reacting to the headline.

The Numbers: Where the Gap Stands

Think of it this way: if three investors set out on January 1, 2026 and ran until May 26, the VN-Index investor crossed the finish line up roughly 5.6%. The E1VFVN30 investor is barely ahead, up about 0.5%. The FUEVFVND investor is still behind the starting line, down approximately 5.4%.

Here is what matters: both funds are still tracking their respective benchmarks reasonably well. The problem is not that they are drifting from their target indexes. The problem is that their target indexes are built differently from VN-Index. This year, that construction difference has mattered a great deal.

Why It's Happening: It Comes Down to Index Construction

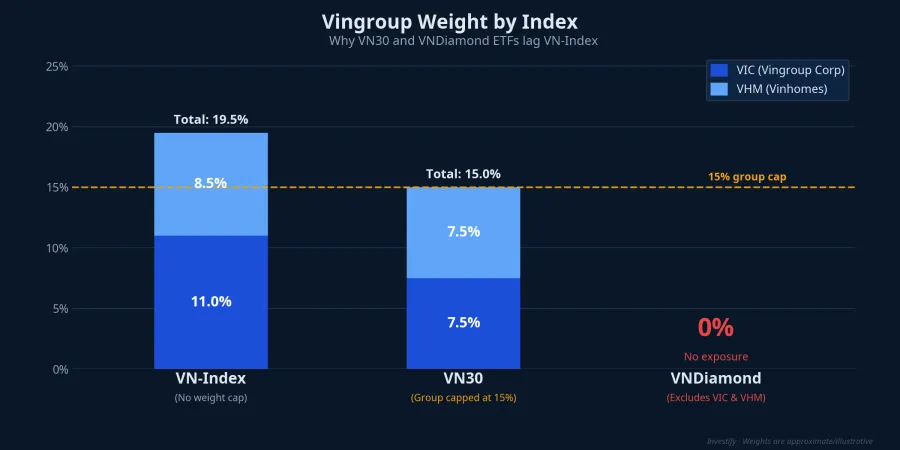

In 2026, VN-Index has been powered primarily by the Vingroup group. VIC and VHM have been the main drivers pushing the index to new highs.VietnamBiz Since VN-Index is calculated using full market-cap weighting with no concentration limits, when large Vingroup stocks rally, the index captures every bit of that move.

VN30 operates under different rules. HOSE's index methodology caps any single stock at 10% and limits the combined Vingroup conglomerate (VIC, VHM, VPL) to a maximum of 15%.PHS The reality, however, is that VIC alone represents approximately 15.16% of free-float market cap. In other words, the VN30 index deliberately compresses the Vingroup weighting, so even when VIC and VHM surge, a VN30 ETF only captures a fraction of the upside compared to VN-Index.

The rebalancing mechanism adds another layer of drag. During the early-2026 index review (announced January 21, completed February 2), VN30 ETFs were required to sell approximately 5 million VIC shares in order to bring the group's weighting back below the cap.VnEconomy That means the fund was forced to trim its best-performing holding at exactly the moment that holding was pulling the broader market higher. This is an inherent feature of any cap-weighted index rule, not a mistake by the fund manager.

VNDiamond: No VIC, No VHM

With FUEVFVND, the story is even more straightforward. The VNDiamond index selects stocks that have reached their foreign ownership limit, which effectively excludes VIC and VHM entirely. After the most recent rebalancing, the largest holdings were FPT at approximately 15%, MWG at roughly 15%, TCB at about 9.4%, PNJ at around 9.1%, and ACB at approximately 7.2%.VnEconomy These are primarily banking, retail, and technology names.

In 2026, none of these sectors have been the primary market driver. When you hold a basket with zero exposure to the two stocks pulling the index to new highs, lagging by 11 percentage points is an expected outcome, not a surprise.

Fund Fees: Real, But Not the Main Culprit

A common misconception is that the performance gap stems from fund fees and tracking error. These factors exist — a passive ETF typically carries costs below 1% per year — but they simply cannot explain a 5 to 11 percentage point gap within five months. The overwhelming driver remains index construction: VN30 compresses the Vingroup weighting, and VNDiamond excludes it entirely. Attributing the gap to fees means misreading the fundamental cause.

