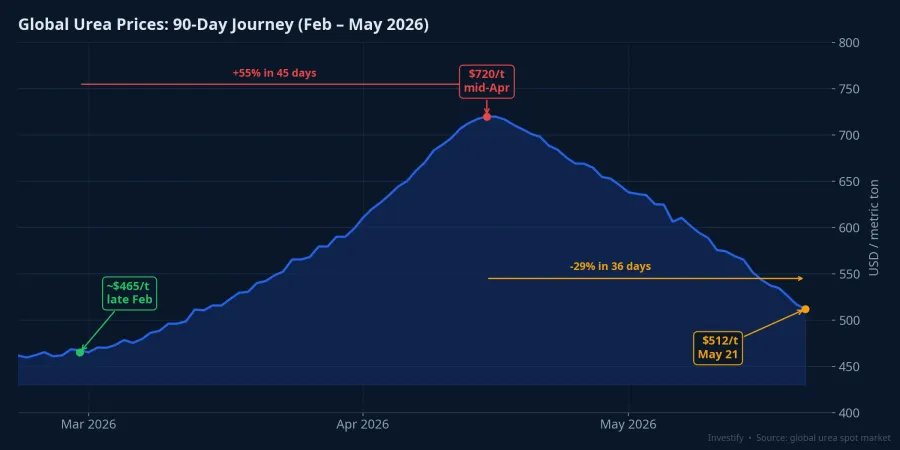

Three months were enough for global urea prices to complete a full cycle: from roughly $465 per metric ton in late February, up to $720 in mid-April, then back down to $512 on May 21. That journey was not just a commodities story. It shaped the strongest Q1 results in years for Vietnam's two major urea producers, DPM and DCM. Almost immediately after, the same move pulled both stocks lower in tandem. The striking detail is in the recent decline: urea lost 27% in a single month while the supply bottleneck remained entirely unresolved.

A 35-km Chokepoint and a 55% Move in 45 Days

Hormuz is the narrowest passage on the shipping lane connecting the Persian Gulf to the rest of the world. According to CNBC, roughly one-third of global fertilizer trade passes through the strait, with urea representing a substantial share.CNBC When conflict broke out in Iran on February 28, 2026, and the strait effectively closed, markets immediately repriced available supply. On March 2, urea jumped 14.18% in a single session, then added another 11% the following day. The rally sustained into mid-April before peaking at $720.25 per ton on April 15, a gain of nearly 55% from the late-February level in just 45 days.

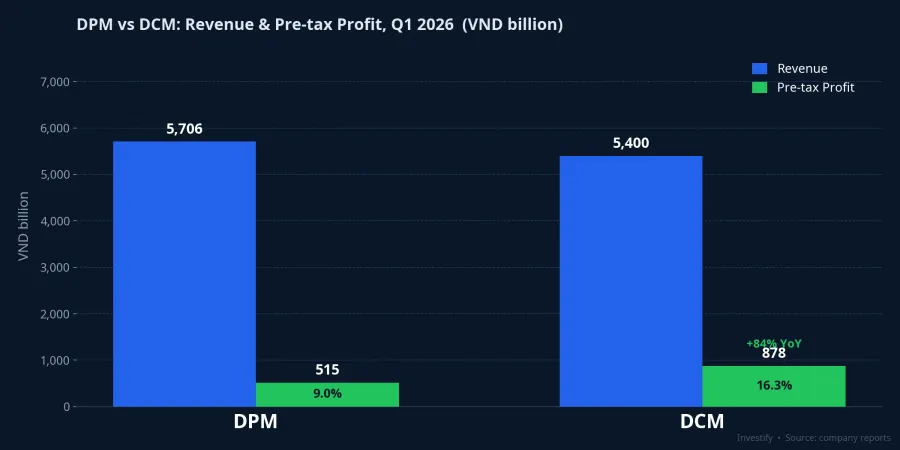

That price window was exactly what both DPM and DCM captured. The entire first quarter of 2026 coincided with the urea price climb. DPM reported revenue of VND 5,706 billion and pre-tax profit (PBT) of VND 515 billion, achieving 150% of its quarterly plan.CafeF DCM's profit performance was even more impressive. Revenue came in at approximately VND 5,400 billion, but PBT reached VND 878 billion, up 84% year-on-year.Fili

Both companies benefited from the same price environment, yet DCM's profitability significantly outpaced DPM despite comparable revenues. The numbers tell the story: DCM's PBT margin reached 16.3%, nearly double DPM's 9.0%. The gap reflects a different sales mix: DCM carried a higher share of export volumes and re-sold imported fertilizer priced at elevated global rates, both of which amplified gross profit during the price surge.

The 27% Drop: Demand Walked Away, Supply Stayed Stuck

By May, the narrative reversed. Urea fell from its peak to $512.50 per ton on May 21, down roughly 29% from the mid-April high. On May 21 alone, the price shed 8.48% in a single session.

What matters here is not the size of the decline, but the reason for it. Hormuz is still closed. Per Argus data cited by farmdoc at the University of Illinois, at least 27 vessels carrying 1.24 million metric tons of urea are anchored in the Persian Gulf, waiting for the strait to reopen before they can deliver.Farmdoc Supply on paper remains tight, yet prices reversed. So what pulled them down?

