On May 25, 2026, in Rome, Ferrari unveiled the Luce, its first fully electric car in the company's 90-year history and the first five-seat model Maranello has ever produced.CNN The car features four electric motors, one per wheel, delivering a combined output of 1,035 horsepower, a top speed exceeding 310 km/h, and a range of over 500 km.Dezeen Starting at €550,000, or approximately $640,000, the Luce is the world's most expensive electric car at launch. The exterior and interior design was created by Jony Ive, designer and co-founder of studio LoveFrom, together with Marc Newson, industrial designer and co-founder of LoveFrom, following five years of close collaboration with Ferrari's engineering team in Maranello.

On the surface, this was a historic milestone worth celebrating. Yet in the trading session that followed, RACE shares fell as much as 8% intraday before closing down around 6% in Milan, the steepest single-session decline since October 2025.CNBC The first wave of analyst and social media commentary focused not on the car's specifications, but on its appearance: many said the Luce resembled a Tesla Model 3 or a mainstream family sedan, "not a Ferrari."CNBC

Why would a technological milestone send investors to the exit? The answer lies not in the car itself, but in what Ferrari investors have always been buying.

RACE Investors Were Never Paying for Technology

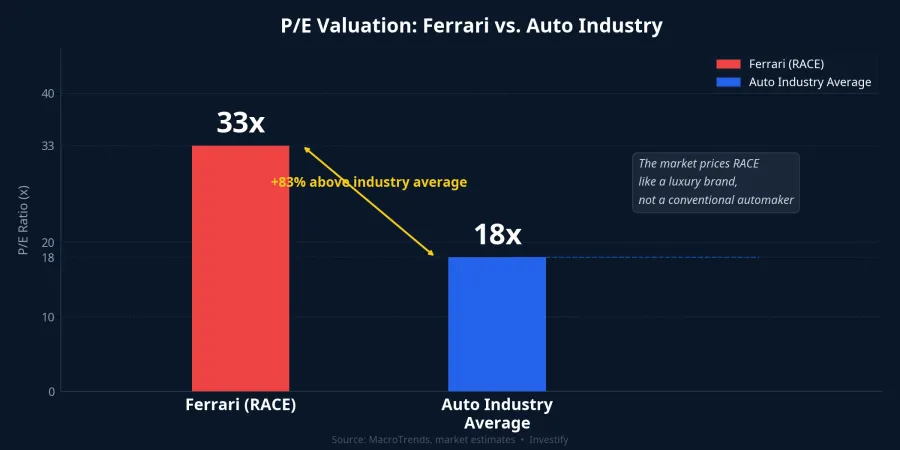

The market's valuation of RACE makes the underlying logic clear. The stock currently trades at a P/E of roughly 30 to 35 times earnings, compared with an industry-wide average of around 18 times for global automakers. A company that sells a few tens of thousands of cars per year commands nearly double the valuation multiple of the broader sector. That premium has nothing to do with production scale or engine technology.

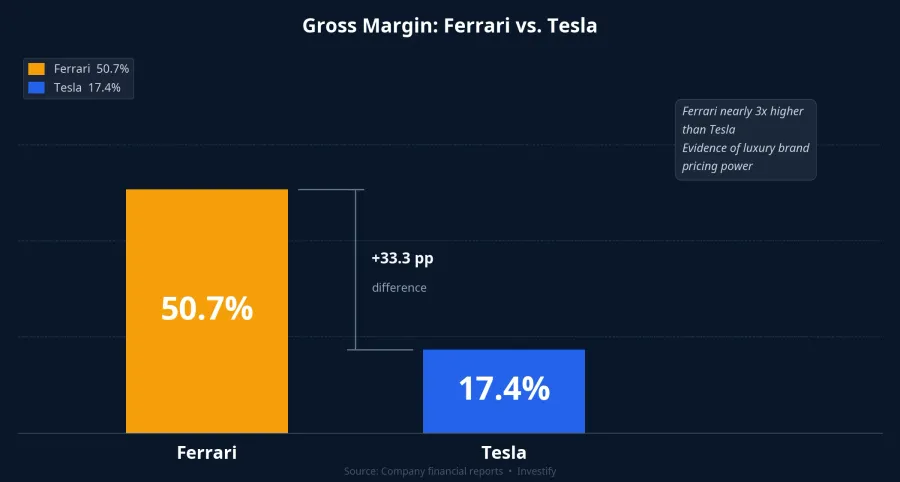

The margin structure tells the same story. Ferrari's gross margin stands at 50.7%, against Tesla's 17.4%. Ferrari retains more than half of every euro in revenue after subtracting the cost of goods. That is nearly three times Tesla's rate.Nasdaq Ferrari's operating margin runs at approximately 29%.

