Ask any retail investor what "corporate bonds" bring to mind, and the answer almost always leads back to 2022: Tan Hoang Minh, Van Thinh Phat, and high-yielding real estate bonds that ended in default. That caution is not unreasonable. Even in Q1/2026, real estate still accounted for 60–61% of total issuance value across the whole market, and interest rates on bonds from some property developers were still reaching 12.5% per year.Thanh Nien

But if retail investors dismiss the entire market based on that memory alone, they are missing a structural shift that has already happened in May 2026. The real picture looks nothing like what the label "corporate bonds" implies.

Two Doors Into the Market: Which One Can You Actually Use?

Think of Vietnam's corporate bond market as a building with two different entrances. The first is the private placement channel: only professional securities investors may enter, specifically those whose listed portfolio has stayed above VND 2 billion for at least 180 consecutive days. This is the arena for large institutions, investment funds, and high-net-worth individuals.

The second is the public offering channel: ordinary retail investors can participate with a minimum denomination of just VND 100,000. This is the only door most people can actually use.

The 2022 trauma is tied mainly to the private placement channel, where real estate developers issued bonds aggressively at inflated yields. But the channel that retail investors can actually reach, the public offering channel, is operating in a very different way.

May 2026: The Public Channel Is Almost Entirely Banks

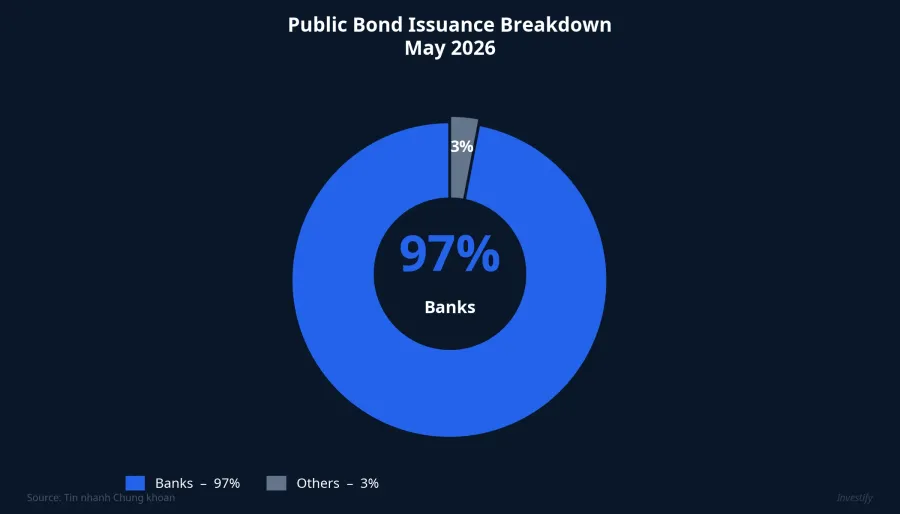

In May 2026, roughly 97% of the value issued through the public offering channel belongs to banks.Tin nhanh Chung khoan Looking at the full market, banks have also claimed around 70% of total new issuance for the month, a marked turnaround from Q1 when the group held only approximately 28.5%.

The list of issuers makes this shift concrete. Just in the first weeks of May, MB issued VND 3,500 billion, Bac A Bank VND 3,000 billion, Techcombank VND 2,000 billion, MSB approximately VND 1,000 billion, alongside VPBank, Nam A Bank, and others.Phu nu Viet Nam Two of the large state-owned banks joined as well: Agribank announced plans to issue up to VND 15,000 billion to the public, with a 10-year tenor, floating interest rate, and Tier 2 capital treatment.Doanh nghiep va Hoi nhap

Put simply, the "corporate bonds" that retail investors can actually buy in May 2026 are overwhelmingly bank bonds.

Why Are Banks Paying 8 to 8.9%?

The instinctive reaction from many investors is: "That yield is high — the bank must be in trouble." This is one of the most common misconceptions. Banks offering 8–8.9% per year, about 2–3 percentage points above last year's levels,Phu nu Viet Nam are not doing so because they are short on cash. They need long-term capital to balance their balance sheet structure.

Here is a simple way to understand it: banks take in short-term deposits and lend them out at long tenors. Most deposits mature in 6–12 months, while loans can run 5–10 years. That maturity mismatch creates risk. Issuing long-term bonds is a way to close that gap.

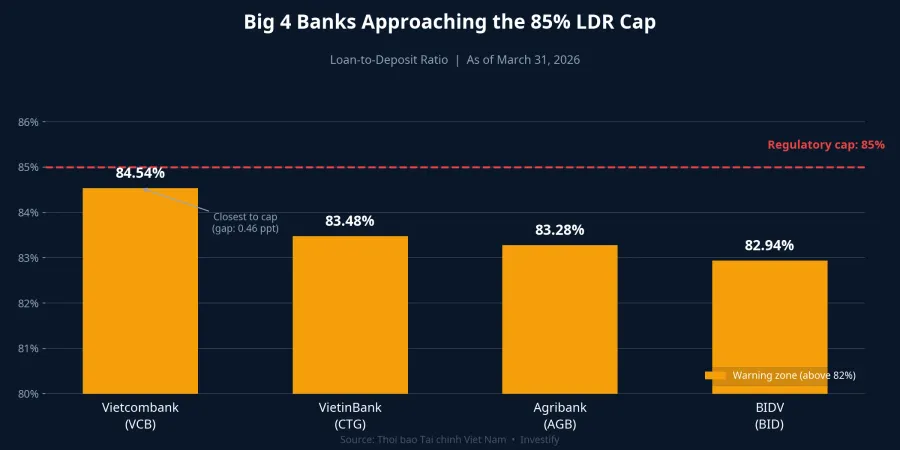

The underlying numbers illustrate the pressure. As of end-April 2026, total system-wide credit outstanding exceeded VND 19,400 trillion (VND 19.4 quadrillion), up 4.42% from end-2025 and up 18.26% year-on-year.Vietstock Deposit growth has not kept pace, widening the gap between credit and deposits to approximately VND 1,400 trillion, equivalent to 7.22% of total outstanding credit.Thoi bao Tai chinh Viet Nam