The Prior Two Years Tell a Different Story

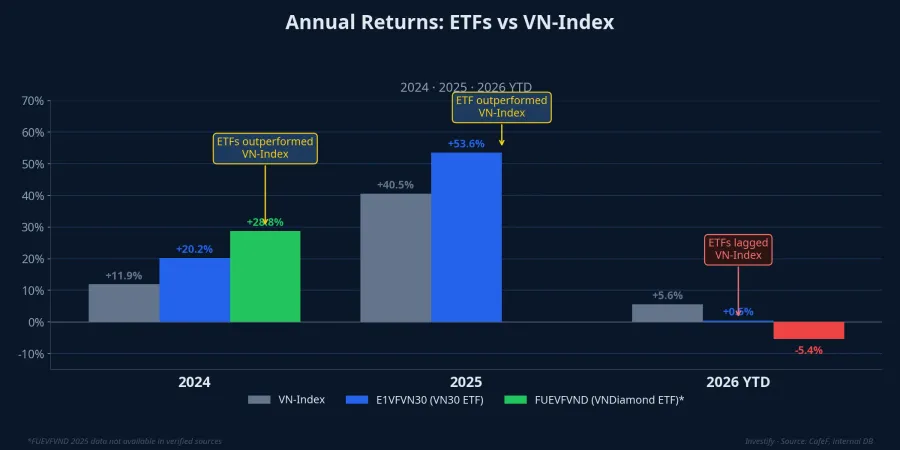

To assess these funds fairly, it helps to look at recent history. In 2024, FUEVFVND returned approximately 28.8% and E1VFVN30 gained roughly 20.2%, while VN-Index rose only about 11.9%. In 2025, E1VFVN30 surged approximately 53.6%, well ahead of VN-Index at around 40.5%.

The takeaway is that an ETF's relative performance depends on the type of market rally, not on fund quality. When market gains are broad-based or concentrated in the large-cap stocks that populate these indexes, both ETFs track or beat VN-Index. When the rally narrows to a handful of stocks that VN30 caps and VNDiamond excludes — as was the case with Vingroup in 2026 — these ETFs fall behind. This is a structural characteristic, not a flaw.

Thai Investor Outflows: Reading the Signal Correctly

A point attracting attention recently is that Thai investors have been redeeming their positions in both funds. They access Vietnamese ETFs indirectly through Depositary Receipts (DRs) issued by Bualuang Securities in Thailand. Since the start of the year, DR units linked to E1VFVN30 have fallen by roughly 11.8 million units to approximately 90.4 million, equivalent to around VND 3,200 billion, the lowest level in several years. DR units linked to FUEVFVND have declined by approximately 10.9 million units to over 112 million, equivalent to roughly VND 4,000 billion.CafeF

The causal direction matters here. Thai investors are most likely selling because of the funds' weak performance, not causing that weakness by selling. This is a lagging signal reflecting what has already happened, not a leading indicator that the market will fall further. Do not treat a foreign outflow figure as a sell signal for your own portfolio.

What Investors Should Take Away

The most important thing is to understand exactly what you own. A VN30 ETF or a VNDiamond ETF is not a VN-Index tracker. If your goal is to replicate VN-Index returns, both products follow different indexes with different weighting methodologies. That distinction matters before you decide whether to hold, adjust, or switch products. It is also a very different conclusion from simply saying "the fund is underperforming."

Two signals are worth monitoring going forward. First, market breadth: if the rally remains concentrated in VIC and VHM, the performance gap between these ETFs and VN-Index is likely to persist. If capital broadens into banking, retail, and technology — the sectors that dominate VNDiamond — these funds could close the gap. Second, the next VN30 and VNDiamond rebalancing date is worth watching, as it will determine which stocks the fund must buy and sell, and at what weights.

The right question to ask is not "what are foreign investors doing?" — it is "does the index I own match my expectations for how this market will move?" That is the question that actually shapes long-term portfolio outcomes.