These numbers do not come from technology. They come from brand. The market prices RACE the way it prices Hermès or LVMH, not the way it prices Toyota or Volkswagen. The premium over the industry P/E is what investors pay for intangibles: deliberate scarcity (Ferrari intentionally produces below demand to protect pricing power), an identity inseparable from combustion sound and racing heritage, and a 90-year legacy that cannot be manufactured in a competitor's factory. That is the actual value-creation machine. Not the car, not the horsepower figures.

When "Looks Like a Mainstream Car" Becomes a Valuation Risk

With that framework in mind, the criticism that the Luce "looks like a Tesla" reveals its full weight. For a conventional automaker, a modern and practical design language is a selling point. For Ferrari, any resemblance to mass-market vehicles is a direct attack on the most valuable thing the brand owns: the perception of absolute, irreplaceable exclusivity.

Ferrari's elevated P/E is built on the belief that the company stands completely apart and cannot be replicated. When its first electric car invites comparisons to a mainstream sedan, it seeds market-wide doubt that the "differentness" is being diluted. Crucially, this doubt is enough to compress the valuation even before Ferrari has delivered a single Luce. The market did not sell because it feared weak unit volumes (deliveries are not scheduled until Q4 2026). It sold because the brand-equity component of the valuation formula appeared to wobble on launch day itself.

This highlights a particular risk category for luxury brand equities: the danger is not a product that fails commercially, but a product that succeeds technically while diluting identity. The Luce may well be an extraordinary automobile on any engineering measure. But if buyers and collectors no longer feel the absolute distinction from everyday transport, a P/E of 33 times becomes difficult to sustain.

Three Forces Behind the Sell-Off

It would be inaccurate to attribute the full 6% decline to a single cause. At least three forces converged in that session.

The first was profit-taking. RACE shares had risen meaningfully in the run-up to the launch, and a segment of investors followed the classic "buy the rumor, sell the news" pattern once the announcement was made public. The second was the broader context of the luxury EV segment slowing down. Both Porsche and Lamborghini have been pulling back or stretching out their electrification timelines due to weaker-than-expected demand, which made the market skeptical about a hyper-expensive EV with no established demand evidence. The third factor was Ferrari's own stated ambition: the company has lowered its target for fully electric vehicles to approximately 20% of its lineup by 2030, signaling that the electrification road will be gradual and capital-intensive.

That said, the center of gravity in the market reaction was clearly the identity question. Both sell-side analysts and social media commentators locked onto exterior design, not margin trajectories or revenue roadmaps. Profit-taking and sector headwinds amplified a sell-off that was fundamentally driven by one question: does this car still feel like a Ferrari?

The Porsche Taycan Contrast

Ferrari's situation looks sharply different when set against how Porsche entered the EV space with the Taycan in 2019. The Taycan was positioned as a natural extension of Porsche's performance DNA: the same driving philosophy, the same instantly recognizable sporting proportions. Its launch raised no questions about whether Porsche was abandoning its identity. The result was a car that was well received from day one and quickly became one of the best-selling models in the brand's lineup within its first few quarters.

Both moves were transitions to electric. But the Taycan reinforced Porsche's identity while the Luce placed Ferrari's identity in question. This is the core distinction for investors: technological innovation is not always a positive signal for the stock. What matters is whether the innovation serves or disrupts the engine currently generating value for the business. A transformation only deserves a positive re-rating when it extends the core competitive advantage, not when it calls that advantage into question.

The principle applies well beyond Ferrari. Any stock that trades at a premium because of brand, scarcity positioning, or durable competitive advantage faces the same test whenever management announces a major strategic shift. Before passing judgment on such transitions, investors should ask: is the part of the business I am paying a premium for still intact after this change?

What to Watch for RACE

For RACE specifically, the key question over the coming quarters is not whether the Luce is technically impressive (on an engineering level, it clearly is). The question is whether Ferrari can preserve scarcity, pricing power, and collector appeal as it moves into electric vehicles.

Two concrete signals are worth watching. First, the state of the Luce order book when deliveries begin in Q4 2026: a long waiting list at full asking price would be compelling evidence that Ferrari's identity premium remains intact in the eyes of qualified buyers. Second, the response of the classic Ferrari market at auction: if prices for combustion-engine models rise sharply after the Luce launch, it may signal that collectors are re-pricing pre-EV Ferrari heritage as scarcer and more desirable by contrast.

Ferrari's Q4 2026 earnings report will provide the first meaningful data point. Only then will investors have enough evidence to determine whether the Luce represents the successful evolution of a brand that knows how to adapt, or the opening of a longer-term dilution story the market is beginning to price in today.