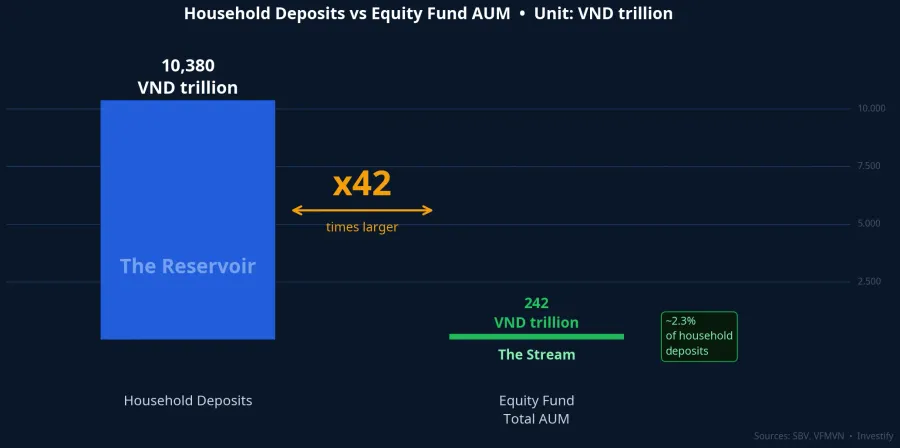

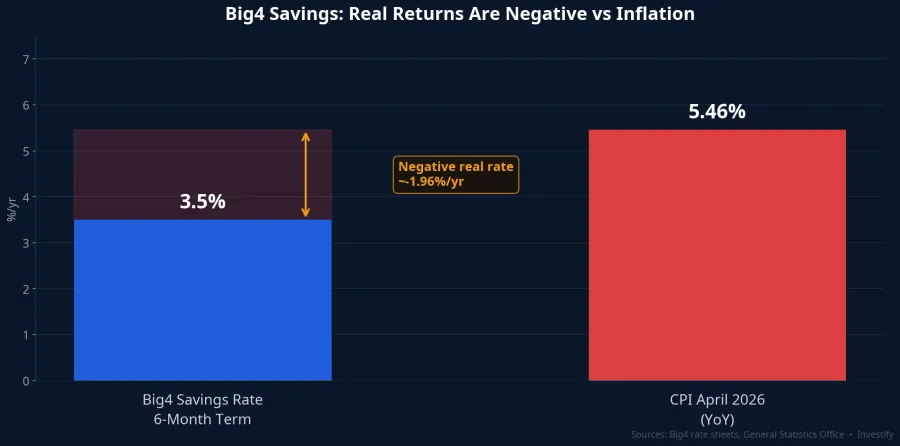

By the end of January 2026, total household deposits in the Vietnamese banking system had surpassed VND 10,380 trillion, the highest level ever recorded.VietnamNet To put that in perspective, the figure is roughly 43 times the combined assets of all equity funds currently operating in Vietnam. At the same time, the six-month savings rate at Vietnam's Big 4 state-owned banks was sitting at 3.5% per annum, while April CPI rose 5.46% year-on-year.VTV Put simply: each year, money sitting in a bank account is losing close to 2% of its real purchasing power.

Depositors know this. So why aren't they withdrawing?

The answer lies in behaviour, not in interest rates. There are three layers of reasons, each deeper than the last.

A Real Record, But Growth Has Slowed Sharply

Before diving into the psychology, it is worth reading the headline figure carefully. "Highest ever" describes the total stock of money sitting in banks, not the rate at which new money is flowing in.

In reality, household deposits at end-January were up just 0.45% compared to end-2025.Tuổi Trẻ Moving into Q1, total customer deposits across 27 listed banks grew by only about 0.26%, while outstanding loan balances expanded 3.47%.BáoMoi A dozen banks even recorded an outright decline in deposits during the quarter. Meanwhile, deposits from corporate entities fell 1.62%, dropping to just over VND 6,000 trillion.VietnamNet

The accurate picture is not a surge of new money rushing into banks, but a pool accumulated over many years that is now growing very slowly. The right question is not "why is money still flowing in" but "why won't the existing pool flow out."

Layer One: Saving Is the Default

The strongest layer, and also the hardest to see, is generational inertia. For most Vietnamese households, putting money in a savings account is not a considered investment decision. It is simply where money goes when there is nothing else to do with it. Savings deposits are the multigenerational default: safe, familiar, requiring no new knowledge.

