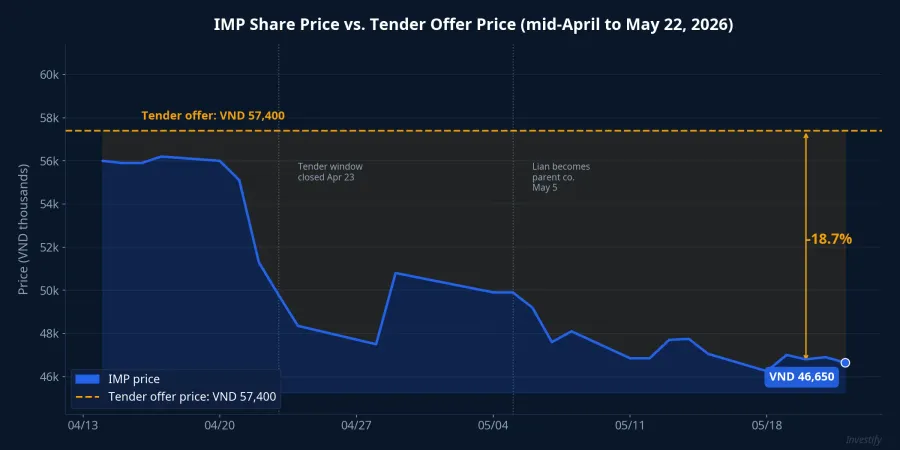

In early May 2026, Lian SGP Holding, a subsidiary of Chinese pharmaceutical group Livzon, completed its purchase of 104.5 million IMP shares — equivalent to a 67.87% stake in Imexpharm — at a tender offer price of VND 57,400 per share. The total transaction value was approximately VND 6,000 billion, making it the largest M&A deal in Vietnam's pharmaceutical sector this year.VnEconomy

Yet by the close of trading on May 22, IMP was sitting at just VND 46,650, some VND 10,750 (18.73%) below what Lian had paid. The VND 6,000 billion acquisition now carries a market value of roughly VND 4,875 billion. Per VnBusiness, Lian's paper loss on the position is approximately VND 1,100 billion.VnBusiness

For many new investors, news of a "high-price takeover" reads like a green light to buy. Imexpharm's story shows why that instinct can lead to poorly timed entries. The lesson lies in a distinction that often gets overlooked: two very different things are bundled inside every M&A deal, and conflating them is where mistakes happen.

How Long Does a Tender Offer Price Last?

The most common point of confusion is the phrase "public tender offer." This is a time-bound transaction: Lian registered to buy up to 120 million IMP shares at VND 57,400, with the window open only from early April through April 23, 2026.Vietstock During that window, Lian collected 104.5 million shares from 109 selling investors.

Think of the tender offer price as a dated voucher. Shareholders who held IMP before April 23 and chose to sell received VND 57,400 per share. Once the date passed, the voucher expired. Anyone who buys IMP after that point transacts at the prevailing market price, with no special rate on offer.

The market confirmed this quickly. On April 22, as the window was about to close, IMP fell 6.90% to VND 51,300. By May 5, when Lian formally became the parent company, the share price had already slipped to VND 49,900. The VND 57,400 level was never a price floor that would hold the stock up after the deal closed. It existed precisely for the duration of that one transaction, nothing more.

You're Not Buying What Lian Bought

The next natural question is: why would Lian pay VND 57,400 when the market was only pricing IMP around VND 50,000 at the same time? The answer is that the two parties were buying entirely different things.

Lian was not buying a block of shares to flip for a quick gain. Lian was acquiring control of an EU-GMP-certified antibiotic manufacturing platform, along with an established distribution network and a strong position in Vietnam's hospital tender channel. The premium above the market price is what finance professionals call a control premium: the extra amount a strategic buyer is willing to pay for the right to run the company, not merely to own a small stake in it.

A retail investor buying a few hundred IMP shares on the exchange has none of those rights. Without control, there is no reason to pay the price of control. The 18.73% gap between what a controlling acquirer paid and what the market offers for a minority position is entirely normal in any acquisition. It is not a signal that the deal was overpriced, or that the stock is unusually cheap.

Post-Deal: Concentrated Ownership, Almost No Liquidity

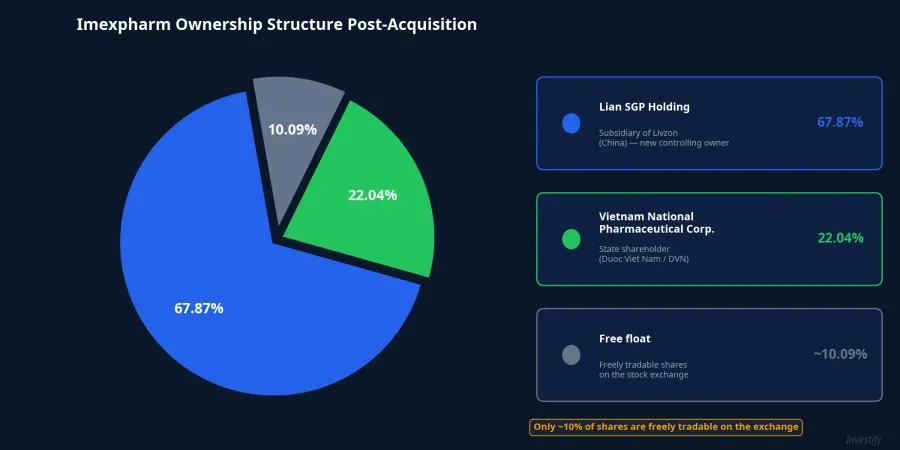

After the transaction closed, IMP's ownership became heavily concentrated in two large shareholders. Lian holds 67.87% and Vietnam National Pharmaceutical Corporation holds 22.04%.DNSE Together they account for roughly 90% of the outstanding shares, leaving a free float of only around 10%.

