On the morning of May 25, 2026, Vinhomes launched a program allowing homebuyers to use gold as payment, along with a headline guarantee: after 5 years, if you no longer want to keep the property, you get back 110% of the original converted value of your gold.CafeF On the surface, 110% sounds attractive, like buying a home and pocketing a 10% bonus. But break it down simply: spread that 10% total over 5 years, and you're looking at roughly 2% per year on a simple interest basis. Meanwhile, a large commercial bank is currently paying 5.9% to 6% per year on savings deposits.

So what is this program actually offering, and where does its real value lie?

When 110% Equals Just 2% per Year

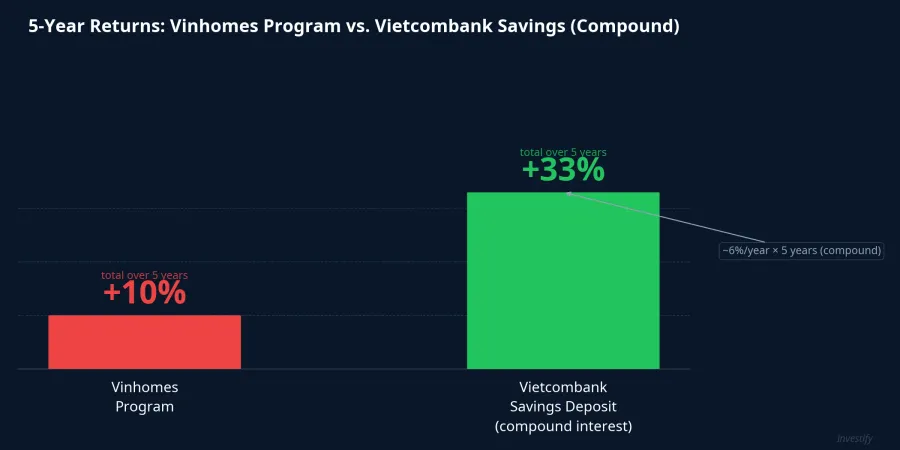

Start with the simplest arithmetic. Say you convert gold worth VND 100 million and use it to buy a home under this program. After 5 years, if you choose to exit, you receive VND 110 million. That is VND 10 million in gains over the full 5 years, roughly 2% per year on a simple interest basis.

Put that beside a standard savings account. Vietcombank currently offers 5.9% per year on 12-month deposits and 6% per year on 24-month deposits.VietnamBiz BIDV is likewise at 6% per year across 24- to 36-month tenors.VietnamBiz If you deposited VND 100 million at Vietcombank and rolled over a 12-month term at 5.9%, compound interest over 5 years would accumulate to roughly 33%, more than three times the 10% Vinhomes is offering.

Vietnam's largest real estate developer did not accidentally design a financial product that underperforms a savings account by that margin. This is the first signal that 110% is not a yield reward. It is something else entirely, and understanding exactly what it is will change how you evaluate the program.

What You're Actually Buying: A Price Floor

Think of it this way: the program is not selling you an interest rate. It is selling you insurance against falling property prices.

The structure works like this. You buy a home today and simultaneously receive an option exercisable in year five. If after 5 years the property has appreciated beyond the gold value you put in, you keep the home and capture that upside. If prices have stagnated or declined, you can exit and receive 110% of the original converted gold value. Vinhomes absorbs the downside risk on your behalf: whatever the market does over 5 years, you are guaranteed a cash floor.

What you pay for that floor is the yield you give up. Instead of earning 5.9% per year in a savings account, you receive around 2% per year. That is roughly 4 percentage points per year sacrificed, which compounds to nearly 20% of your original principal over 5 years. That 20% is the cost of the downside insurance: not an arbitrary loss, but the explicit price of the protection.

There is a second important mechanism in the floor that is easy to miss. Under the most widely-reported interpretation, the 110% is calculated on the original converted gold value at the time of purchase, not on the gold price at the time of repayment. SJC gold bars are currently trading around VND 163.5 million per tael and reached nearly VND 169 million per tael in late April.Vietnam.vn If gold continues to rise over the next 5 years and you choose to exit the program, you would receive 110% of the old fixed figure, not a quantity of gold valued at the then-current price. That is a second trade-off that belongs in your calculation.

It is worth noting that Vinhomes has not yet released the full official terms governing the 110% formula. Reading the contract carefully before committing is mandatory, because that single clause determines the entire financial equation for participants.

Why Vinhomes Wants Your Gold

From the developer's perspective, the picture is considerably brighter.

The World Gold Council (WGC) estimates Vietnamese households hold approximately 400 to 500 tonnes of gold, equivalent to USD 35 to 40 billion, or close to 8% of GDP.Dân Trí The WGC itself notes the 500-tonne figure is dated and difficult to verify precisely, but the scale of gold savings held by Vietnamese households is undeniably large by any measure. Most of it sits in home safes, entirely outside the financial system.

With this program, Vinhomes taps directly into that stockpile and redirects it into the real estate market without going through bank credit. For every transaction, the developer faces two outcomes, and both are favorable. If the buyer keeps the home, that is a completed sale and the 110% obligation terminates. If the buyer exits, Vinhomes has effectively borrowed that capital for 5 years at roughly 2% per year, significantly cheaper than issuing corporate bonds or drawing bank loans.

This all fits the company's stated financial target: VND 60,000 billion in net profit for 2026, the highest in the company's history and a 38% increase over the prior year.CafeF Hitting that target requires a strong sales wave. The gold program follows an earlier 0% to 6% interest rate support package launched in April,Tuổi Trẻ reflecting an aggressive and sustained sales strategy. VHM shares closed at VND 153,800 on May 22, down 3.75% from the previous session, suggesting that market sentiment remains under pressure even as stimulus policies roll out in quick succession.

The gold program should not be read as a straightforward sales promotion. It is a hybrid financial product: simultaneously a tool to unlock real estate demand and a cheap funding vehicle, designed for a company racing toward a record profit target.

Who This Program Actually Fits

Once you understand the structure correctly, the question shifts. It is no longer simply whether 2% per year is worth it. The real question becomes: is the downside protection floor worth the 20% opportunity cost you are giving up?

The ideal candidate is someone who already intends to buy a specific Vinhomes property, currently holds idle gold, and values minimum price protection more than savings yields or gold appreciation potential. For anyone primarily seeking a return on savings, a bank deposit still wins by a wide margin. For anyone holding gold because of its long-term price trajectory, joining this program means locking in today's gold value and surrendering future upside.

The deciding variable comes down to one question: over the next 5 years, will Vinhomes property prices rise enough to offset both the foregone savings interest and the foregone gold appreciation? If yes, keeping the home is the winning outcome and the 110% floor is just a backup you never need. If you are uncertain, that floor is the only thing in the package with genuine value.

The most important signal to watch for is the official terms document when Vinhomes publishes it fully: whether the 110% is calculated on the original converted gold value or on the gold price at the time of repayment. That one clause completely changes the financial calculus, and as of the time of writing, it has not been officially confirmed.