In investing, some reflexes form over years of observation and work remarkably well. One of them is: when commodity prices rise, buy stocks in that sector. You watch Brent crude climb and BSR, PLX surge with it. You see HRC steel recover and Hoa Phat's margins widen within the quarter. This reflex has a solid foundation and it works in many cases.

So when world rice prices rose more than 18% in a single month and Vietnam climbed to the top of the regional export price rankings, the question "which food stocks should I buy?" appeared naturally across every investing forum. It is a completely reasonable question. The problem is that if you apply the oil or steel price transmission mechanism directly to rice, you risk buying the wrong sector at exactly the moment the story is hottest. Rice operates on a different logic, and most of the reason lies in the structure of its value chain. The price level itself is secondary.

This article explains why, and where that reflex does actually work within the agricultural chain.

Vietnam Rice Is Genuinely Well-Positioned

First, let us be fair to the good news in this story. Vietnamese export rice prices are at elevated levels. According to the Vietnam Food Association, on May 22, Jasmine rice from Vietnam was being offered at $524–$528 per tonne, continuing a strong upward trend compared to early May.Vietnam.vn And per the global rice export price table published by the VFA on May 21, Vietnam held the most expensive position among major exporting countries.VFA

Vietnam maintains higher prices thanks to a mix weighted toward fragrant and premium varieties, consistent milling quality, and steady demand from the Philippines along with growing markets in Africa and the Middle East. This is good news for farmers and for the country's trade position. But from "strong international prices" to "listed companies earning more," there is a very long distance.

Spot Price and Realized Price Are Two Different Numbers

This is the key point that many new investors miss. The 18% surge in world rice prices is a spot market recovery over the past few weeks, following more than a year of declining prices. But Vietnamese rice exporters do not sell at the spot price every day.

Think of it this way: before a container of rice leaves port, the company has already signed a fixed-price contract one to three months earlier. The raw paddy was also purchased and stockpiled at the beginning of the crop season. When today's spot price jumps, the company's cost base and selling price are already locked in. Any profit from this price surge, if it holds until contracts are renegotiated, will not show up in financial statements for several quarters at the earliest.

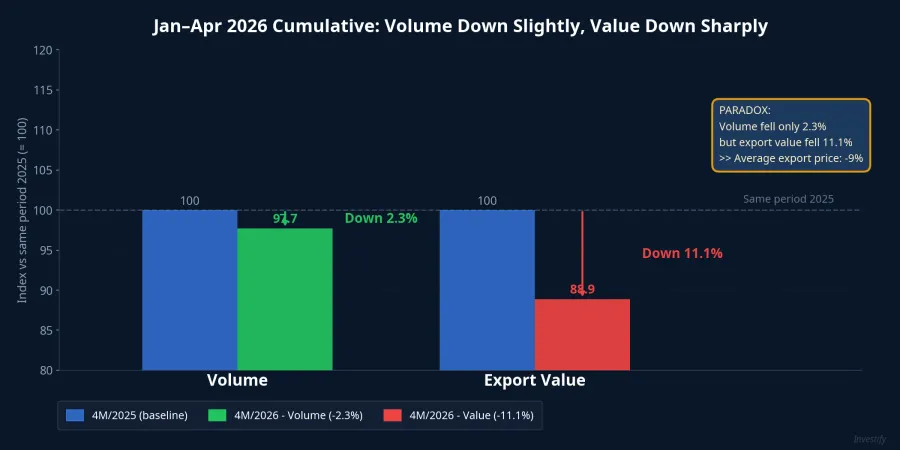

The clearest evidence sits right in the cumulative data. In the first four months of 2026, Vietnam exported approximately 3.37 million tonnes of rice, earning approximately USD 1.58 billion.BaoMoi Compared with the same period last year, volume fell only 2.3%, but export value fell 11.1%, equivalent to an average export price of approximately USD 468.4 per tonne, or 9% below the prior year.Dan Viet In other words, while headlines say "rice prices are rising," the average price that Vietnamese companies actually received across the first four months of the year was lower than last year.