The consequence shows up immediately on the trading screen. Recent sessions have seen IMP match only a few thousand shares per day. On May 22, only 6,700 units changed hands. When the freely traded supply is this thin and there is no large institutional buyer propping up the price, even modest sell orders can push the stock down significantly. This is why post-acquisition shares often struggle to reclaim the tender offer price: the buying that created that price has left, and liquidity has dried up.

For anyone who already holds the stock, this also matters for exit timing. With such thin volume, even a mid-sized sell order can result in meaningful slippage from the quoted price.

Business Fundamentals and the Governance Gap

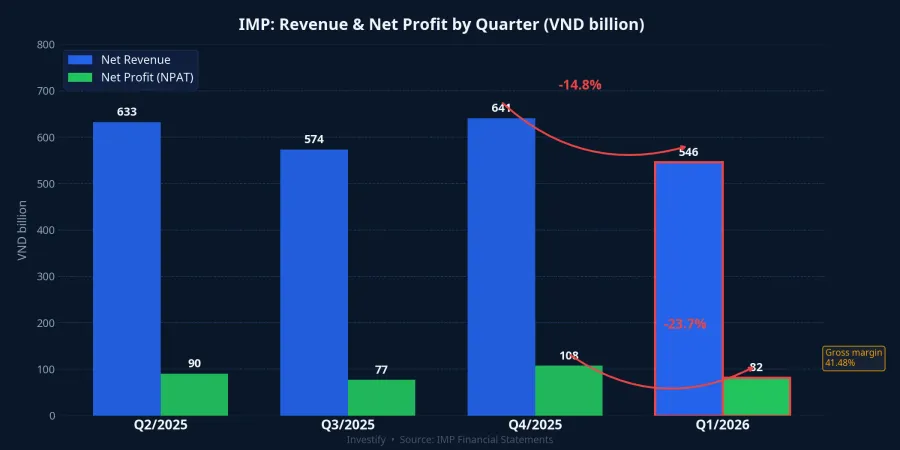

Imexpharm's underlying business is not in bad shape. In Q1 2026, the company posted net revenue of VND 546.21 billion and net profit of VND 82.02 billion, with a gross margin of 41.48%, still among the stronger readings in the domestic pharma sector. Compared with Q4 2025, however, revenue fell from VND 640.78 billion and profit declined from VND 107.49 billion, drops of approximately 14.8% and 23.7% respectively.

The market prices IMP on the basis of these earnings, not on the basis of what a foreign conglomerate was willing to pay for strategic control. These are two completely different valuation inputs, and conflating them is the most common mistake investors make when reading M&A news.

At the same time, the company is navigating a leadership transition following SK Group's exit. Three board members nominated by SK have submitted resignation letters: Chairman of the Board of Directors Woo Sungmin, Board Member Truong Minh Hung, and Independent Board Member Chung Suyong, all at Imexpharm (IMP).Vietstock An extraordinary general meeting will be held to fill the vacant seats.

A governance gap of this kind is a standard reason for investor caution. When leadership is unsettled and the new owner's strategic direction is not yet public, the market typically waits and watches before repricing the stock. This pattern holds for any company going through an ownership change.

What Lian's Paper Loss Actually Tells Us

The approximately VND 1,100 billion paper loss needs to be read in context. It is an unrealized loss based on the current market price, not a completed loss. Lian did not buy IMP to trade in and out over a few weeks. This is a long-term strategic acquisition, and the day-to-day share price on the exchange is almost certainly not the metric Lian is watching.

The fact that the acquirer was willing to pay 18.73% above the prevailing market price signals that they value Imexpharm's potential more highly than the market currently does. That is a constructive long-term signal about the new owner's expectations. But that signal belongs to a controlling shareholder with a multi-year horizon. It does not automatically translate into near-term gains for a retail investor buying shares on the open market today, and Lian's internal valuation should not be used as your own buy justification.

What to Watch Next

The IMP situation crystallizes a principle that often gets lost in the excitement of M&A headlines. The tender offer price was available only to sellers who acted within the tender window, which closed on April 23. Anyone who bought shares after that date transacts at market prices reflecting real operating fundamentals and the available float, not the control premium a strategic acquirer was prepared to pay.

For investors tracking IMP, the signals that genuinely matter are the outcome of the upcoming extraordinary general meeting: who replaces the three departing board members, and what strategic direction Lian sets for Imexpharm over the next three to five years. When governance and strategy become clearer, the market will have a real basis for repricing the stock.

For M&A news in general, the right question is not "how much did the buyer pay?" but rather "is that window still open, and what is holding the price up now that the deal is done?"