The answer is on the demand side. Brazil, one of the world's largest importers of nitrogen fertilizer, refused to buy at elevated prices and pivoted to ammonium sulphate (amsul), a cheaper substitute. Amsul imports into Brazil exceeded urea for the first time in many years.World Fertilizer China also failed to enter the market as analysts had expected, held back by elevated domestic inventory and a peak agricultural season that had already passed.ChemAnalyst

Two major demand anchors withdrew at the same time, at the same high price. The result: prices had to self-correct even though physical supply was still trapped in the Gulf.

The distinction matters. If prices drop because 1.24 million tons are released to the market, that signals a supply recovery, rational and expected. If prices drop because buyers walk away while goods remain stranded, that is a different and more dangerous state for sellers. The stockpile has not disappeared. It is waiting.

1.24 Million Tons: A Supply Overhang Waiting to Land

This is where the 90-day story remains open. When Hormuz reopens, 1.24 million tons of urea will flow into the market nearly simultaneously. Under normal demand conditions, that alone would pressure prices downward. Under current demand conditions, it is a clearly defined risk scenario.

Markets have already begun pricing in this possibility. Brent crude closed at $102.98 per barrel on May 22, down 5.7% on the week, reflecting expectations that the strait could soon reopen. The same logic that applies to oil applies to urea: if Hormuz opens, the resulting supply wave would arrive on top of a demand base that is already weak, creating a double-sided pressure.

Not every segment of the fertilizer chain is cooling off, however. Sulfur, the key raw material for phosphate fertilizers and DAP, rose to CNY 7,550 per ton on May 22, up roughly 16% from the start of the month. Middle East shipping disruptions are tightening sulfur supply through a different channel. The picture is uneven: the nitrogen segment is softening on weak demand, while the phosphate segment continues to face cost pressures from supply constraints.

DPM, DCM: Stocks Already Pricing the Scenario

For Vietnam, Hormuz's impact on DPM and DCM flows through the world price channel, not through direct trade. Iran is not a meaningful urea import source for Vietnam due to payment barriers and sanctions. But when international urea prices rise, margins at both producers expand. When prices correct, that window narrows.

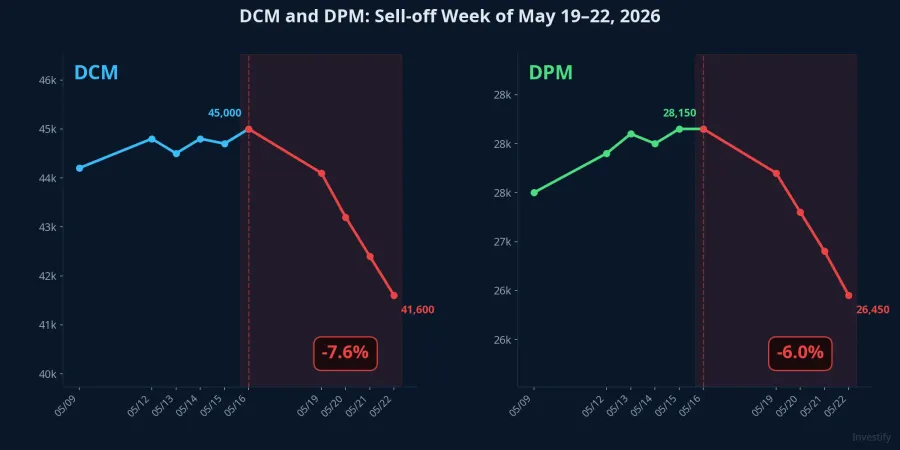

Equity markets moved ahead of the news. During the week of May 18–22, as urea prices slid sharply, DCM fell from VND 45,000 to VND 41,600, a decline of roughly 7.6%. DPM dropped from VND 28,150 to VND 26,450, down approximately 6.0%.

Both stocks pulled back from their recent highs almost in lockstep with the urea price decline. The market's signal is clear: the profit wave driven by elevated urea prices may have passed its peak.

This does not mean either company is in difficulty. DCM holds approximately 40% of the domestic urea market and would still benefit if prices stabilize at a reasonable level through the second half of the year.Fili But the year-on-year comparison base from Q2 onward is now significantly elevated. For domestic farmers, the dynamic runs in reverse: if Hormuz reopens and urea prices continue easing, input costs for second-half crop cycles should soften after following global prices higher throughout Q1.

Two Variables That Will Define the Second Half

The relevant signal is no longer Q1 earnings. Those results are clear and have been absorbed by markets. Two more important variables lie ahead.

The first: when Hormuz reopens and how quickly 1.24 million tons flows out. If that supply hits the market while demand has not yet recovered, a second price correction — this time supply-driven — is a well-grounded scenario. The second: whether Brazil and China return as buyers. If those two demand anchors come back, they could absorb a meaningful share of the released supply and hold prices at a level that works for producers. If demand stays weak, the current $512 per ton floor may not hold.

H2 2026 profitability at DPM and DCM will be determined by these two variables, not by the strong Q1 results already recorded. The Q1 numbers confirm that both companies captured the opportunity when the high-price window opened. Whether the price floor holds long enough for the second half to sustain that momentum, or whether the release of 1.24 million tons writes a new chapter in this 90-day price cycle, depends on forces still unresolved.

This article is informational analysis only and does not constitute investment advice.