The direct consequence: the loan-to-deposit ratio (LDR) at Vietnam's largest banks is approaching the 85% regulatory ceiling. As of March 31, 2026, Vietcombank stood at 84.54%, VietinBank at 83.48%, Agribank at 83.28%, and BIDV at 82.94%. All four are in the warning zone.Thoi bao Tai chinh Viet Nam

Issuing 7-to-10-year bonds solves this structural challenge: it adds Tier 2 capital to give LDR more room and lengthens the average funding tenor. Paying 8–8.9% is the price of that structural capital pressure, not a sign of impending insolvency.

Two Market Segments: Completely Different Stories and Risks

When you pull the market apart, what you find in May 2026 is two segments operating almost independently of each other.

Segment one is bank bonds via public offering. Buyers are ordinary retail investors, minimum denomination VND 100,000. The issuers are regulated and supervised by the State Bank of Vietnam, disclosure is transparent, and yields run around 8–8.9% per year. This is the segment expanding in May.

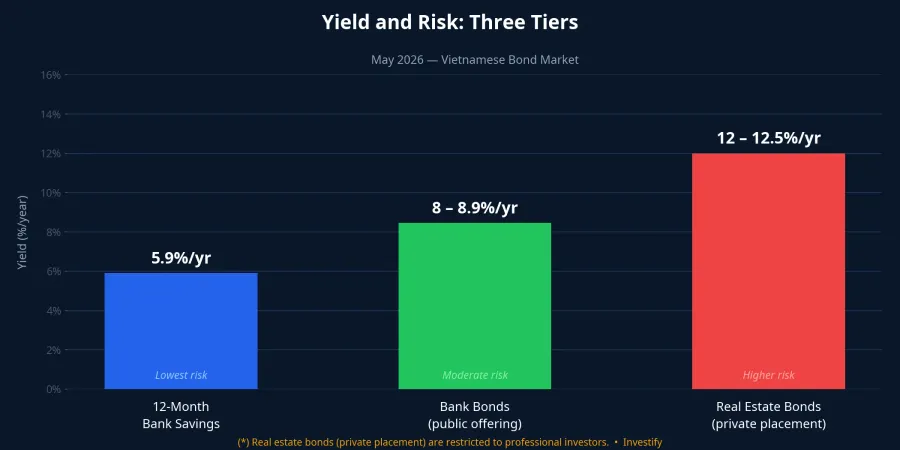

Segment two is real estate bonds via private placement. Only professional investors may participate. Average yields run around 12% per year with a peak of 12.5%,Nhip cau Dau tu mostly used to roll over existing debt coming due, carrying clear refinancing risk. This is the segment tied to 2022 memories, and it is also the segment retail investors cannot access.

The belief that "corporate bonds equal real estate risk" is still partially accurate for segment two. But it has become outdated for the only segment retail investors can actually reach. The problem is that most people lump both together.

The Real Trade-offs to Understand

Set bank public offering bonds (8–8.9%/year) alongside the 12-month deposit rate at Vietnam's Big 4 banks, currently around 5.9% per year,Kenh14 and the yield gap of roughly three percentage points is worth considering. But higher yield always comes with something in exchange, and that is the most important thing to understand before deciding.

There are three specific trade-offs. First, many of these bank bonds qualify as Tier 2 capital, meaning they have a lower repayment priority than ordinary deposits in the event the bank encounters difficulties. Second, tenors are typically 7 to 10 years, and some tranches carry floating interest rates, so their effective return may vary with the rate environment. Third, selling before maturity depends on secondary market liquidity, which remains shallow in Vietnam.

In short, this is an alternative yield channel relative to savings deposits, with clear trade-offs around repayment priority, long tenor, and secondary market liquidity. Not a trap. Not risk-free. But an entirely different situation from what happened in 2022.

Read Each Segment Correctly, Not the Whole Market

Vietnam's corporate bond market in May 2026 is no longer a single, homogeneous block of risk. The portion accessible to retail investors this month is primarily bank bonds, driven by the banking system's own structural need for long-term capital. The real estate portion still exists, still offers high yields, but sits in a separate channel with a separate investor eligibility requirement.

For investors seeking yield above savings deposits while keeping their money with a tightly supervised institution, bank public offering bonds deserve to be evaluated on their own terms. Not because they are risk-free, but because their risks — repayment priority, tenor, and liquidity — are entirely different from the risks that define 2022. Reading each segment correctly, rather than avoiding the whole market, is the smarter approach to this opportunity.

Two signals worth watching over the coming weeks: whether deposit growth catches up with credit growth (which would ease LDR pressure), and at what yield levels Agribank's planned VND 15,000 billion public offering is absorbed by the market.