The weight of this inertia shows up in a striking statistic: nearly half of all idle cash held by Vietnamese households is still kept at home, not channelled into any income-generating instrument at all.VNBusiness When a large share of household money has not even made the short journey from a home safe into a bank account, expecting it to leap directly into a mutual fund or equities is asking for a step too far.

Bank deposits have inadvertently become the "first step forward" in many families' financial journeys, and for a significant number, it is also the last. This inertia is not irrational. It reflects decades during which a savings account was both the safest option available and the most accessible one.

Layer Two: Fear of Loss Outweighs Fear of Missing Out

Depositors know they are underperforming inflation, but the loss is invisible and arrives gradually in small instalments. The risk of losing capital in stocks or funds, by contrast, is visible and emotionally far more painful. This is loss aversion: behavioural research consistently finds that losing one unit of value causes more psychological pain than gaining the same unit brings pleasure.

Market memories reinforce the fear. The sharp volatility and corporate bond defaults of 2022 are still vivid for many investors. Even when conditions are favourable, picking the right fund is not straightforward: in April, while 81 of 83 equity funds reported positive returns, only a handful actually outperformed the VN-Index benchmark.BáoMoi The message retail savers take away is simple: if even the professionals struggle to beat the market, why take the risk?

Together, the first two layers produce a strange equilibrium: savers accept losing 2% of purchasing power each year but are unwilling to tolerate even a temporary paper loss in an investment portfolio. Psychologically this is coherent, even if numerically it makes little sense.

Layer Three: Emergency Funds Need Instant Access

The third layer is the most straightforward. Savings deposits can be withdrawn almost immediately; at worst, the depositor forfeits the accrued interest by breaking the term. Other investment channels require planning ahead: open-ended fund units typically take three to five business days to settle after redemption, and the value can fluctuate while the investor waits.

For a household that needs a liquidity buffer for school fees, medical costs or an unexpected opportunity, the ability to withdraw instantly is worth more than a few extra percentage points of expected return. This is the most defensible of the three layers, and it explains why some portion of household deposits will always stay in a bank account, regardless of how deeply negative the real rate becomes.

The three layers are not equal in strength. Inertia is the dominant force because it prevents most depositors from asking the question of whether to move at all. The other two layers add weight for those who have already asked the question but still hesitate.

A Small Stream Is Beginning to Flow

Is any money actually moving? Yes, and open-ended mutual funds are the most visible destination.

In April, total net asset value across the fund industry reached over VND 259,000 billion, up 3.7%, with equity funds alone accounting for VND 242,000 billion, up 4.6%.VnEconomy More significant than the market-driven gain was new money: open-ended funds recorded a net inflow of over VND 749 billion, the second consecutive month of positive flows, with 24 of 36 equity funds increasing deployment. Fund distribution platforms are also seeing strong growth in user numbers, tracking toward the industry's stated goal of reaching 5 million fund certificate investors.VietnamBiz

Context matters here, however. The entire VND 242,000 billion in equity fund assets represents only about 2.3% of household deposits. Monthly net inflows of VND 749 billion, placed next to VND 10,380 trillion sitting in banks, are a fraction of a fraction. The shift is real; the scale remains tiny.

What makes open-ended funds a plausible first step is that they partially address all three barriers: buying through an app for a few hundred thousand dong is no harder than opening a savings account, portfolio selection is delegated to a professional manager (reducing the fear of picking wrong), and liquidity, while slower than a bank withdrawal, is still far more flexible than real estate or individually traded corporate bonds.

Signals to Watch

The portion of savings earmarked as an emergency buffer should stay in the bank. No investment channel can replace that function. The remainder, quietly losing purchasing power each year, is where it makes sense to consider a higher-expected-return alternative.

The signal worth watching over the coming months is the combination of two trends: if open-ended fund net inflows sustain positive momentum into a third and fourth consecutive month while household deposit growth continues to stagnate, that will be the first concrete evidence that the VND 10,380 trillion pool is genuinely starting to move rather than simply sitting still. The current market backdrop does not work against this scenario: the VN-Index closed on 25 May at 1,886.03 points, not far from the all-time high of 1,927.94 points set on 18 May.

The story of VND 10,380 trillion parked in Vietnamese banks is ultimately not a story about interest rates. It is a story about behaviour. And behaviour changes slowly — but it does change.