The two figures do not contradict each other. One is today's spot price. One is the average realized price across many months when the market was still declining. Both are accurate, but only one determines corporate profitability.

What Food Stocks Said in May

If the "commodity prices up, stocks up" mechanism applied to rice, then food sector stocks should have tracked the global price surge in May. The opposite happened. Trung An (TAR) fell from around VND 3,200 to VND 2,900 during the month. Loc Troi (LTG) dropped sharply from VND 6,400 to VND 5,400. An Giang (AGM) did rise from VND 2,000 to VND 2,300, but with short-term speculative volume rather than any change in business fundamentals. PAN, the group's largest stock by market cap at approximately VND 6,700 billion, edged up slightly but moved according to its own logic as a diversified conglomerate, not in response to the global rice price board. VLF has been suspended from trading since early 2026.

This non-reaction is not random. It is the market's answer: the correlation between world rice prices and Vietnamese food sector stocks is near zero, and at times even moves in the opposite direction.

Why Rice Does Not Work Like Oil

Here is the mechanism, and once you understand it, everything becomes logical.

For oil and gas, companies sell their products at near real-time market prices. BSR sells fuel under a pricing mechanism that tracks Brent closely. When prices rise, revenue and margins improve immediately. Stocks react quickly because the link between selling price and commodity price is direct and calculable.

For rice, no such mechanism exists. Export contracts are signed at fixed prices one to three months before delivery. Raw paddy is purchased and stored at the beginning of the crop season. A rice company's margins depend on the spread between the paddy price already paid and the rice price already contracted, not on today's spot price. For companies with large raw material sourcing zones, margins are also significantly affected by the USD/VND exchange rate and ocean freight costs. A small shift in either can erase whatever gain the export price just made.

One more important factor: Vietnam's listed food sector has very few names, small market caps, and extremely thin liquidity. Many sessions see almost no meaningful order matching. A strong macro signal has difficulty moving prices smoothly through stocks like these. Meanwhile, any value added when exports improve typically flows first to farmers and traders, or is absorbed by intermediary costs before it reaches a listed company's profit line.

The Real Story of Vietnamese Rice

The problem for the rice sector is not "prices are low." The problem is "strong in volume, weak in pricing power." That is precisely why the Vietnam Food Association (VFA) recently proposed three groups of measures to strengthen Vietnam's rice pricing power.Bao Cong Thuong

The first group focuses on raising farmers' market position, through a cooperative-enterprise-bank framework that provides post-harvest financing so farmers can store paddy and choose when to sell rather than being forced to sell immediately after harvest. The second group addresses logistics bottlenecks and market diversification, particularly expanding trade with China, the Philippines, and untapped demand in Africa at a time when freight cost volatility is eroding competitiveness. The third group targets brand-building and quality assurance, maintaining variety purity, developing traceability, and building product brands for specialty rice lines.

These are proposals, not enacted policy. But they communicate something important to investors: if implemented, the added value will come from restructuring the supply chain and building brand recognition over many years, not from a few weeks of spot price gains.

Reading the Value Chain to Avoid the Wrong Entry Point

So within the agricultural chain, where does the "commodity prices rise, stocks rise" mechanism actually work? The answer is at the top of the chain, not the bottom.

Fertilizer companies such as DCM (Ca Mau Fertilizer) and DPM (Phu My Fertilizer) price their products close to the world urea price. When agricultural input commodity prices rise, their margins improve almost immediately, following a mechanism similar to oil and gas. This is where the commodity investing reflex operates correctly within the agricultural value chain.

For pure-play rice exporters like TAR and LTG, price transmission is slow and uncertain as analyzed above. PAN, the group's largest company by market cap, moves according to its own logic as a diversified business conglomerate and does not directly reflect world rice prices.

Two signals are worth monitoring in coming quarters. First, whether the cumulative average export price recovers to last year's level. The four-month figure is currently still approximately 9% below the same period in 2025. When that number turns positive, that is when the spot price story begins to touch corporate profitability. Second, whether the VFA's pricing power proposals are translated into specific policy, and on what timeline. Both signals require time to confirm — not just a few weeks.